There is an old trading adage which I subscribe to that says you should not overtrade. It’s the same with blogging about currencies – sometimes it is best to stay on the sidelines. So I’ve been quiet as there hasn’t been much to say on the Aussie this week. Really, it has just traded in a range, tested support at 1.05 and found it solid, and is now back up at 1.0667 testing fibonacci resistance from the past week or so’s range.

It is fair to say that this quiet trade is indicative of a currency market that is lacking in catalysts to break recent ranges at present (perhaps all the volatility has sapped traders nerves) while the USD tries to work out what its doing, while Japan slips back into recession and while Europe deals with Greece and the succession to DSK’s Presidency at the IMF. So the focus is simply elsewhere.

But there is something that I found interesting in the RBA minutes with regard to the currency earlier this week that is worth drawing out in the context of the long run trend for the AUD and what it means for exporters and our economy.

The RBA said (my bolding),

The Australian dollar had appreciated to a fresh post-float high against the US dollar. On a trade-weighted basis, the currency was at its highest level since 1985 and had appreciated by 6 per cent since the start of the year. While this partly reflected the general depreciation of the US dollar, the Australian dollar had tended to rise more than most other currencies. An important influence had been purchases by other central banks seeking to invest their official reserve assets.

Now we have talked about the impact of diversification of investors into the AUD many times. It’s all about the “Investment” fundamentals I talk about all the time.

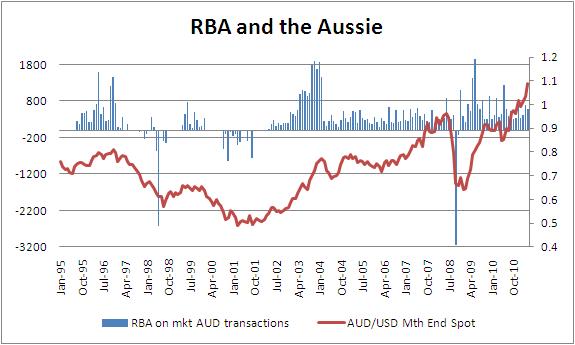

But what the paragraph above does do, along with a chart I’ve put below, is tell us what the RBA is thinking and crucially doing about the AUD’s strength.

This chart is from the RBA Statistical tables with the Blue bars representing RBA “Market” transactions in either buying or selling foreign exchange. Above the line it is buying FX, that is selling Aussie, while below the line it is sellinig FX and buying Aussie.

The stark thing for me is how aggressively the RBA resisted the pulse higher in 2003/2004 and in 2009 compared to both 2007/8 and now.

Now, it is important to know that the RBA says it intervenes only when markets get disorderly to add liquidity. They move when they think that the level of the AUD/USD (for want of a better indicator and because it represents the bulk of the trading volume) is out of line with the economic fundamentals.

The massive intervention on the buy side to support Aussie during both the Asian crisis and then again when Lehman Bros. fell over speaks for itself, but equally so does the lack of Aussie buying (in massive interventionist volume anyway) around the lows back in 2001. They mustn’t have thought the rate was too far out of wack.

And so it seems is the case now. In highlighting in its minutes that other central banks are buying the Aussie for their reserve assets they are implicitly signalling that we are an attractive destination but equally they can’t stand in the way of the freight train . No surprises there.

Indeed, the RBA’s current passivity speaks volumes about how they view the Aussie’s appreciation as it is holding back the need to hike rates faster and further, which gives them time to assess what’s really going on in the economy. No matter the hawkish rhetoric in their minutes or from the bullhawks.

This doesn’t help us with a resolution as to whether the Aussie is going to break down through 1.05 or move back to 1.10. But it does reinforce that we all need to get used to a higher Aussie on average than the past decade or two. We’ve been singing from that hymm book for some time but clearly the RBA and their central bank cousins agree.