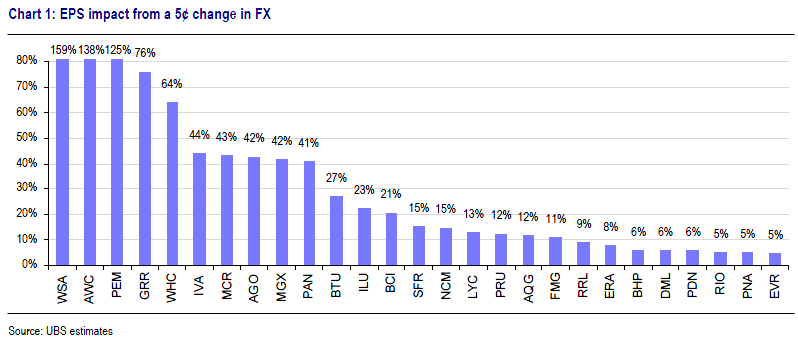

Anyone would think that Australia was an economy of houses and holes. It’s a constant snap back narrative of buy banks, buy miners, as if that’s the only option. It isn’t and a couple of new investment notes today show why. The first is from UBS looking at the positive benefits to miner’s EPS if the dollar keeps falling. The chart assumes a 5% fall:

The greatest change in earnings is displayed by WSA, AWC and PEM, with a 100% change in EPS for a US5¢ change in the A$. Albeit these companies have little to no earnings, which amplifies the sensitivity. Interestingly, BHP is slightly more sensitive to the A$ than Rio Tinto.

Weaker A$ could drive EPS upgrades and improved equity performance

A weaker A$ would drive upgrades to consensus earnings for the miners, as consensus A$ for CY 13/14 is US$1.04/US$1.00. Therefore we should expect that Resource equities to outperform in an EPS upgrade environment. However, we also need to consider the reason for A$ weakness; that being the possible winding back of QE and weaker commodity prices. Both may weigh on equity performance. We retain our preference for the high quality diversified names.

That’s spot on. But even diversified names are risky. Almost half of BHP’s revenue comes iron ore and the margins are huge so the impact on profit is even greater.

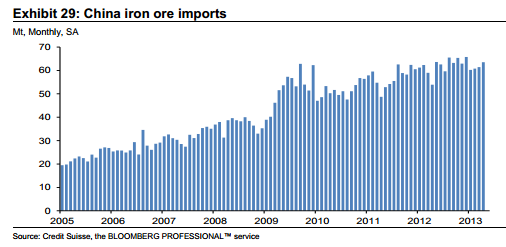

Moreover, rightly, Credit Suisse is advising ongoing bearishness on bulks, especially iron ore:

Advertisement

China’s April iron ore imports, after seasonal adjustment (sa), rose 3.4% mom to 63.5 Mt. In our view, this reflects the

anticipated increase in availability of seaborne supply rather than any particular strengthening of demand.

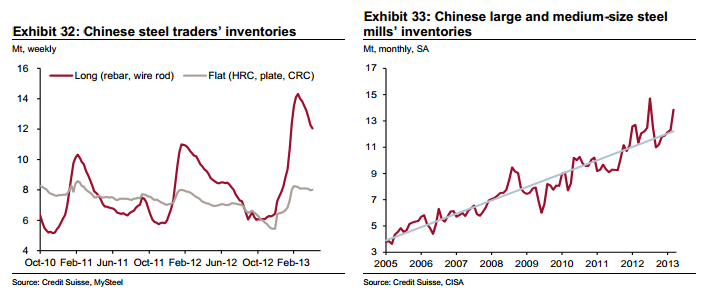

…the build of finished steel inventories in both the hands of traders and at the mill suggests that crude steel production has been running ahead of underlying demand. With such an inventory stockpile, we see little reason to believe that mills will not reduce run-rates, and hence their actual iron ore demand, as we move into the second half of the year:

CS’s long term forecasts are for a steady decline from a $125 average this year to $100 next year and $90 every year after that.

Even allowing for 10% volume growth, the Australian dollar will need to fall below 80 cents to offset that downdraft.

Advertisement

And that does not account for pressure on thermal and coking coal either.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.