Snippets of information received in recent weeks have again raised concern over whether the Australian economy has become more structurally imbalanced, raising the likelihood of a disorderly unwind down the track.

The news that Holden is likely to join Ford in ceasing its Australian car production from 2016, along with the recent closure of the Electrolux refrigerator factory in Orange and today’s announced closure of the Qantas heavy maintenance base at Avalon, is set to place further pressure on Australia’s manufacturing sector, which already looks to be in terminal decline, with the total number of people employed in manufacturing and the industry’s employment share falling sharply over the past 30-years just as manufacturing capital expenditures are at an all time low:

Then there is today’s news that a quarter of scientists, researchers and workers at the CSIRO will lose their jobs under the federal government’s public service jobs freeze, with the end result likely to be a meaningful diminution of Australia’s scientific skills base.

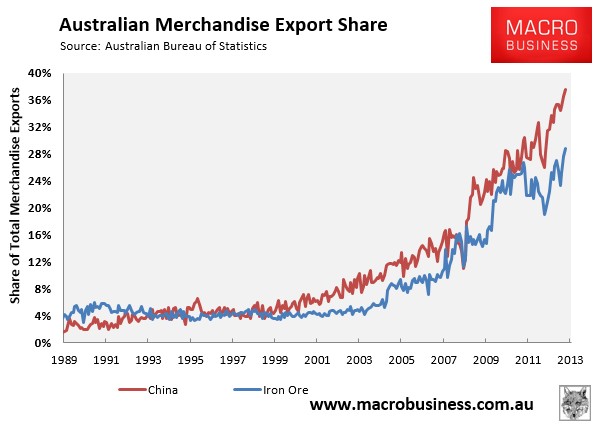

Offset against these losses is this week’s trade data, which showed both exports to China and iron ore exports hitting a record high share (see next chart).

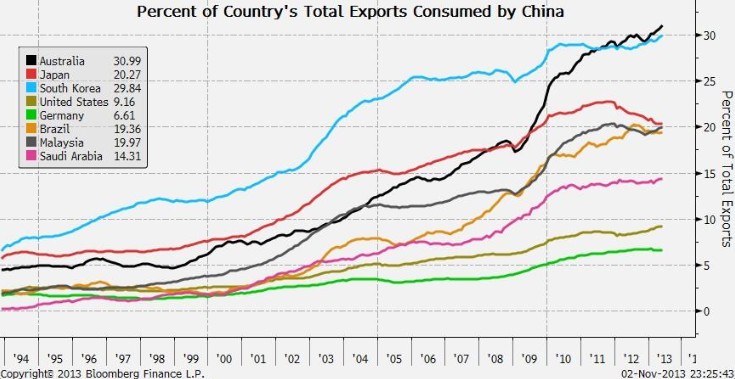

As shown recently by Bloomberg’s Michael McDonough, there is no other significant economy in the world as dependent on exports to China:

While all will remain fine as long as Chinese demand for Australian commodity exports remains voracious, we risk a protracted downturn in the event that China’s economy slows unexpectedly and/or it rebalances abruptly away from investment-led growth.

While it may not seem apparent at the moment, given the cyclical bounce from record low interest rates, the risks facing the Australian economy are growing from an increasing lack of diversification and heightened dependence on one sector (construction) of one economy (China).