The AFR is reporting that BP is mulling the sale of its two Australian oil refineries:

If BP, Europe’s second-largest oil and gas company which runs two of Australia’s six refineries, was to bite the bullet and formally appoint advisers, it may look towards its lending bank syndicate which includes Deutsche Bank and UBS.

The unconfirmed rumour doing the rounds is that BP has held back from $50 million of spending needed at its Bulwer Island refinery in Brisbane, seemingly confirming its lack of interest in throwing more money at the plants. The Brisbane plant has long been seen as a prime candidate to link up with Caltex’s Lytton plant, just 300 metres away, but no deal has yet been done.

BP’s Kwinana refinery in Western Australia is better placed competitively but faces the same broader difficulties.

Credit Suisse estimates Caltex’s refining losses reached about $150 million this year, signalling BP’s losses may be similar.

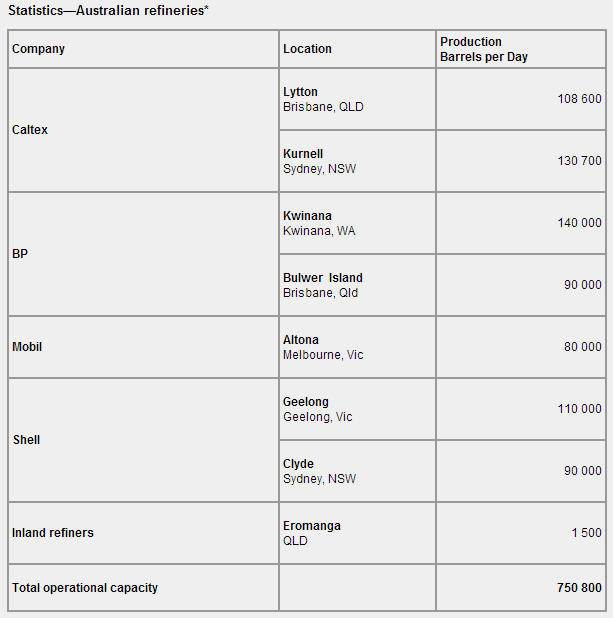

Here is the list of current and former Australian refineries:

Kurnell and Clyde are already shut. Geelong is for sale with no buyer. If BP adds its two refineries the prospects for any sale become more dubious and more closures loom.

The implications are straight forward. From the FT last year:

Australia consumes about 1m barrels a day of oil-refined products – on a par with a medium-sized European country such as the Netherlands. If the country imports half of its fuel requirements, as Canberra is now forecasting, it could easily surpass Indonesia’s fuel purchases of about 400,000 b/d – the largest in Asia and one of the biggest worldwide.

In 2000, when there were eight refineries in Australia, only 5 per cent of fuel was imported – equivalent to less than 100,000 b/d. Fuel imports rose to nearly a quarter of total demand by 2010, or 320,000 b/d, as consumption increased and one refinery closed.

Soozhana Choi, chief oil strategist at Deutsche Bank in Singapore, says further consumption growth and the impact of closing the Shell and Caltex refineries, which will reduce the total number of plants to five, would push Australia’s imports of petrol, diesel, jet fuel and fuel oil to 640,000 b/d by 2015.

In short, we’re gutting our liquid fuels security as fast as we can.

Gimme another one of those big and far flung houses, matey. I can always drive to work!