You’ll find any number of articles in the press today about the terrific value of mining stocks. The source of this majority act of contrarianism (yes, that’s an oxymoron) seems to be a Goldman Sachs report that yesterday did a nice job of outlining the discounts in the mining and metals segment of the ASX. It’s either that or the journo’s are star-struck by proximity to big mining names at the Baio Forum.

So does the valuation argument in favour of buying miners stack up? From Goldman:

Focus on the Miners

Given our more cautious views on bulk commodity prices and concerns over margins if revenues fall, we recently downgraded the Resource sector from Overweight to Neutral (see. Post-reporting, post-rally: Resetting our views, March 11). Despite the sector’s poor momentum at the time, we were hesitant to move underweight given the valuation support on offer.Since then, the sector has fallen 12.2% underperforming the ASX 200 by 7.8%.

While we remain concerned about the short-term momentum in the sector, we have taken the opportunity to review the long-run performance, earnings and valuation trends given the relative value that has emerged over recent months.

The Miners over the long-run

Over the past 2 years, the Mining sector has underperformed the ASX 200 by 40%, its worst run since 1999, when the sector lagged by 55% over a 2-year period. The drivers of that period seem similar to today: Resources suffered significant share price falls driven by weak revenues and high fixed costs, while the broader market was relatively strong.Miners now trade at 11.3x forward EPS, a 30% discount to Industrials. On a relatively low 3.3% yield they have missed the markets re-rating of higher income generating stocks, but this remains a possible upside case given recent pay-out ratios of c.40% are well below the 60% pay-out that was delivered during the low growth phase pre-2003.

50% of the ASX Metals sector now trades below 10x P/E and 5x forecast EV/EBITDA: DML, MGX,SFR, FMG, PNA, AGO and RIO.

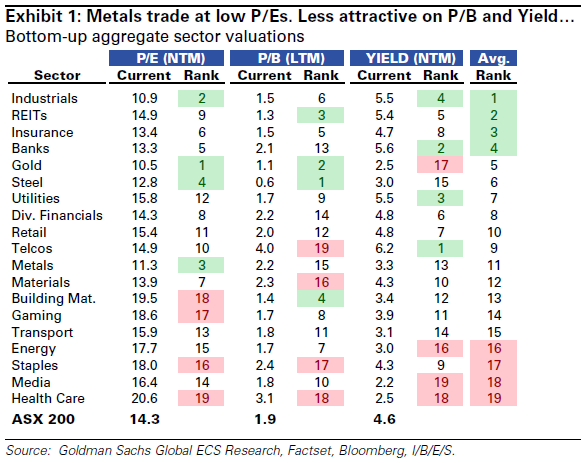

Here are the key charts. First, the sectoral valuations:

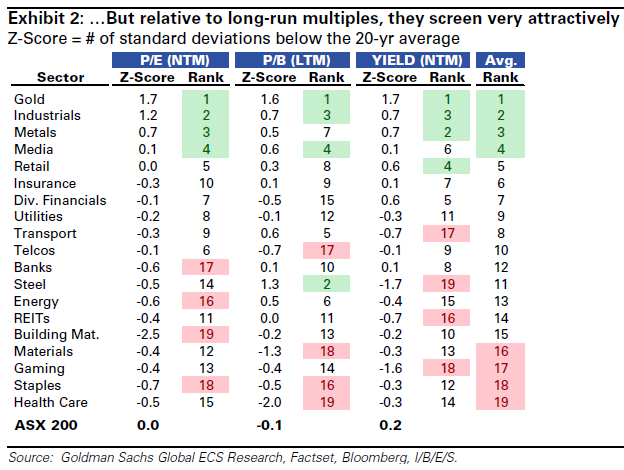

And over time:

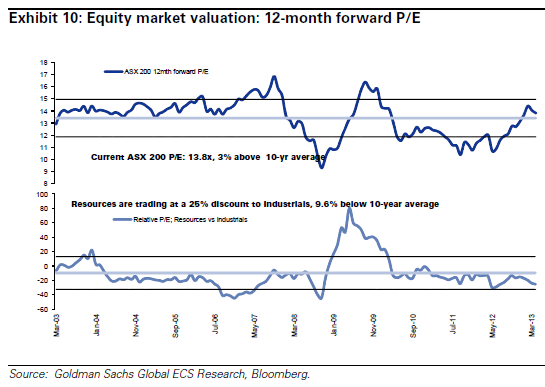

And the discount to Industrials:

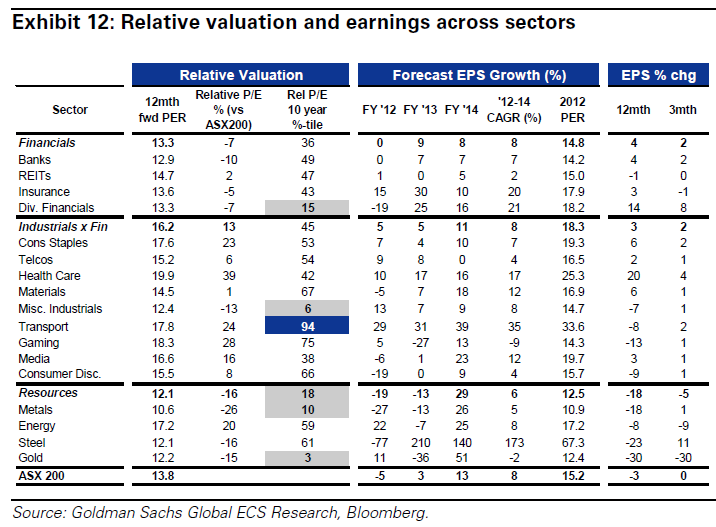

And EPS growth forecasts:

Take a look at those EPS growth forecasts for industrials (2014 11%) and mining (2014 28%). These are very aggressive. They imply a smooth as silk transition in Australian rebalancing with soaring volumes for miners and a rebounding non-mining economy for Australia. With nominal growth likely to struggle to hit 5%, how are industrials going to get this kind of growth?

With all due respect to the market, these forecasts are bunkum and so therefore are the valuation calculations. That doesn’t mean financial repression won’t stretch the valuations even further but there is no fundamental valuation argument here to buy Industrials (except those with dollar exposure). So comparing miners to Industrials at this point doesn’t make much sense either.

I’ve long been of the view that fundamental or value analysis is a good times methodology. To really understand value you need macro and other tools. One really doesn’t need to get past the first sentence of the Goldman report to answer the question of whether it is time to buy the miners. Goldman is bearish on bulk commodity prices. And with good reason.

There were only two reasons prices were so high in the first place, the China demand shock, as well as QE and a falling $US adding to the attractiveness of real assets for speculators. Neither of these is what it was. The Chinese authorities appear determined to slow the investment component of their economy, via crisis or not, and new mine capacity has caught up to demand already in bulk commodities. In the US, QE has passed its usefulness as a currency devaluation tool as other countries outdo it and the $US has stopped falling.

If, as I believe and the markets are now beginning to discount, the Chinese succeed in slowing the investment component of their economy, mine capacity will exceed current demand by a very significant margin quite soon. In iron ore, Morgan Stanley is forecasting a 100 million tonne surplus in seaborne iron ore for 2015, growing to 300 million tonnes by 2018. And this is on still aggressive demand growth rates of 7% next year falling to 4.4% by 2017. It will never happen.

What will happen is this. As excess capacity grows, bulk commodity prices will fall further and some of the mines will to have to close. In short, there will be a bust that takes out marginal players. We had a taste of it late last year.

At that point, markets will heavily discount all miners as it sorts out winners and losers. That will be the time to buy as the majors pick through the ruins of the marginal players, consolidate production and regain pricing power. Right now, miners are a value trap.