The Chinese reform campaign has moved to a new phase. Over the past week, the project has moved from controlling interbank rates to the currency as the People’s Bank of China appears determined to both boost export sectors and rid its economy of the hot money flows that are underpinning shadow bank excess.

The yuan fell 1.3% against the dollar last week, which is very steep in context. There are three theories about what’s going on. The first is that the PBOC is preparing markets for a float and also does not want to see the yuan higher than it is because of concerns about competitiveness.

The FT’s Short View has a nice take on those theories:

I agree that this is partly behind the move. But there’s more.

The second theory is that the PBOC has so surprised markets that it’s lost control of the currency as hot money goes into full reverse. From Morgan Stanley:

In our previous note, we estimated that US$350 billion of TRF [Redemption Forward contracts]have been sold since the beginning of 2013. When we dig deeper, we think it is reasonable to assume that most of what was sold in 2013 has been knocked out (at the lower knock-outs), given the price action seen in 2013.

Given that, and given what business we’ve done in 2014 calendar year to date, we think a reasonable estimate is that US$150 billion of product remains.

Taking that as a base case, we can then estimate the size of potential losses to holders of these products if USD/CNH keeps trading higher. In round numbers, we estimate that for every 0.1 move in USD/CNH above the average EKI (which we have assumed here is 6.20), corporates will lose US$200 million a month. The real pain comes if USD/CNH stays above this level, as these losses will accrue every month until the contract expires. Given contracts are 24 months in tenor, this implies around US$4.8 billion in total losses for every 0.1 above the average EKI.

That is, the PBOC has, or is close to, triggering a run of leveraged hot money out of bets on a rising yuan. There may be some truth to that but if it were a sign of outright capital flight then Chinese interbank rates would also be headed for the moon and they’re not (though they’re rising). Also from the FT:

“My guess is that this is deliberately engineered, it is not an accident since they have managed the process of appreciation extremely well. But the amount of things going on in China means it is very difficult to interpret,” says George Magnus, a senior adviser at UBS.

“It’s very different from June. If it’s the financial system crashing, you should see interbank rates moving higher,” says Wei Yao, China economist at Société Générale. Current interbank lending rates are at their lowest in almost 12 months, and have fallen sharply since the start of the year. “It is intervention from the central bank,” Ms Yao adds.

I agree and think that the “lost control” brigade have it backwards. The PBOC is not concerned about outflows, it’s trying to prevent inflows. This is the key point that most are missing. Also from the FT:

Speculative inflows into China had shown signs of accelerating as the renminbi continued to rise, until last week, while other emerging market currencies were falling sharply. Banks bought a monthly record of $73bn of foreign currency in the onshore market from their clients who wanted renminbi in January, according to data published this week by the central bank.

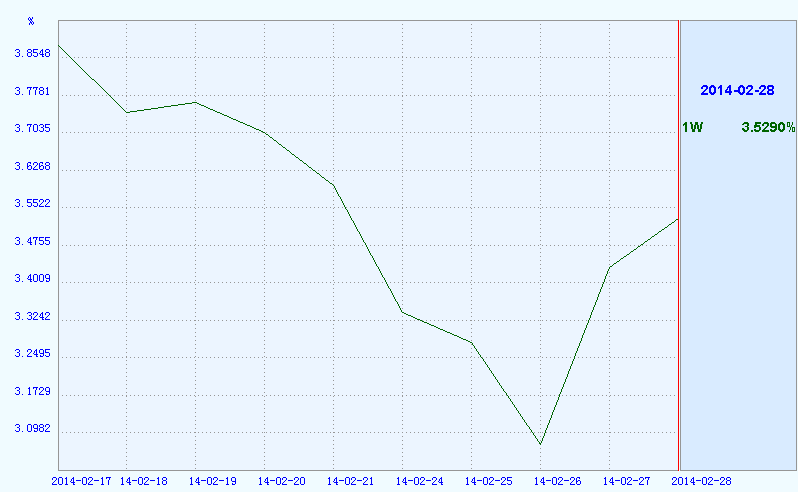

In short, the PBOC does not want to see its domestic tightening circumvented by international “hot money” flows into banks and, perhaps even more so, shadow bank products. I don’t think it wants to tighten like mad but it does not want to loosen either. Interbank markets have responded accordingly. The post-Chinese New Year liquidity burst has reversed nicely in the past three days. Here’s one week SHIBOR:

This is very impressive stuff from the PBOC. Other central banks have a habit of throwing up their hands when their tools are challenged by markets. The takeaway from this episode is this:

“Is there a problem or two with China? Yes, there are a series of complex problems,” says Mr Milligan at Standard Life. “Are they likely to erupt into a crisis in the near term? Probably No. Does this mean the Chinese economy is likely to slow because the authorities have less room for manoeuvre? Certainly.”

In other words, more pressure coming on the property and commodity complex. And that’s where we can turn to the AFR’s Lisa Murray, who produced a fine feature over the weekend:

This abandoned and eerie construction site, outside the coalmining town of Liulin in Shanxi province, is ground zero for China’s fast-growing “shadow banking” system. It is one of the biggest risks lurking in the global economy.

The brainchild of local coal tycoon Xing Libin, it was supposed to transform his humble birthplace into a hive of economic activity. The unfinished apartment blocks would have provided accommodation for the people working on Xing’s vast agricultural scheme involving hundreds of acres of nearby farms. In this idyllic new world, locals would tend to walnut trees, raise chickens, fatten cattle and farm fish.

Instead, Xing’s grand plans have left his coalmining company, Liansheng Energy Group, crippled under a pile of debts worth more than 30 billion yuan, almost a quarter of which was sourced from China’s poorly regulated trust sector.

Xing’s demise has sent ripples across global markets as his struggle to pay back investors lays bare what is arguably the most serious risk to the world’s second-biggest economy this year – a major trust default. Such an event has been likened to a wake-up call on the scale of the Lehman Brothers’ collapse in the United States.

…David Cui, who has published extensive research on the issue for Bank of America Merrill Lynch, says it will probably be more like the less dramatic failure of Bear Stearns.

…Cui’s view is that the first default will happen in the next few months and, once more defaults pile up, a tipping point will be reached in terms of public confidence. That’s when the credit crunch happens.

…“I think the government will react very fast, write off some debt, force some debt to convert into equity and hopefully we can recover quickly.”

I’ve noted many times that China has various mechanisms not available to Western regulators in managing financial crises. It can summon bad banks from thin air, has suasion in bank balance sheets and does not face the same legal constraints in forcing swift resolutions. More broadly, the economy has loads of productivity potential as its moves up the value chain. Cui’s optimism about swift action has some basis in fact and offers hope that China is a giant Korea in the making, not a giant Japan.

But let’s not kid ourselves. We are dealing with an outrageous bubble in fixed- asset investment and bringing it to heal comes with large risks. There is also what may prove to be China’s greatest challenge over the long term to consider: its fading demographic dividend.

On balance, I still think that China will be fine in the long run but I wouldn’t count on its over-sized support of Australian mining for very much longer.