Over the weekend China released its May data dump and the news is good if you’re looking to see a Chinese rebalancing and bad if you’re Australian.

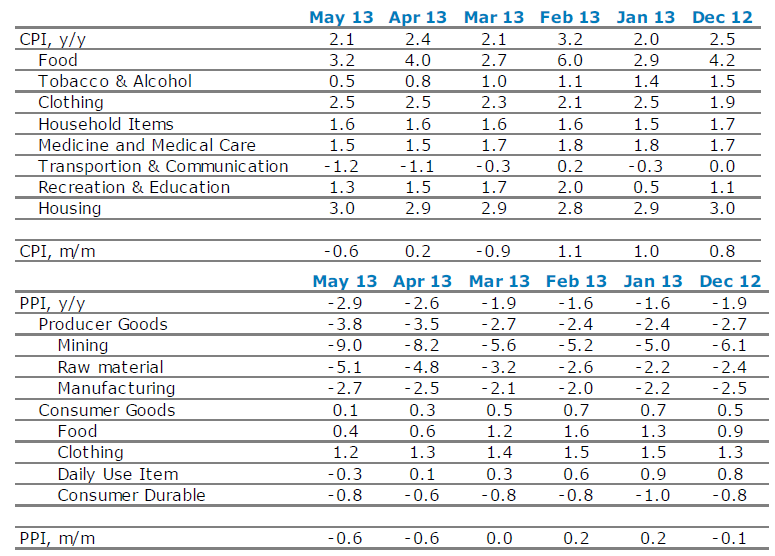

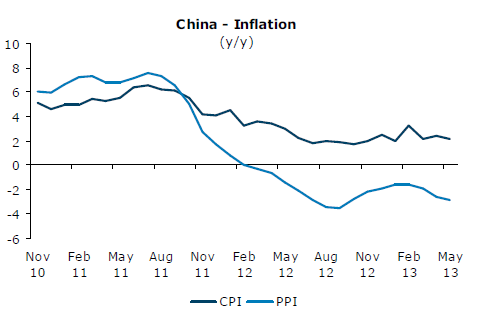

Starting at the top, inflation came in weak and well below expectations at -0.6% MoM and 2.1% YoY for the CPI. Good news perhaps but more concerning the PPI accelerated downwards at -0.6 MoM and -2.9 YoY (all charts and data thanks to ANZ):

You may recall that sharp falls in the PPI presaged China’s second half weakness for 2011 and 2012:

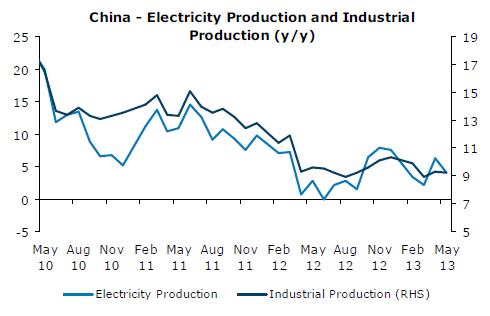

Next up, the composition of growth was positive for rebalancing but not so much for Australia. Industrial Production fell to 9.2% YoY in May, from 9.4% in April and electricity production confirmed the weakness, falling back to 4.1% from 6.2% in April:

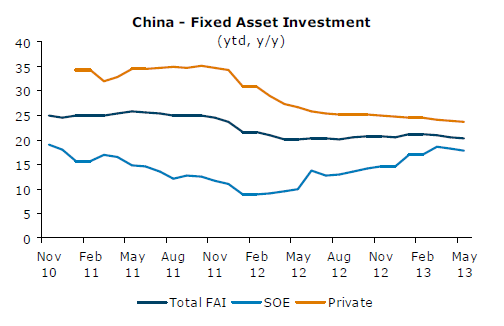

The all important (to Australia) fixed asset investment fell 0.2% to 20.4% YoY, resuming a gentle downtrend and the key component of strength, state spending, appears to rolling over:

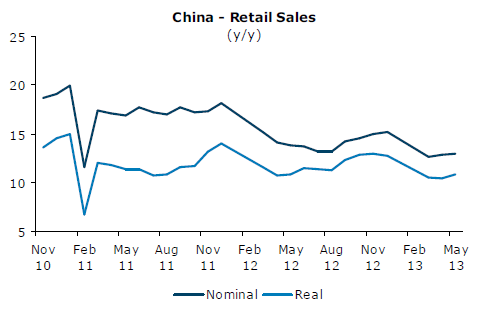

Retail sales grew a little faster up 0.1% YoY to 12.9% to suggest some rebalancing:

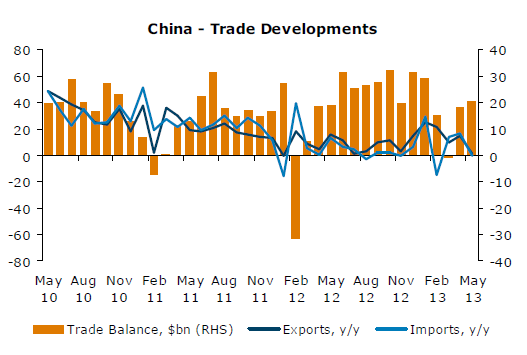

But trade data literally collapsed as authorities cracked down on dodgy invoicing. Exports growth crashed 1.0% YoY in May, compared with market expectations of a 7.4% and in increase of 14.7% in April. Import growth declined by 0.3% YoY in May, compared with 16.8% in April and the market consensus of 6.6%. The trade surplus widened to USD20.4bn in May, from USD18.2bn:

Finally, lending data collapsed as well in May with new loans at RMB667.4bn, miles below consensus and April’s RMB792.9bn. More importantly, total social financing, which includes shadow bank lending, was RMB1.19trn in May, down a stunning 32% from April’s RMB1.75trn. M2 still grew a respectable 15.8% YoY, 0.3ppt lower than last month.

We might again see this as good thing for rebalancing as shadow banking slows dramatically but it is clearly also a challenge to growth.

In fact, that is how I would characterise all of this data which points to the Chinese economy slowing to 7% sooner rather than later. And perhaps below for while if the slow down become self-fulfilling. I can’t see how any of this data supports anything other than further declines in commodity prices and Australia’s terms of trade.

Here is how Phat Dragon describes it:

The recovery has been consistently challenged in the year to date by stop-start investment spending, an end to the inventory rebuilding phase and soft external demand, which took a material turn for the worse in May.

The majority of the data flow has underwhelmed through March, April and May. The exceptions from earlier in the year – exports (over-invoicing), housing sales (a flurry ahead of tightening), new credit (likewise, plus heavy refinancing), railways (as expected) and manufacturing investment (curious) – all levelled out or decelerated in May.

Non-food consumer inflation remains relatively low and stable, while producer prices are softening anew. Policy is a heavy influence on many areas of the economy at present: SAFE and CBRC controls are driving tight interbank liquidity and a swift unwinding of disguised capital inflow, which in turn distorts the FX market; housing controls are slowing turnover; and credit data are showing signs of easing from the pace seen in Q1.

Phat Dragon maintains his basic views that

a) A low ceiling recovery-expansion remains in place, leaving one feeling a bit hollow.

b) Growth, such as it is, is likely to plateau quite soon, consistent with the degree of policy accommodation having levelled off since late last year.

c) The clear intent of the authorities to limit the upside has prevented a more durable upswing. Even so, with CPI under control, and external pressures dragging on growth, there is little need to move to a more overt tightening posture.

And his chart pack:

Phat_Dragon_the_chart_pack_June_2013.pdf by Sarah Crawford