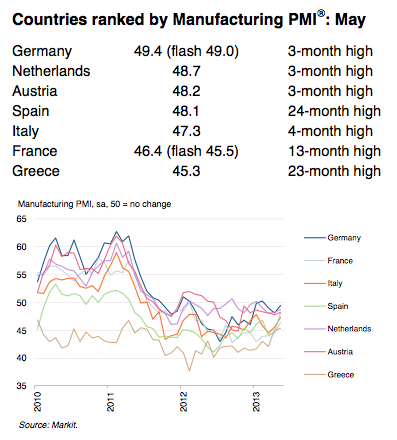

Manufacturing data was out in Europe overnight with again some upside:

- Final Eurozone Manufacturing PMI at 48.3 in May (flash:47.8)

- Downturns ease in all nations covered

- Price deflationary pressures remain, as input costs and output prices fall further

The eurozone manufacturing downturn eased for the first time in four months in May. Moreover, all sub-indices from the latest survey improved on the earlier flash estimates except suppliers’ delivery times. At a 15-month high of 48.3 in May, up from April’s four-month low of 46.7, the

seasonally adjusted Markit Eurozone Manufacturing PMI indicated the slowest pace of contraction since February 2012.Business conditions still deteriorated overall, however, with the current downturn extended to a twenty-second month. PMIs for all of the nations covered by the survey signalled weaker rates of contraction in May.

The German PMI signalled the slowest rate of contraction overall and moved close to the stabilisation level as output and new orders both rose for the first time in three months. Downturns in the Netherlands and Austria were also only moderate.

Are we finally seeing some good news out of the Eurozone? Yes and no. Firstly, although these numbers are monthly highs across the board not one single country managed to register an expansion.

Yes, manufacturing appears to be bottoming out, at least in the short term, as demand for export goods picks up in a number of periphery nations, however, as we saw from the latest unemployment figures and has also been backed up by service PMI data, much of the gain in the export sector is coming at the expense of internal demand.

As can be seen in places like Spain the services components of the composite index are still falling, so although we are seeing a recovery in manufacturing and a move towards current account surpluses, quite a lot of that is to do with the lowering of internal demand, and therefore imports, with the overall result being a continuation of the loss of jobs and deflationary pressure on the economy.

It should also be noted that the PMIs don’t take into account the relative size of the economies being compared with the two biggest economies outside of Germany, France and Italy, still deeply in contraction even with these latest improvements.

More from Markit’s chief economist:

Although the euro area manufacturing economy continued to contract in May, it is reassuring to see the rate of decline ease to such a marked extent. The sector still seems some way off stabilising, however, and therefore remains a drag on the economy.

Despite the final PMI coming in above the flash reading, the surveys still suggest that GDP is likely to have fallen 0.2% in the second quarter, extending the region’s recession into a seventh successive quarter.

Policymakers will nevertheless be pleased to see the downturn not getting any worse, suggesting the ECB will see no immediate need for further action at its June meeting. In particular, the surveys brought good news in terms of signs of stabilisation in Germany and export-led growth in Italy and Spain, the latter suggesting structural reforms are boosting competitiveness.

France remains a key concern, having contracted at a steeper rate than Spain and Italy throughout the year so far. The ongoing marked fall in

employment and the steepest drop in factory gate prices for three-and-a-half year also act as sobering reminders that the region faces the twin problems of unemployment rising to new record highs and underlying deflationary pressures.

So a mixed bag.

That’s not to say that this isn’t good news in terms of re-balancing. As I have stated over the last month, Germany does appear to be letting domestic inflation off the leash more than they have in the past and this again should hopefully shift the import/export balance towards the periphery and therefore help in this adjustment. I do fear, however, that some of this may just be political rhetoric in the lead-up to September elections in Germany, which is why I still believe we need to wait until Q4 2013 to get the true state of the fiscal policy direction of the zone into 2014.

Full Eurozone PMI report below.