At last we’re getting somewhere in official circles. The Bureau of Resource and Energy Economics (BREE) has released its April half report and, yes, there is an investment cliff in the offing.

For the first time, BREE offers a forecast for the stock of investment in the pipeline in the years ahead:

BREE has modelled two scenarios based on this rating system:

• A ‘likely scenario; which includes all existing projects at the Committed Stage and the projects assessed as likely to progress to the Committed Stage in the next five years.

• A ‘possible scenario’; which includes all projects in the likely scenario, but also includes projects assessed as possible in terms of their progression through to the Committed Stage within the next five years.

Projects assessed as unlikely to proceed are not included in the forward projection of the value of committed investment. The two scenarios model the rate at which projects currently at the Committed Stage are expected to move to the Completed Stage and are subsequently removed from the list, as well as the timing of projects assessed as possible or likely to progress to the Committed Stage.

Advertisement

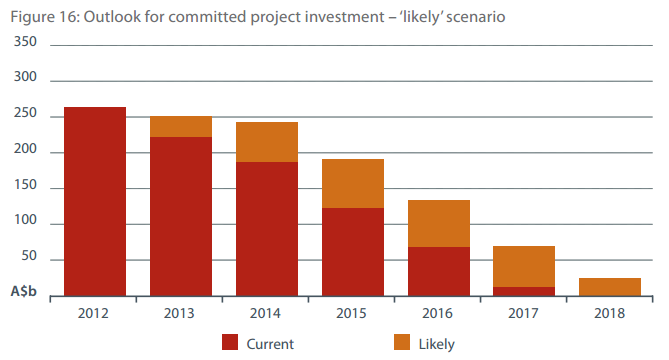

Here’s is BREE’s “likely” scenario:

In the six months from October 2012 to April 2013, the value of projects at the Committed Stage of development decreased by $799 million. There are currently projects valued at $43 billion at the Committed Stage that are scheduled to progress to the Completed Stage by the end of 2013. The largest of these include Citic Pacific’s Sino Iron project ($8.4 billion), Rio Tinto’s Cape Lambert expansion ($5.2 billion) and the Woodside led NWS Rankin B joint venture ($5 billion). Potentially offsetting this expected decrease in committed investment is $31 billion of projects assessed as ‘likely’ to progress to the Committed Stage that have a FID scheduled in 2013. In this ‘Likely Scenario’, the net effect is for the value of projects at the Completed Stage to decrease by $12 billion to total around $256 billion at the end of 2013 (see Figure 16).

After 2013, the value of projects currently at the Committed Stage is scheduled to moderate, underpinned by the completion of mega projects currently under construction. In 2014, Queensland Curtis LNG and BHP Billiton’s Jimblebar iron ore mine are schedule to start up, followed by Gorgon LNG, Gladstone LNG and the first train of APLNG in 2015.

In 2014 the stock of committed investment in the likely scenario decreases by $8 billion and then by a further $63 billion in 2015. From 2017 onwards, the stock of committed investment in the mining sector is projected to revert back to levels comparable to 2007. BREE expects that this would lead to a substantial decrease in the flow of annual capital expenditure, as measured by the ABS.

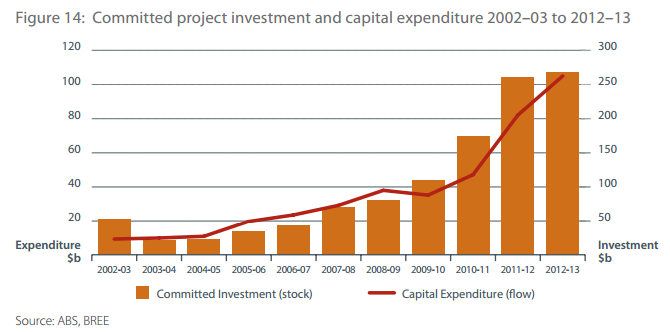

Now remember this is the stock of projects not the flow of spending. Nonetheless, holy cow! The timing is different to some private forecasts but a $71 billion fall in the stock in two years to 2015 is very big. And the relationship between stock and flow is strong as BREE illustrates:

It should be noted that not all committed project investment is spent in Australia, and not all capital expenditure is related to committed projects. Nevertheless, as can be seen in Figure 14 there is a close relationship over the past ten years between the value of committed project investment (the stock) and ABS capital expenditure data (the flow).

Advertisement

What’s more, in my view, this is still bullish forecasting. I don’t expect any more major project approvals in bulk commodities as the terms of trade keep falling. That could change with a very big fall in the dollar. But until then, projects are off.

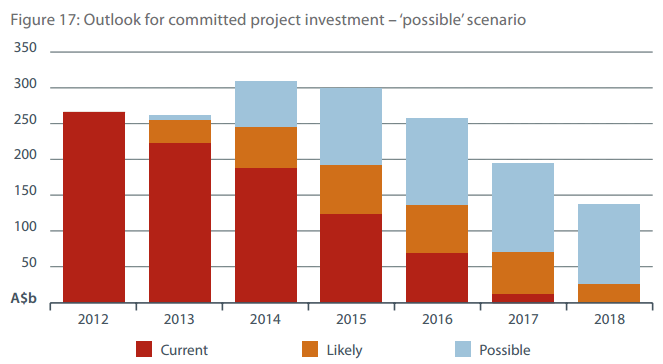

BREE’s more optimistic scenario is that we secure more investment:

From 2014, the value of projects assessed as ‘possible’ increases substantially. If the challenges to these possible projects progressing can be resolved, there is an opportunity for committed investment in resources and energy major projects to exceed the level in April 2013. Market factors, particularly commodity prices, and especially costs of construction will play a key role in determining the future of many projects assessed as possible.

Advertisement

I’ll refer to this as BREE’s delusional scenario. The only real prospect I see for more investment is in FLNG and it won’t be in the next three years.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.