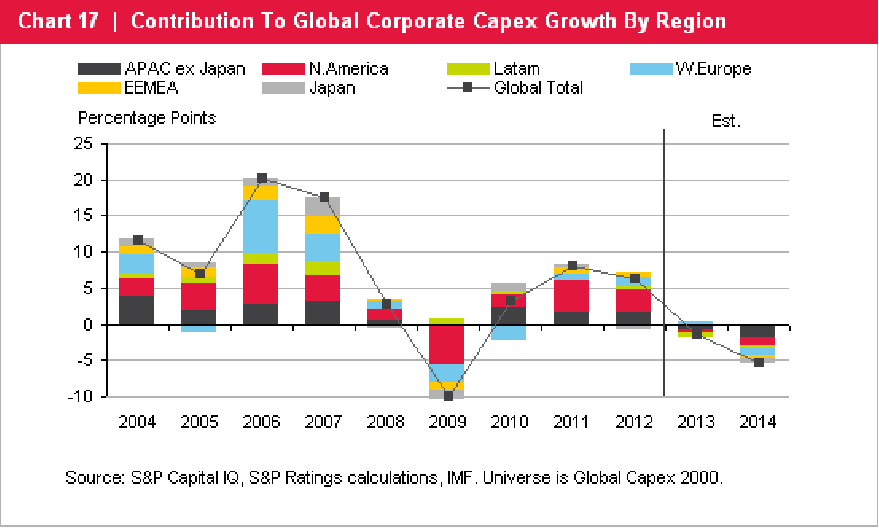

S&P has released a global capex report that shows the next few years are unlikely to be as kind as the last few as the commodities super-cycle passes. Here is the chart:

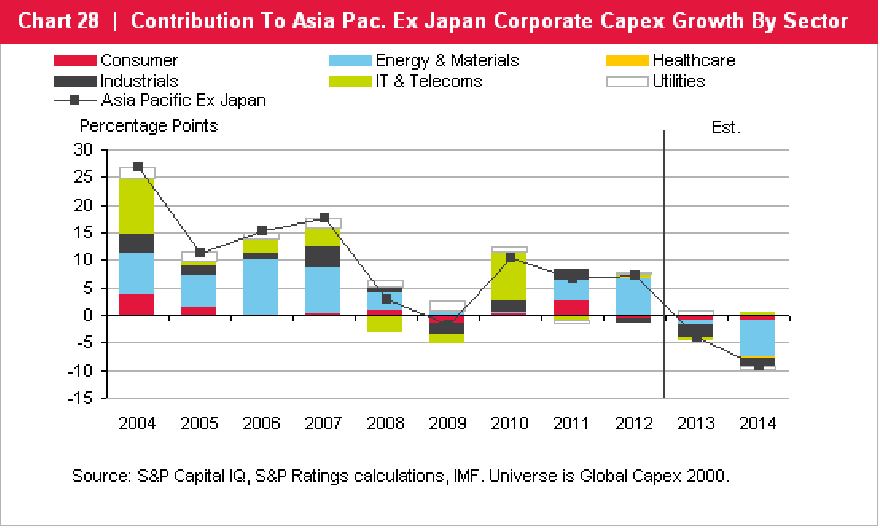

More concerning is the capex forecast for the Asia Pacific, which is not promising:

A final surprising element of our regional capex trend analysis is the weakness apparent in Asia-Pacific. The reversal of capex growth in the energy and material sectors is-–as with other regions-–part of the story (see chart 28). But there appears to be downward pressure on industrial capex, too, and little sign of the strongly positive contribution from IT and telecoms that has been a feature throughout most of the past decade.

Advertisement

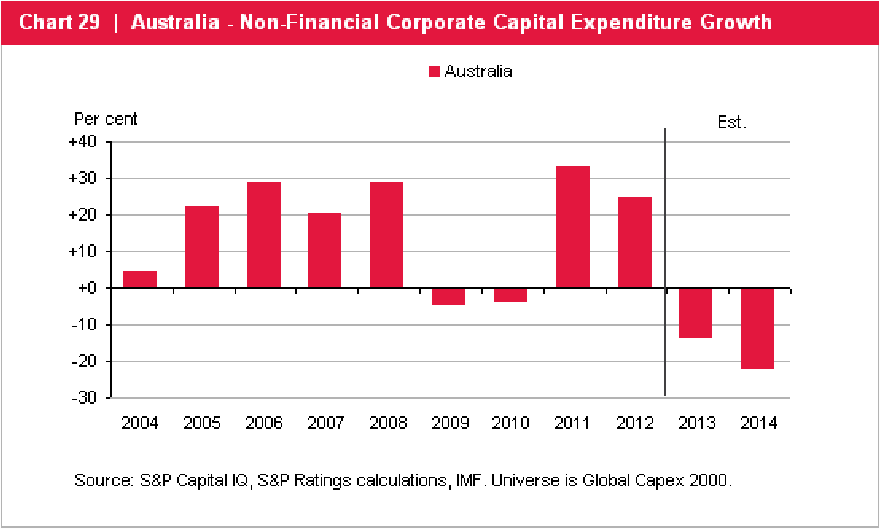

And outright eye-popping is the forecast for Australia:

The fact that the commodity “super cycle” has, at the very least, paused for breath is a major factor explaining negative capex expectations for 2013-2014. This is best illustrated by the capex outlook for Australia, which is central to emerging Asia’s energy nexus. Here, the scaling back of mining investment is projected to bring an abrupt reversal of the strong capex growth seen in 2011-2012 (see chart 29). Current estimates suggest a decline in capex in real terms of 12% in 2013 and more than 20% in 2014, caused primarily by a sharp reduction in investment intentions by the major mining corporations. These growth rates, if realized, would be the worst capex growth figures for Australia in the 10-year period for which we have data, exceeding the downturn that followed the financial crisis.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.