McKinsey Global Institute has produced an in-depth document that states the obvious on the affects of QE and the likely problems with its withdrawal.

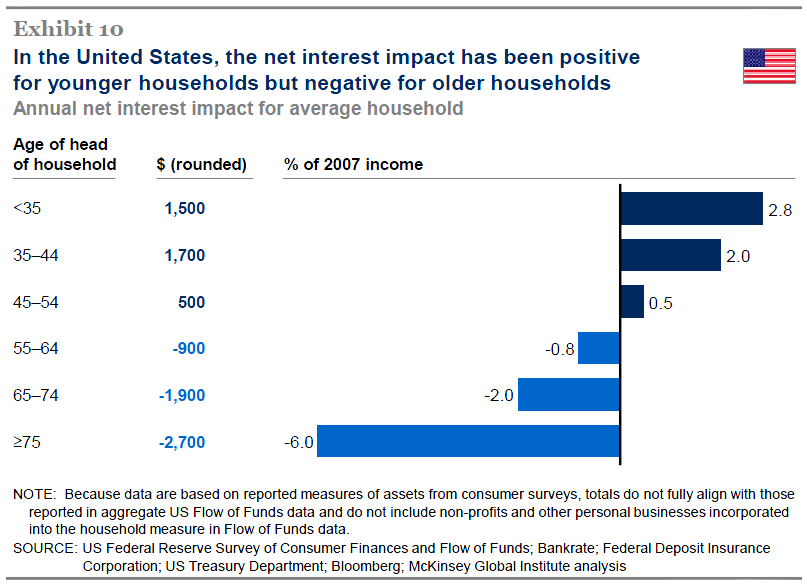

Between 2007 and 2012, ultra-low interest rates produced large distributional effects on different sectors in advanced economies through changes in interest income and interest expense. By the end of 2012, governments in the United States, the United Kingdom, and the Eurozone had collectively benefited by $1.6 trillion, through both reduced debt service costs and increased profits remitted from central banks. Meanwhile, households in these countries together lost $630 billion in net interest income, with variations in the impact among demographic groups. Younger households that are net borrowers have benefited, while older households with significant interest bearing assets have lost income. Non-financial corporations across these countries benefited by $710 billion through lower debt service costs.

The era of ultra-low interest rates has eroded the profitability of banks in the Eurozone. Effective net interest margins for Eurozone banks have declined significantly, and their cumulative loss of net interest income totaled $230 billion between 2007 and 2012. In contrast, banks in the United States have experienced an increase in effective net interest margins as interest paid on deposits and other liabilities has declined more than interest received on loans and other assets. From 2007 to 2012, the net interest income of US banks increased cumulatively by $150 billion. Over this period, therefore, there has been a divergence in the competitive positions of US and European banks. The experience of UK banks falls between these two extremes.

Life insurance companies, particularly in several European countries, are being squeezed by ultra-low interest rates. Those insurers that offer customers guaranteed-rate products are finding that government bond yields are below the rates being paid to customers. If the low interest-rate environment were to continue for several more years, many of these insurers would find their survival threatened.

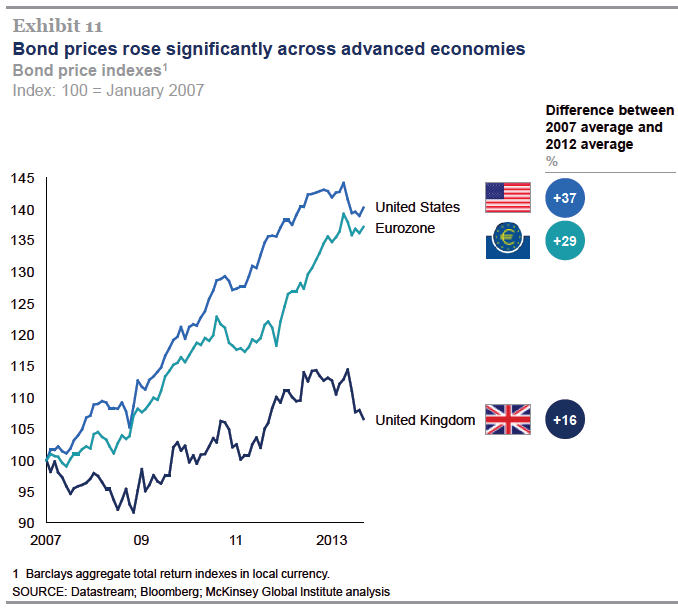

The impact of ultra-low rate monetary policies on financial asset prices is ambiguous. Bond prices rise as interest rates decline, and, between 2007 and 2012, the value of sovereign and corporate bonds in the United States, the United Kingdom, and the Eurozone increased by $16 trillion.

But we found little conclusive evidence that ultra-low interest rates have boosted equity markets. Although announcements about changes to ultra-low rate policies do spark short-term market movements in equity prices, these movements do not persist in the long term. Moreover, there is little evidence of a large-scale shift into equities as part of a search for yield. Price-earnings ratios and price-book ratios in stock markets are no higher than long-term averages.

Ultra-low interest rates are likely to have bolstered house prices, although the impact in the United States has been dampened by structural factors in the market. At the end of 2012, house prices may have been as much as 15 percent higher in the United States and the United Kingdom than they otherwise would have been without ultra-low interest rates, as these rates reduce the cost of borrowing. We based this estimate on academic research using historical data that suggest how housing prices rise as interest rates decline. In the United Kingdom, it is plausible that this relationship holds today. However, in the United States, it is unclear whether the historical relationship between interest rates and housing prices holds today because of an oversupply of housing and tightened credit standards.

If one accepts that house prices and bond prices are higher today than they otherwise would have been as a result of ultra-low interest rates, the increase in household wealth and possible additional consumption it has enabled would far outweigh the income lost to households. However, while the net interest income effect is a tangible influence on household cash flows, additional consumption that comes from rising wealth is less certain, particularly since asset prices remain below their peak in most markets. It is also difficult today for households to borrow against the increase in wealth that came through rising asset prices.

We should point out that other factors are also at work here beyond just low interest rates.

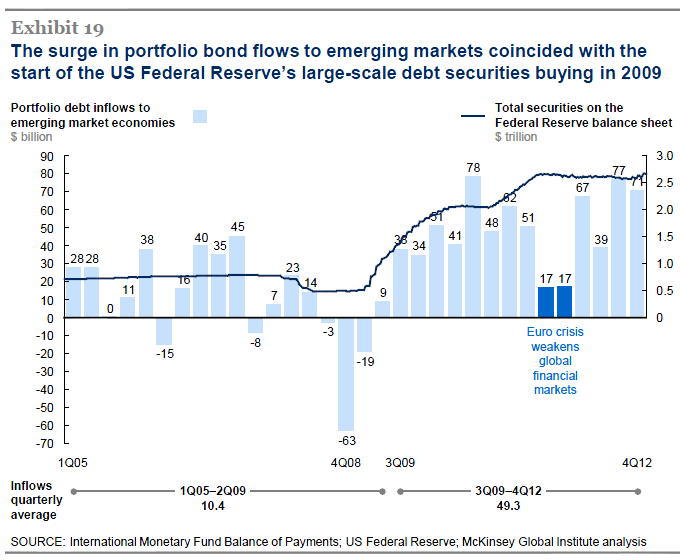

Ultra-low interest rates appear to have prompted additional capital flows to emerging markets, particularly into their bond markets. Purchases of emerging-market bonds by foreign investors totaled just $92 billion in 2007 but had jumped to $264 billion by 2012. This may reflect a rebalancing of investor portfolios and a search for higher returns than were available from bonds in advanced economies, as well as the fact that overall macroeconomic conditions and credit risk in emerging economies have improved. In some developing economies, including Mexico and Turkey, the percentage increases in capital inflows into bonds have been even larger. Emerging markets that have a high share of foreign ownership of their bonds and large current account deficits will be most vulnerable to large capital outflows if and when monetary policies become less accommodating in advanced economies and interest rates start to rise.

All pretty obvious stuff for someone not living under a rock. Financial repression benefits speculators and governments. The hesitance on stock price isn’t necessary. Anyone watching QEs 1 through 3 knows that share price go up when the Fed prints. That valuation multiples haven’t broken from long term averages simply implies that without QE they’d be a lot lower in a low growth environment.

Anyways, as you’d expect, reversing QE will spike peripheral bond yields, spike equity market volatility and raise debt servicing costs for households as well as pressure house prices. Which is why it’s going to happen ultra-slowly.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.