The Cypriot drama is beginning to wane, but if you read the MoU you’ll understand that this story is far from over:

The economic adjustment programme will address short- and medium-term financial, fiscal and structural challenges facing Cyprus. The key programme objectives are:

to restore the soundness of the Cypriot banking sector by thoroughly restructuring, resolving and downsizing financial institutions, strengthening of supervision, addressing expected capital shortfall and improving liquidity management;

to continue the on-going process of fiscal consolidation in order to correct the excessive general government deficit, in particular through measures to reduce current primary expenditure, and maintain fiscal consolidation in the medium-term, in particular through measures to increase the efficiency of public spending within a medium-term budgetary framework, enhance revenue collection and improve the functioning of the public sector; and

to implement structural reforms to support competitiveness and sustainable and balanced growth, allowing for the unwinding of macroeconomic imbalances, in particular by reforming the wage indexation system and removing obstacles to the smooth functioning of services markets.

It all sounds very Greek to me. Although Cyprus has been granted an extra year to meet a 4% surplus, from a 2.4% deficit, I have no doubt given the completely broken banking system, in which BoC unsecured debt holders are now rumoured to take a 60% haircut, that the country’s economy will report heavily on the downside for many years to come. The MoU reads much like a standard IMF wish list in which internal deflation is expected to reap reward, but as we have seen from other struggling Eurozone nations in most cases this is an economic mirage. Russia has also announced it will not be providing support to depositors who have lost money under the Cypriot bailout, which I can only assume will greater dampen any remaining confidence in the Cypriot banking system.

Advertisement

Of note, however, is that it isn’t just Cypriot depositors taking a bath in Europe. As I mentioned back in July last year, Spanish banks did their best at entrapping deposit holders via the use of under-regulated security offerings promising high yield to unwitting members of the Spanish public. That now also has come home to roost:

CYPRIOT depositors are not the only ones suffering the aftermath of a banking bust. People who bought shares or subordinated debt in Spain’s dodgiest cajas, or savings banks, have either been all but wiped out or forced to take hefty losses. Many small Spanish investors are among them.

Four months after Spain requested a €40 billion ($51 billion) chunk of its banking bail-out funds from its euro-zone partners, on March 22nd it delivered the blow that hundreds of thousands of retail investors feared. The FROB, Spain’s restructuring fund, imposed haircuts of up to 61% as it turned junior debt and preference shares in four nationalised banks—Bankia, Catalunya Banc, Banco Gallego and NCG Banco—into equity.

This week the Spanish government also finally announced its downgrade of its economy, bringing it somewhat in-line with its own central bank, as yet another political scandal rocks the country.

Advertisement

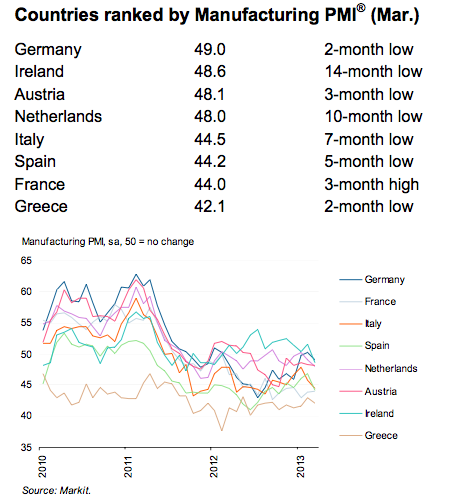

Overnight was also another round of manufacturing PMI data and there wasn’t any good news in it. Germany manufacturing hit a 3 month low, French data continues to worsen, Spain is accelerating downwards, as is Greece, The Netherlands is getting weaker and even Ireland took a dive in March:

Comments from Markit Economics wrap the dour data well:

Advertisement

The Eurozone manufacturing sector looks likely to have acted as a drag on the economy in the first quarter, with an acceleration in the rate of decline in March raising the risk that the downturn may also intensify in the second quarter.

The surveys paint a very disappointing picture across the region, with all countries either seeing sharper rates of decline or – in the cases of Germany and Ireland – sliding back into contraction.

Companies reported that signs of stronger demand from markets such as Asia and the US were countered by a renewed weakening of demand within the euro area, in turn reflecting deteriorating business and consumer confidence.

While in some respects it is reassuring to see that the events in Cyprus did not cause an immediate impact on business activity, with the final survey results even coming in slightly higher than the flash estimate, the concern is that the latest chapter in the region’s crisis will have hit demand further in April.

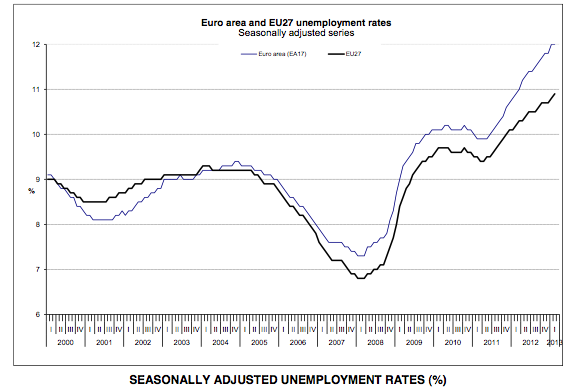

So, like much like the other PMI data, the beginning of 2013 continues to show economic weakness in the region. As expected this is showing up in the unemployment figures which once again reached a new record in February:

The euro area (EA17) seasonally-adjusted unemployment rate was 12.0% in February 2013, stable compared with January. The EU27 unemployment rate was 10.9%, up from 10.8% in the previous month. In both zones, rates have risen markedly compared with February 2012, when they were 10.9% and 10.2% respectively. These figures are published by Eurostat, the statistical office of the European Union

Eurostat estimates that 26.338 million men and women in the EU27, of whom 19.071 million were in the euro area, were unemployed in February 2013. Compared with January 2013, the number of persons unemployed increased by 76 000 in the EU27 and by 33 000 in the euro area. Compared with February 2012, unemployment rose by 1.805 million in the EU27 and by 1.775 million in the euro area.

In short, Cyprus maybe out of the way in the short-term, but you the smell emanating from the EZ economy is growing again.