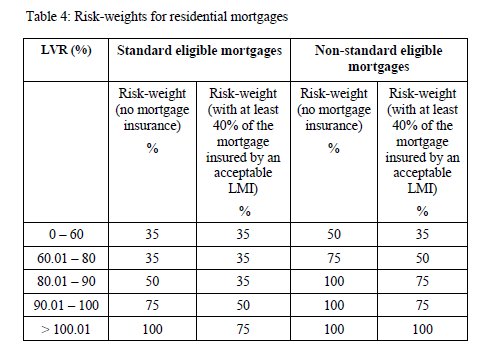

Arguments abound across the web and mainstream media about whether all’s good or the holocaust awaits. Did we survive the GFC better than any western country or did we prime the bubble for a much larger fallout? My school of logic says that the mere fact that so much debate exists means there is a problem. If we accept that there is a problem to be managed then the more the real facts are explained, perhaps the more manageable the problem and the less the fallout. Hysterical bubble talk and delusional denial is not constructive but a “let’s understand what’s going on” may produce some positive results. Unfortunately, both bank and Government spokespeople have far too much vested interest to speak the plain truth. Now that I’ve got that piece of self justification off my chest, let’s have a look at some truth in how the banks calculate capital for residential mortgages. There are two ways an Australian Deposit taking Institution (“ADI”) calculates capital to be allocated against a residential mortgage. Either in accordance with APRA’s APS 112 Attachment C or under Advanced Basel II methodology. Let’s address the rather simple APRA methodology first and then look at the implications of the advanced method. My critics may be saying that I oversimplify. If it’s the simple truth then they’re correct but you can’t understand the bigger position without knowledge of the basic fundamentals. That’s where it starts. My simple question is, how much capital does an ADI need to allocate to a mortgage over time? Let’s start with a $100 mortgage and the table below from APS 112 for standard mortgages. The way ADI capital calculations are articulated, a 100% weighting on a $100 loan asset translates into $8 of capital but APRA weights standard residential mortgages as per Table 4 which shows a lower weight for lower LVR’s. However, I will make the unsubstantiated statement that the total capital now in the system needed by both the ADI and LMI is at least equal to the amount required for an uninsured mortgage. However, for a very long time it was not and a significant arbitrage was in the system between ADI’s and LMI”s until 2008. The definition of standard loan is as follows as referenced in APS112. 6. A standard eligible mortgage is defined as a residential mortgage where the ADI has: (a) prior to loan approval and as part of the loan origination and approval process, documented, assessed and verified the ability of the borrowers to meet their repayment obligation; Sounds reasonable enough, even the last sentence. But here lies the “arbitrage the system” opportunity that every banker dreams of. APRA in APS-112 have insisted that property is revalued by an ADI if “it becomes aware of a material change in the market value of property in an area or region”. I will express an opinion here that I’m sure APRA was trying to protect against properties falling in value but have left open the biggest game in town for all our banks. Currently the major and regional banks use the services of the new technology of automated valuation models (AVMs) to revalue their mortgage books upwards to decrease their capital requirements. Has a light switched on yet as to why there has been such a dramatic rise in the use and media coverage of those property valuation spruikers. If anyone knows of one of those banks who do not use AVMs can you please let us all know. So what is the effect of continually revaluing the properties upwards? Using our standard 95% LVR mortgage above, let’s assume a revaluation so that the LVR is now 85%. The capital required is now $100*50%*8%= $4 with a return on capital requirement of $4*20%= $0.80 pa. Quite a difference, and if we go one step further, then the result and achieve a 75% LVR then the capital is now $2.80 with a return requirement of $0.56. So with roughly a revaluation of the property of 20% (ask any property spruiker, “That’s nothin’ mate!”) a bank can save itself $3.20 of capital per $100 of mortgage which can be recycled as capital to support another mortgage. Think about how that increase in both return on capital and funds allocated to another mortgagor slave is an absolute incentive for bankers to perpetuate the cycle up of house price valuations. Their reward? Huge bonuses based on what is in essence a positive reinforcement spiral where everyone pats each other on the back for what a great job they’re doing. Well at least, that is, until the money runs out. What was that? Did you hear anything? Maybe the sound of a slow burning fuse? But I digress. Under advanced Basel II methodology, banks are able to have their own approved internal models which replace the APS112 requirements. These models only make it much less transparent as to what the capital calculations are based on. Please see the CBA’s statement and make note of the amount of residential mortgages used to calculate capital adequacy on APS 330 Table 16a to 16d – Capital adequacy (risk weighted assets) ie $ 56,753M and the actual credit exposure on table APS 330 Table 17a – Total credit exposure excluding equities and securitization ie $326,384M to understand the extent of the difference between what is actually lent and the exposure used to calculate capital. In this case for CBA it’s $269Bn. I cannot explain how the numbers have been calculated other than to point them out and that some internal model which updates valuations has been used. The benefits on the way up in house prices would seem to be huge. What would the effect be if house prices dropped 20%?, 30%?, 40%? If you have followed all of this then you have my utmost compliments, but also, maybe your heart should also be jumping a beat or two. The emu in the kitchen is not what losses the banks will have to suffer if house prices reduce and borrowers default in large numbers, it is where do they find the capital to support all those loans now on increased LVRs that have not defaulted? As APRA have required, The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region. A positive reinforcement spiral on the way up and a negative one on the way down. Maybe that’s not a fuse I hear, but a gurgle….gurgle…..blup! As all 4 major banks have the same issue to varying degrees, this is a huge systemic risk. It also means for this writer anyway, that it’s not difficult to predict what will happen. The current Government will, in cahoots with the banks, do all in its power to prop up the mortgage and housing markets to the misery and detriment of all new borrowers and many existing ones. Like the bank CEO’s, the PM and her ministers, ie when the truth is finally drummed into their incompetent heads, will just be praying that they’ve collected their loot and past the parcel before it all collapses. Maybe, Matilda, the gangs will take over the highways! Disclaimer: The content on this blog is the opinion of the author only and should not be taken as investment advice. All site content, including advertisements, shall not be construed as a recommendation, no matter how much it seems to make sense, to buy or sell any security or financial instrument, or to participate in any particular trading or investment strategy. The author has no position in any company or advertiser reference unless explicitly specified. Any action that you take as a result of information, analysis, or advertisement on this site is ultimately your responsibility. Consult someone who claims to have a qualification before making any investment decisions. It really is an extraordinary situation Australia finds itself in right now. Whilst we can learn much from history, don’t look there for the answer on this one as the financial position of the country is unprecedented. Although this is par for the course for just about the entire globe, ours seems to be a different different.

It really is an extraordinary situation Australia finds itself in right now. Whilst we can learn much from history, don’t look there for the answer on this one as the financial position of the country is unprecedented. Although this is par for the course for just about the entire globe, ours seems to be a different different.

As far as mainstream media is concerned, do any of you media hacks out there have the figures on how much revenue is generated for Fairfax and News by real property advertising in Australia? Unfortunately, everyone the public relies on has a massive thumb in the 4 and 20.

Therefore if a mortgage is standard and written at 95% LVR then the capital allocated is $100 *75%*8% = $6. On the basis that an ADI wants a 20% return on capital then a borrower pays $6*20%=$1.20 pa to the bank as a return on capital. We’ll not complicate matters by doing the calculation for mortgage insurance as this also involves calculating the capital required for the LMIs.

(b) valued any residential property offered as security; and

(c) established that any property offered as security for the loan is readily marketable.

The ADI must also revalue any property offered as security for such loans when it becomes aware of a material change in the market value of property in an area or region.

Advertisement

Advertisement