Citibank has an impressive note out on the future of Chinese coal usage and the news for Australia is good and bad. Good because carbon emissions are going to fall. Bad because our coal exports face a lot more potential downside:

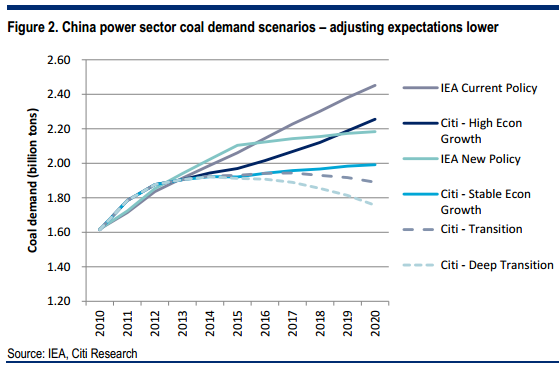

For the last decade, one of the most unassailable assumptions in global energy markets has been the ever-increasing trajectory of Chinese thermal coal demand. The consensus outlook for China’s coal demand, which currently accounts for more than 50% of global demand, has been so strong that the IEA called for coal to surpass oil as the leading global fuel before 2030.

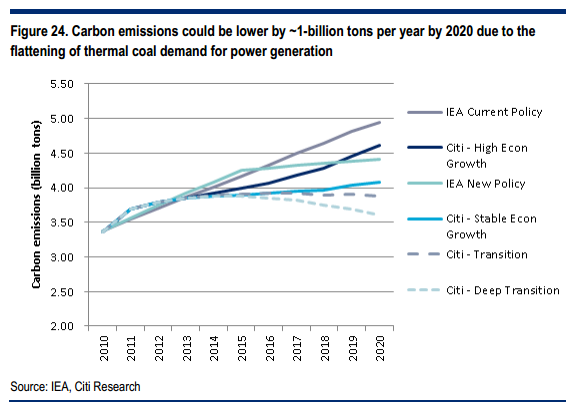

Beyond the possibility of peak thermal coal demand in China, a series of transformative forces are increasingly asserting their influence on the global power mix. Disruptive changes in technology costs and fuel markets are now set to ensure that the next ten years look little like the last twenty. US shale gas is just the beginning. Changes in the power mix, especially in Chinese coal demand, have serious ripple effects on three categories: (1) globally traded coal and commodities, (2) countries and companies reliant on coal production and (3) carbon emissions.

Significant shifts in China’s economic structure and power sector demand a reassessment of coal’s perpetual climb. Key drivers include: (1) reduction of air pollution; (2) structural downward shifts in China’s GDP growth and energy intensity; (3) robust growth of China’s renewables and nuclear capacity, along with increased availability of natural gas from pipeline/LNG imports and domestic production; (4) efficiency improvements in coal power plants and energy demand.

Citi expects this combination of factors to slow the power sector’s use of coal, pointing to a possible flattening or peaking before 2020, although many global energy agencies continue to expect high coal demand in the years to come. We arrive at our results based on a detailed, top-down electricity supply-demand model for China, which factors in power demand, efficiencies, coal and non-coal power generation and capacity, among others. The same macro forces driving the economic transition and lowering power demand should also lead to a deceleration in coal’s use in other sectors. Our conclusions are supported by results from bottom-up, economy-wide analyses by the China Energy Group at the Lawrence Berkeley National Laboratory. Senior research staff at China’s National Development and Reform Commission suggested the possibility of peak coal demand by 2015. Further, our work builds on Citi’s extensive research on China’s transition and on the end of the supercycle in commodities and the mining sector.

As the range of forecasts for Chinese coal demand is wide, we believe investors should price in higher probabilities of lower coal demand. Optimistic long-dated coal prices may be unsupported. Although lower prices may spur demand growth elsewhere, the demand slowdown in China should more than offset such gains, in our view. Coal exporting countries that have been counting on strong future coal demand could be most at risk. The end of the supercycle should weigh on both the mining and equipment sectors. But sectors that excel at renewable integration, distributed generation, transmission could benefit the most.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.