The China Banking Regulatory Commission last week issued several strict-sounding new rules applying to the issuance of Wealth Management Products (WMPs). The investment products have seen massive growth in the past year, with assets tripling to RMB10tn in the past two years, equivalent to 10 per cent of all China’s bank deposits.

Apart from upsetting share prices of mainland Chinese banks, what are the new rules actually going to achieve — if anything?

Advertisement

Here’s a summary of the key points of the new rules, mostly via Chinascope Financial:

– Banks are now required to link each WMP to specific assets rather than an undifferentiated pool.

– No more than 35 per cent of a bank’s WMPs or 4 per cent of a bank’s total assets should be invested in debt that is not within the formal bond market. “Debt outside the formal bond market” refers to the credit assets, trust loans, entrusted loans, acceptance bills, letters of credit, and account receivables that are not traded on the securities exchange or interbank market.

– Banks should not provide guarantees or make repurchase commitments to their WMPs.

– Banks need to be prudent while using the funds raised by their WMPs.

We have written a couple of times about the potential problems with WMPs; the key things are that they have potentially risky duration mismatch (increasingly very short-term against illiquid assets such as property developments); and the underlying assets are almost always well-hidden from investors, as reports from Reuters and the FT demonstrate.

Advertisement

The two problems are self-reinforcing and in trying to solve them, it only gets more complicated. As Capital Economics’ Mark Williams and Qinwei Wang write, around 60 per cent of WMPs were of less than three months duration, far shorter than the underlying assets:

WMP issuers have adopted two main strategies to deal with this problem. One is to repay maturing WMPs using money raised from new WMPs. This would leave any given product highly exposed to a downturn in confidence in whichever asset class it was invested in. WMP issuers have then attempted to lower this risk by creating pools of assets into which WMP funds are invested. This has had the effect of obscuring the risks attached to individual products. In the event that many investments failed, unwinding the WMPs would be difficult. Around 80% of new WMPs issued over the last three months are of this “mixed” type. (See Chart 2.)

Advertisement

The new rules, write Williams and Wang, try to address these problems (emphasis Capital Economics’):

Banks are now required to link each WMP to specific assets rather than an undifferentiated pool. Issuers are instructed to disclose more information about the structure of investments. And WMP loans delivered through channels other than interbank or securities markets must be kept below 35% of the outstanding value of WMPs and 4% of banks’ total assets.

The other big criticism of WMPs is that is that they are marketed through bank branches and therefore often seen as being essentially guaranteed by the banks and by extension, the government. Again, the rules appear to tackle this head on by prohibiting guarantees.

Advertisement

The thing is, as we (and others) have pointed out several times, China’s growth isincreasingly credit-fuelled of late.

As Anne Stevenson-Yang of J Capital Research writes, an ever-growing proportion of that is coming from alternative lending channels. This is not an accident, writes Stevenson-Yang; China’s shadow financing is like a game of ‘whack-a-m0le’ where as soon as one channel is tightened, another appears.

Yet the whole thrust of financial policy over the last year has been to push more financing into alternative channels, without acknowledging how tightly linked those channels are with the banks. This chart shows how non-bank channels have grown alongside total financing:

Advertisement

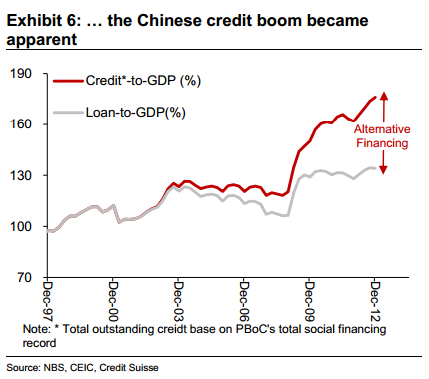

Or, here’s a longer-term chart, from Credit Suisse:

For this reason, Stevenson-Yang is sceptical that these measures are intended to seriously curtail the volume of shadow financing activity. She writes:

The elephant in the room is that the shadow institutions are the co-dependent evil twins to the commercial banks. This is true in two ways: banks are reliant on the shadow institutions to supply their liquidity, and shadow institutions get a lot of their capital from the banks.

At the banks, the key metric to watch is interbank repo assets. Repo assets are like amphetamines mainlined right into the banks’ circulatory system: they represent short-term borrowings that provide liquidity. A big chunk of these assets derives from trusts, WMPs, banker’s acceptances that are discounted in the private market, and other exotic instruments. The repo market works because of guarantees—no bank is going to borrow from another bank without a guarantee. If regulatory pressure were really to come down on this mechanism, the banks might be in trouble.

Not only does the shadow market fund the banks, but banks fund the shadow market: banks are the ultimate source of many “non-standard” financial products. Just about every small local lending institution has a beneficial owner or a director who is also a director of the local commercial bank. That person or institution acts as a bridge to convey cheap bank loans to the more expensive private lending channel. The whole market is running on the rate arbitrage between official channels, which lend at 6.5 9.5%, and gray channels, which lend at 12-60%.

Advertisement

This might sound far-fetched if you don’t closely follow the incredibly dynamic Chinese shadow financial system. Examples however abound of the links between the shadow, grey and formal banking sectors. Look at the case of Huaxia Bank in November and December last year: one of its Shanghai branches was target by investors who lost the principal of a WMP that was issued by Zhongding Wealth Investment Center but sold at the bank. Huaxia in turn said it had nothing to do with selling the Zhongding WMP and blamed a “rogue employee” for the sales (it’s hard to say how it really went down; the bank employee’s husband said she was made a scapegoat). Clearly the China Banking Regulatory Commission would prefer less of this sort of thing — at least enough to take the government more clearly off the hook for WMP failures; if not to actually curtail credit growth itself.

As Capital Economics’ Williams and Wang write, the real solution would be to end the policy of financial repression which sees Chinese households desperately seeking yields above the mostly sub-inflation rates they can get on bank deposits. Which in turn sees them piling into real estate, financial instruments, or an ever more convoluted combination of the two.

However…

Advertisement

We always have to point out in these kinds of posts that China’s government, its regulators and various influential agencies are not perfectly unified in their approach to the country’s economy. The People’s Bank of China and the CBRC in late Decembercalled for more vigilance about ‘risk’, particularly around local government financing vehicles (LGFVs), another somewhat sketchy segment of the Chinese financial system.

The official 2013 M2 growth targets, meanwhile, were lowered relatively sharply to 13 per cent for 2013, down from 14 per cent in 2012. So to us it seems conceivable that the new WMP rules are perhaps intended to dampen credit growth just a little. Whether or not the relevant authorities are simply expecting the ‘mole’ of shadow finance to pop up somewhere else, though, is hard to gauge.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.