The Business

The bulk of BHP’s non-current assets reside in Australia (55% as of June 2010), with 14% in South America and 11% in North America.

BHP Billiton came into existence in 2001 when Australian Broke Hill Proprietary Company merged with Anglo-Dutch Billiton. BHP is listed on both the ASX and the London Stock Exchange and is the largest company on the ASX by market capitalisation.

Financials

BHP’s return on equity (ROE) has averaged an impressive 48% over the last 5 years. ROE dropped to 22% during the GFC, but is now forecast to rise to 49% for FY11. Intangibles assets are very low at $0.14 compared to $10.53 of tangible assets, which is expected given the large capital investment required for a resource company.

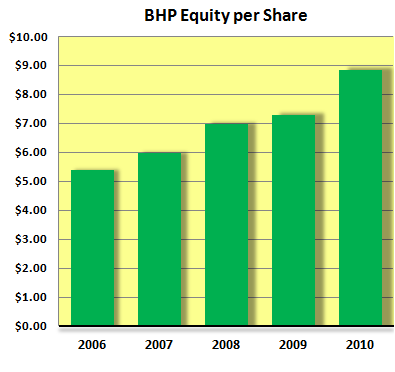

BHP’s net debt is zero, with $16B in interest-bearing debt offset by $16.2B in cash and equivalents – another impressive statistic for a mining company. Equity per share has grown consistently from $5.23 at the start of 2006 to $10.65 in 2011 as a result of acquisitions and organic growth. After several failed merger and joint venture deals, BHP instituted a share buy back program in 2010 in order to return surplus cash to shareholders.

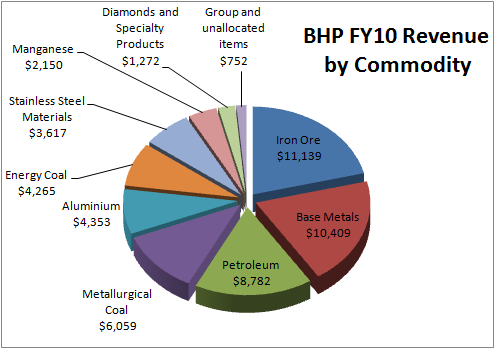

In terms of earnings streams, BHP revenue totalled $52.8B in FY10. Of this, 25% was from Chinese customers, 19% from the rest of Asia (excl Japan), 16% from Europe, 11% from North America and 10% from Japan.

[one_half]

Return on Equity

[/one_half]

[one_half_last]

Equity per Share

[/one_half_last]

[/one_half_last]

Management

BHP is currently lead by CEO Marius Kloppers, who took the helm in October 2007. Holding a degree in chemical engineering, he has both technical and corporate experience in the industry, especially within the BHP/Billiton organisations. The remaining top-level management consists of a mix of industry, finance and corporate expertise with a heavy emphasis on resource backgrounds.

BHP management has tried to expand BHP’s reach through several acquisitions and JV opportunities over the last few years. Some of these have been successful; however those that would have significantly increased BHP’s market power were stopped by regulatory authorities. BHP is still looking to diversify into soft commodities like potash. The use of surplus cash to buy-back shares in 2010 (after the failure of the Rio Tinto joint venture) indicates a good grasp of capital management.

Management remuneration is based on a complex combination of base salary, short term incentives ,cash incentives and long term share-based incentives. Cash incentives are typically at the same level as base salary, whilst the long term incentives appear to be the largest of the renumeration components.

Opportunities

- BHP will continue to benefit from high commodity prices as long as China continues to grow,

- BHP has a well-diversified portfolio,

- The balance sheet of BHP is very good, with low debt and high ROE,

- Management have pursued sensible acquisition targets, whilst also returning cash to shareholders where appropriate.

Risks

- BHP’s earnings are tied to the strength of commodity prices and the US dollar (the currency in which its commodities are sold), both of which can be volatile,

- BHP’s increasing reliance on China to generate revenue growth,

- Regulatory attempts to increase BHP’s tax burden (especially in Australia),

- The increase in supply being brought online around the world (due to new mining projects) may see commodity prices decrease in the medium to long term.

Summary

BHP is the world’s largest resource company, with a healthy balance sheet and impressive ROE. It is well positioned in the midst of a commodities boom, with a variety of established, low-cost operations spread around the globe.

Management appear to consider the allocation of capital seriously, choosing acquisition targets well whilst also returning surplus cash to shareholders at appropriate times.

At Empire Investing we consider BHP Billiton to be a “Good” company due to a lack of competitive advantage and its exposure to commodity price and exchange rate volatility.

Valuation

Using a forecast ROE of 36% (dropping to 28% over 5 years) with an equity per share of $10.65, Empire values BHP at $46.00 per share.

Using a 50% Margin of Safety, our maximum buy price is ~ $30.70.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has no interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.