Cross-posted from FTAlphaville.

Following on from our post on Monday comparing China’s relatively low GDP growth and its relatively high levels of new credit…

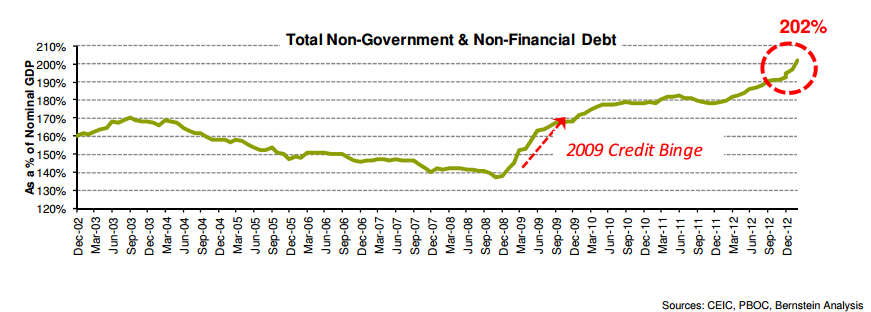

Here are some updated charts from Michael Werner of Bernstein Research, which show that the total stock of non-government and non-financial debt to nominal GDP continued to climb to new levels in Q1 (it was 193 per cent at the end of 2012):

(There are other ways of comparing credit growth and GDP which we looked at in theoriginal post; those did not change so much.)

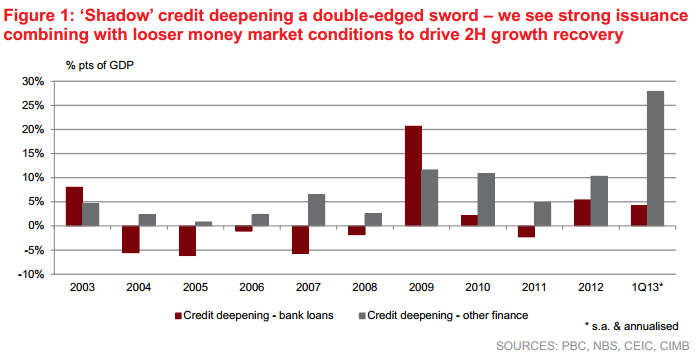

Meanwhile the cost of financing all that debt continues to rise, relative to the total economy:

This increased cost of financing has occurred together with a rise in shadow banking as a proportion of total credit:

We’ve mentioned before that shadow financing, as well as tending to be more expensive than bank loans, also seems to generate less growth.

A couple of commenters were wondering why credit-to-growth ratio (or credit-to-GDP if you prefer) is important anyway.

We think there are a few good reasons as to why. One is that those financing costs keep rising. Another is that China’s economic growth appears to be increasingly derived from credit growth and therefore if the credit growth stops, it might have some ugly effects on growth.

But what happens when it does stop?

The FT’s bureau chief Jamil Anderlini has a very interesting piece on how a financial crisis might manifest in China. He argues that it wouldn’t fall into the familiar categories seen elsewhere — depositor bank run, or interbank freeze, or foreign capital outflows — because China’s state maintains a tight grip on both the domestic system banking system and the country’s capital flows. In otherwords, a banking crisis would effectively be an almost unimaginable crisis of confidence in the entire state.

What is a little easier to envisage is a repeat of the previous Chinese banking crisis:

Back then, the state-owned financial institutions, under orders from the party to avoid a traditional crisis at all costs, were busy rolling over, forgiving and hiding the mountains of bad loans they had built up through state-directed lending in the 1990s.

The result was non-performing loan ratios of up to 50 per cent and a clutch of zombie banks that kept on lending but created progressively less real economic activity.

Some analysts warn that a similar dynamic is at work today following the enormous expansion in lending to local governments and state-backed infrastructure projects in the wake of the global financial crisis in 2008.

Indeed, and these warnings have been around for some time — but another of our colleagues in Beijing, Simon Rabinovitch, has a must-read story on a very strong warning on the local government debt situation which is notable because it comes from a senior figure within the Chinese financial industry.

As for the late 1990s/early 2000s crisis, the Reserve Bank of Australia has a history of Chinese banking with a breakout box that summarises it in a little more detail for the curious.

Much of the Chinese banks’ lending during the late 1980s and 1990s was to state-owned enterprises, many of which were loss-making and reliant on bank credit to continue financing their activities, but ultimately did not repay these loans (Lardy 1999). Bank lending had also contributed to a boom and subsequent bust in the real estate and stock markets in the early 1990s (Huang 2006). As a result, banks’ non-performing loans increased significantly: by the late 1990s the large state-owned banks’ aggregate non-performing loan (NPL) ratio exceeded 30 per cent (Huang 2006).[1] These banks were severely undercapitalised at this time (relative to minimum international regulatory standards) and had only small loan loss provisions (Lardy 1999).[2]

The very short version of what happened next is that the government established four big asset management companies (AMCs) to deal with many of the bad loans, and others were simply written off, prior to the big banks listing in Hong Kong.

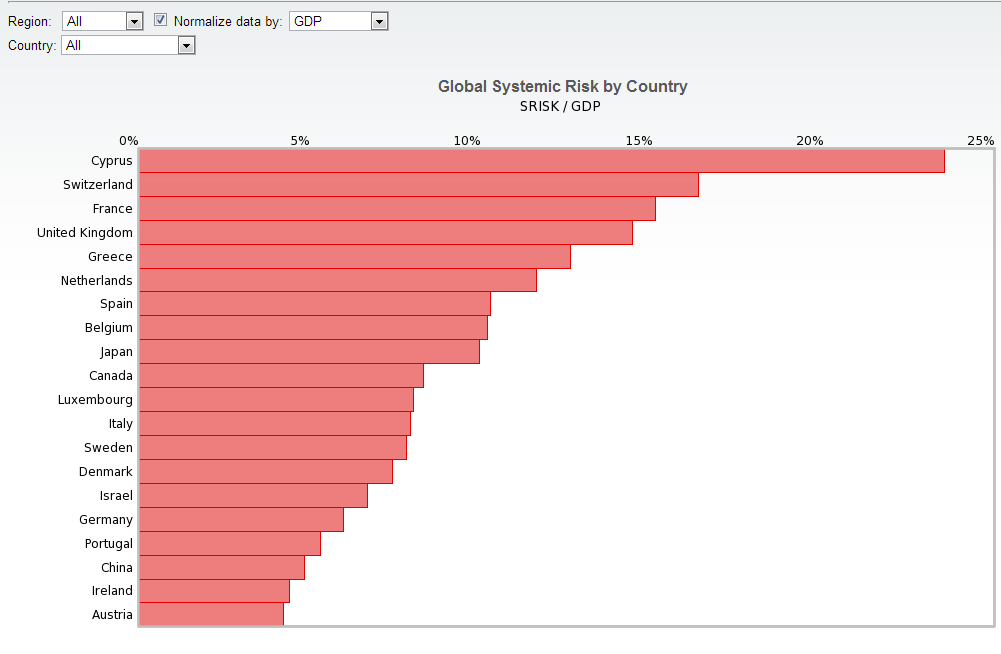

We’ll just ponder quickly how well-placed China really is to deal with another banking crisis. By this measure from NYU Stern’s ‘SRISK’ tool, which compares bank assets by country to evaluate their systemic risk of a banking crisis, China looks fairly bad:

Yet, when adjusted for GDP, China is barely on the list:

So, kind of not much of a problem. Unless you consider two things: first that a lot of the debt in China doesn’t show up in the banking system; and secondly that the nature of China’s capital regime and the related fact that much of its current account surplus is tied up in foreign assets that would be tricky to sell down. In fact volatility supremo and NYU Stern professor Robert Engle, who led the development of the SRISK system, expressed scepticism about this when we asked him about it at a conference in Sydney late last year.