First, the correlation between commodity and other asset price changes was near 20 per cent in the 1980s and 1990s. Commodities were better placed to diversify investment portfolios and hedge against risk. Today, however, the correlation is closer to 60 per cent. During the financial crisis, when markets plunged and investors most needed uncorrelated assets, commodities printed a peak-to-trough fall of almost 55 per cent, compared with less than 45 per cent for equities.

Second, price movements in individual commodities have also exhibited correlations with more mainstream assets. Over the past few years, for instance, gold has been correlated with equities and more recently with treasuries, as a result of gold’s changing reaction to quantitative easing, or QE. First, gold reacted positively to QE due to concerns that the latter might cause inflation. But more recently any hint from the US Federal Reserve that it will scale back QE has sent gold tumbling along with bond prices.

Third, while it may be true that commodities initially kept pace with US inflation after the US abandoned the gold standard in 1971, this effect only lasted for a decade. Prior to this, and during the 1980s and 1990s, commodities lost value when adjusted for inflation. It wasn’t until emerging market demand started pushing up commodity prices in the early 2000s that commodities began to make up lost ground.

Fourth, in the case of gold, investors will long remember 2013 as the year that their precious shiny metal ceased to be a safe haven. In April, gold plummeted 14 per cent in two days, including 9 per cent in a single day. And this was only the fifth largest one-day fall since the end of the gold standard. No asset with this kind of volatility should be considered safe.

Finally, putting history aside, our analysis suggests the outlook for commodities is bleak. At various points in recent years, loose central bank policy and fears of inflation have stoked commodity demand. Talk of tightening policy affects this in two ways.

First, commodities pay no income, unlike equities and bonds. When interest rates and incomes from financial assets rise, commodities will look less attractive. Second, the boom in the sector in the 2000s prompted investment in commodity supply.

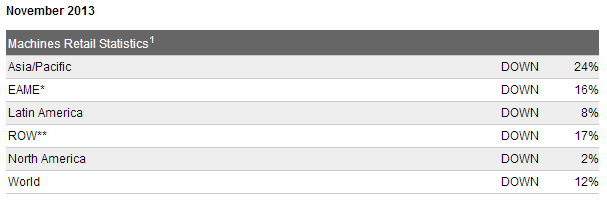

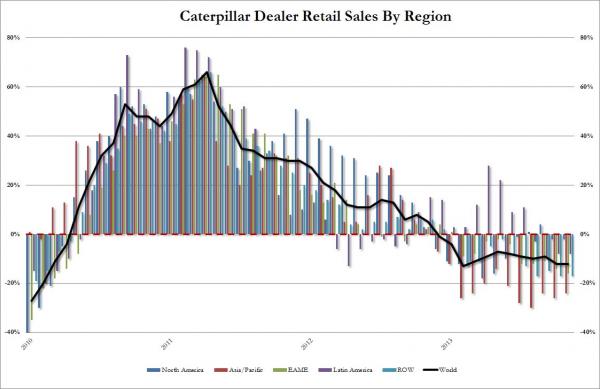

Quite right. I find the rise of supply an especially compelling argument for the medium term. The emerging markets story is probably alos waning as rebalancing becomes priority, though the markets themselves won’t. We can see the unfolding accident today again in Caterpillar’s overnight results:

This is the cost-out deflation trend I reckon is secular and will go on and on.

But it is not all bad news. In the longer run, there are reasons to think that the US dollar will remain challenged which will lend commodities (especially precious metals) longer term support.

The model for this is the Great Depression. In his epic work on the subject, Charles Kindleberger ascribed his number one cause of the depression not as debt, nor animal spirits, but geo-politics. He argued that the enduring nature of the challenge was the result of the decline of Britain and its empire, which was so swift that when challenged economically it was unable to respond with policies that could reverse the deflationary tide. And the rise of the US, which was too young to shoulder the responsibility of carrying demand as the old power waned. Thus, a breakdown in the responsibilities between nations meant nobody was able to rally global policy to a solution and the world disintegrated into internecine states.

While we probably have a better handle on such things today, as witnessed by the more effective global response to the GFC, the settings of a declining and rising superpower are eerily similar. It is in forex markets where this tension is most obvious and I do not expect that to be resolved any time soon.