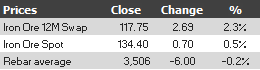

Find below the iron ore price table for October 17, 2013:

Word of the day: breakout!

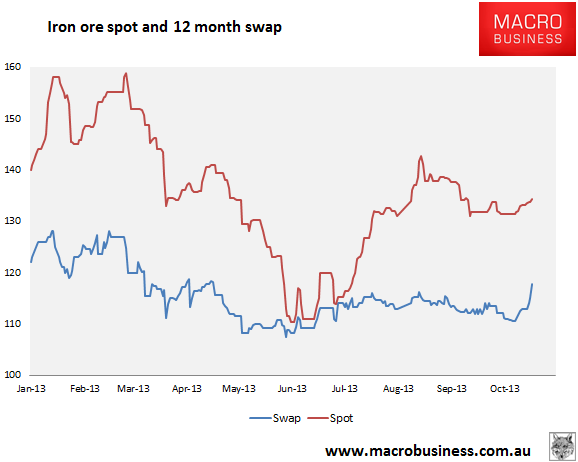

The reason I include 12 month swaps in this missive is they have a strong correlation with spot, usually leading. Yesterday it broke out spectacularly with spot also looking firm:

In technical terms we’ve quickly morphed from a bearish head and shoulders top to bullish and rather large inverted head and shoulders bottom. The neckline is not broken but it’s something to watch.

There are two ways to read this. First, the 12 month might be signalling a shift in the longer term pricing of iron ore. The recent strength despite rising supply might be convincing the market that futures prices are under done. The other rationale, the one I favour, is that the 12 month is signalling that the window for Chinese seasonal weakness is passed and the Q4 restock pulse is imminent. (As a quick aside Dalian iron ore futures debut today but I can’t see why that would be a factor).

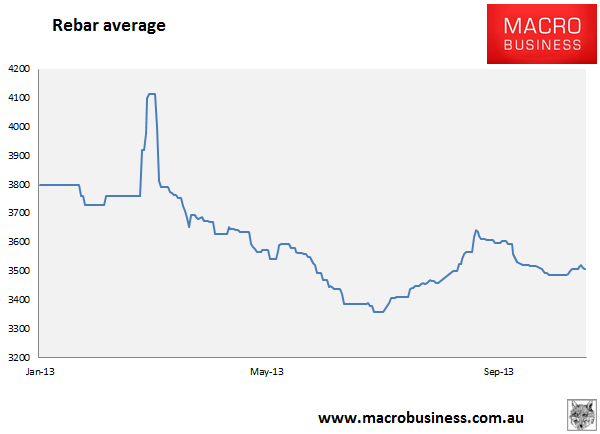

In that event it really doesn’t matter that steel prices are weakening:

Futures were even weaker. But if the restock is on the who cares!

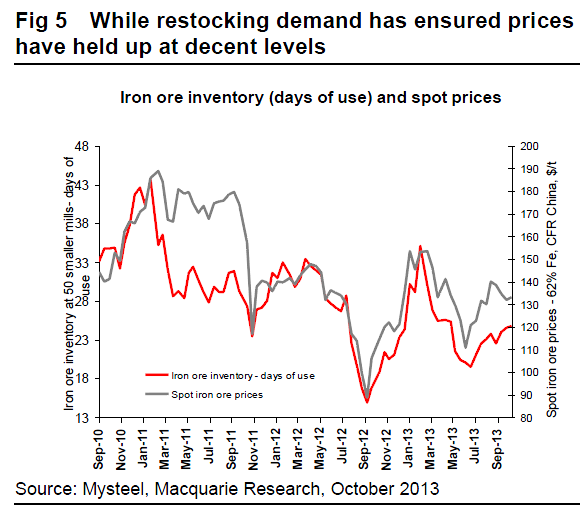

Chinese mill ore inventories are well above last year’s Q3 lows. From Mac Bank:

But they are also well below last year’s January highs. Steel inventories at mills are still seasonally high but there is nothing in the economic environment to suggest the demand matrix is about to change so I would expect the restock to still take place. The drivers of it are manifold: Australian cyclone season; Chinese weather patterns for construction and holiday seasons etc. The November plenum might an issue but at this stage it seems unlikely to be of concern. Every year Q1 steel production leaps so next year will surely be the same.

With the supply deluge beginning, mills may elect to rebuild stocks less dramatically that last year but it’s fair bet it will still be decent and with the price already high, a decent price spike is not out of the question.