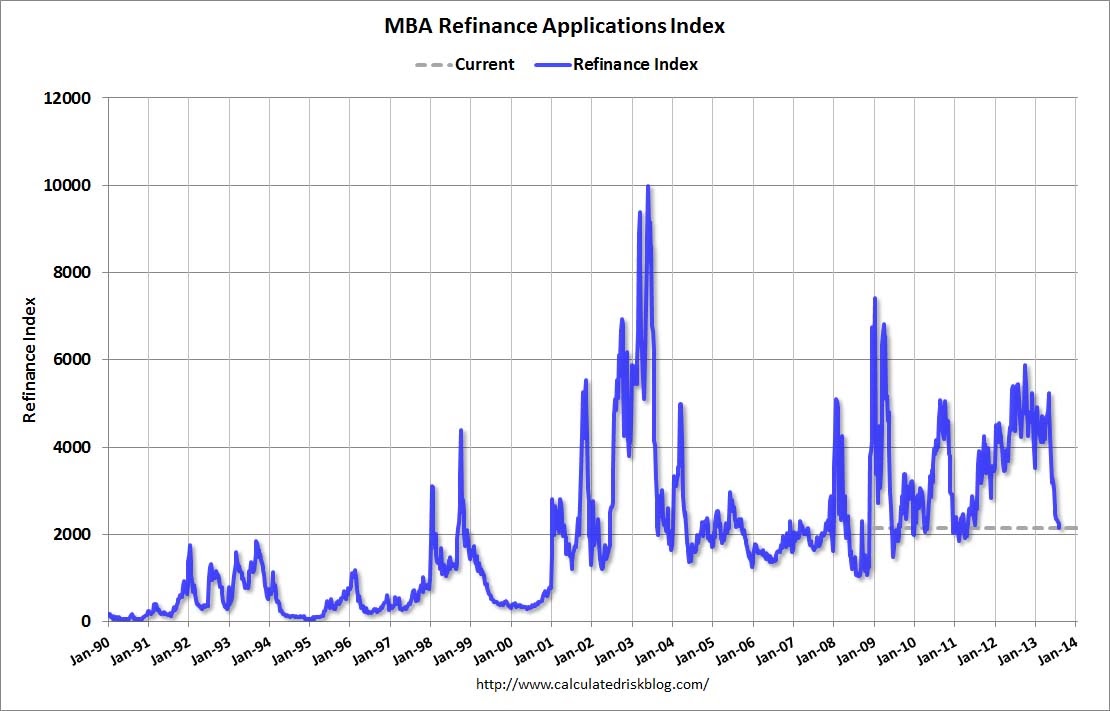

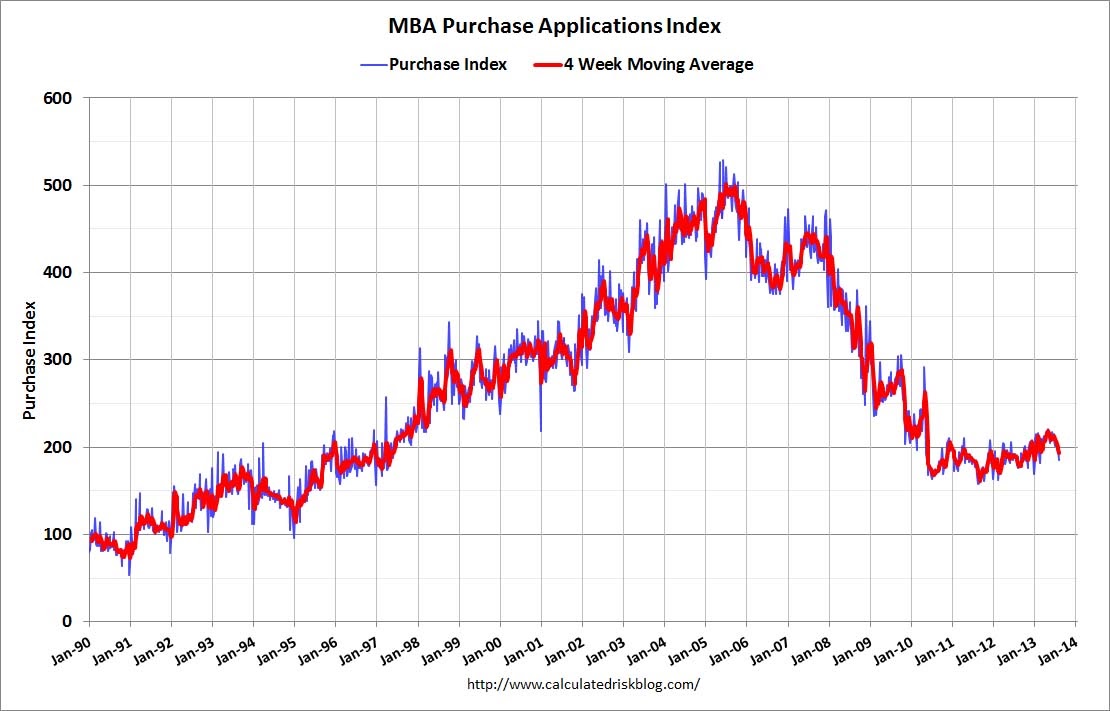

Last night markets appeared to embrace more taper prospect. However the data was not favourable. It is now quite clear that the US mortgage market has turned sharply on the taper inspired spike in bond yields and hence mortgage rates. From the Mortgage Bankers Association:

Mortgage applications decreased 4.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 9, 2013. … The Refinance Index decreased 4 percent from the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. … The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) decreased to 4.56 percent from 4.61 percent, with points decreasing to 0.39 from 0.42 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. … The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.60 percent from 3.66 percent, with points decreasing to 0.35 from 0.43 (including the origination fee) for 80 percent LTV loans.

As usual, Calculated Risk has the charts:

Remember that US house prices actually track the refinancing index quite closely so I expect price gains are likely to slow sharply in the not too distant future, slowing consumption as well, although the new construction wave will proceed. Nonetheless, the 30 year bond is sitting right at the top of its recent range with yields at 3.75%.

Also weighing against any imminent taper were producer prices, which were unchanged on the month and sit at 2.1% year on year.

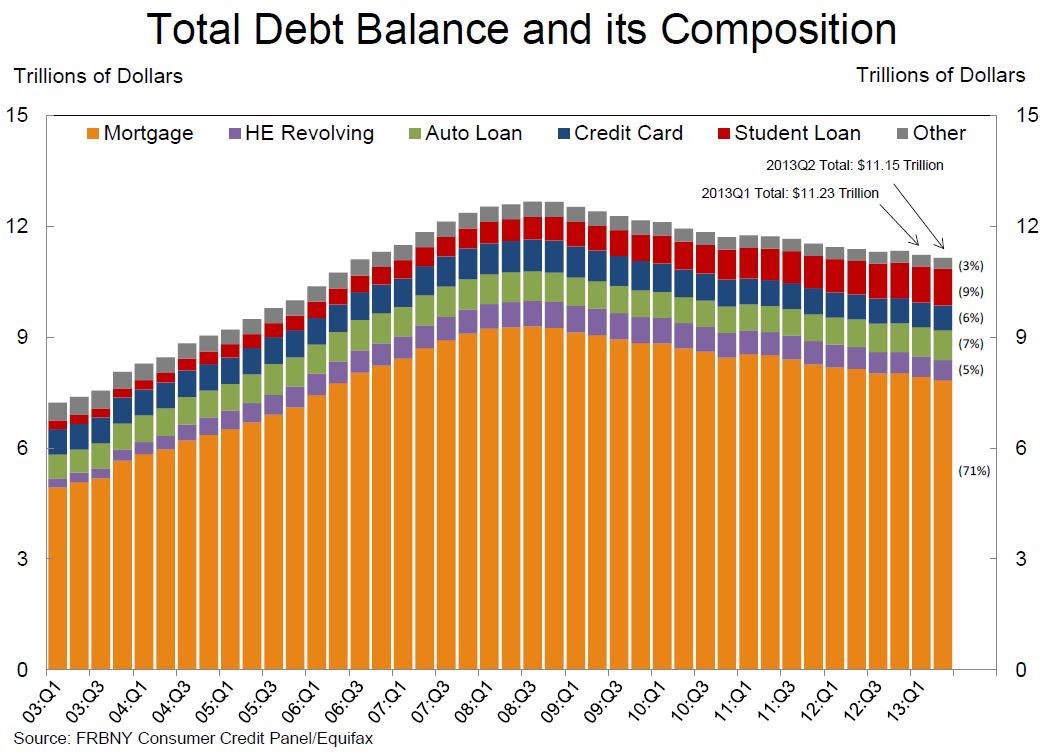

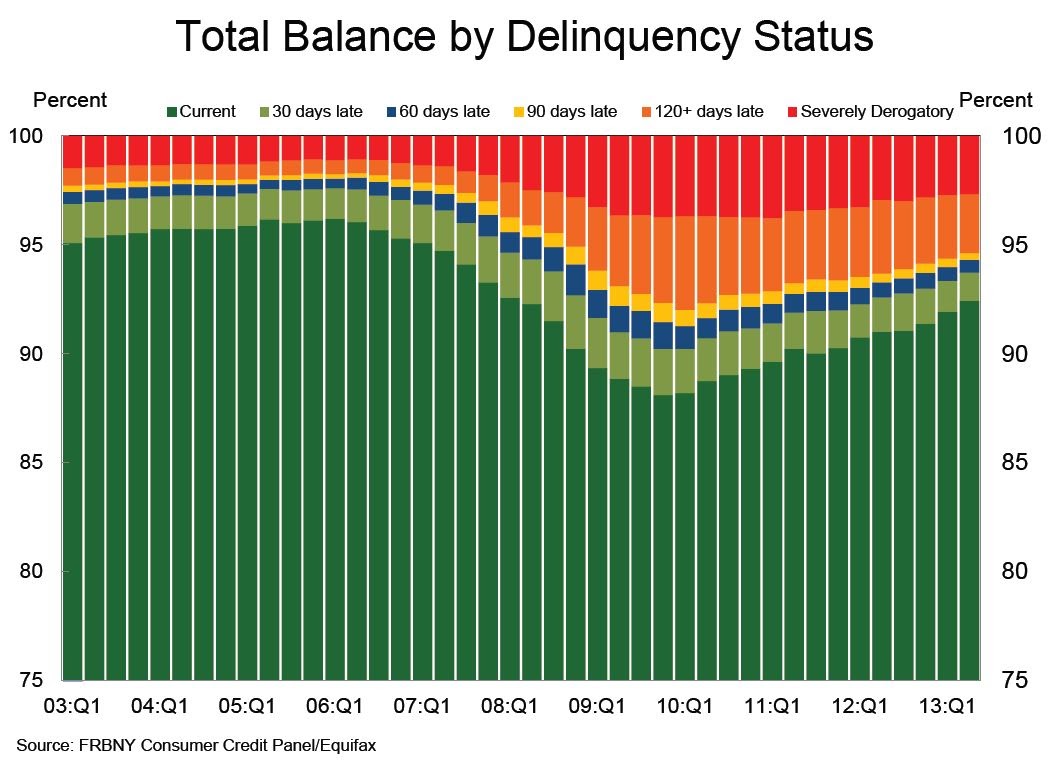

Rounding out our evening’s data, despite the recent surge in mortgage debt, US households continue to deleverage, according to the Fed:

The Fed told us it was going to taper to prevent excessive leverage building up as the cycle accelerated. It is succeeding but growth is not going to accelerate as a result.