Cross-posted from Tom Conley at the Big P Political Economy

Asia’s rise has been Australia’s economic gain. The rise of Japan, followed by South Korea and Taiwan, Singapore, Malaysia, Thailand and other non-communist countries of Southeast Asia had provided significant export markets for Australian commodities, though not a sustained structural increase in their value. Then along came China, changing everything. Not only did rapid Chinese demand increase the prices Australia received for its exports, but also Chinese manufacturing production helped to decrease the price of Australian imports. Manufactured goods made (or assembled) in China became significantly cheaper. Chinese competitive pressures also helped to keep in check the prices manufacturers throughout the world could charge for their goods.

Currently there are several narratives about Australia’s economic future. The first is an acceptance of Australia’s role as a resource exporter built on the back of long-term Asian demand and a high exchange rate. Alongside this story is one about a growing Asian middle class, which will be increasingly receptive to utilising Australian services. This view means that there will be an alternative market for Australian exports after the Asian giants become less resource intensive economies as they progress up the income ladder.

All of these positive narratives are based on a projection that Asia’s remarkable rise over the past half century will continue over the next half. The possibility that Asia may not continue its rapid economic rise is largely dismissed as a narrative, although the likelihood that Asia will become conflict-ridden is common in international relations, foreign policy and security studies.

To understand where Asia might be headed we need to fathom how far it has come since the end of World War II.

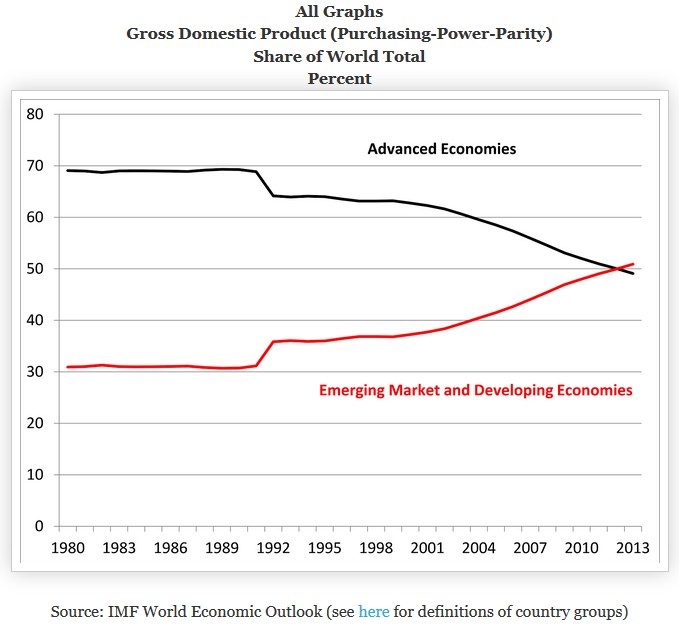

This post shows that if current GDP trends were to continue, even at a moderated pace, Asia will become the world’s most important economic region and China the world’s largest economy. Emerging market and developing economies have overtaken the advanced economies on a purchasing power parity basis. The major component of this GDP convergence has been the rise of developing Asia, particularly China. Asian GDP (both developed and developing) is now approaching the GDP of the European Union and the United States combined.

Economically, a continuation of present trends would provide amazing opportunities for Australia, although politically it might heighten concerns amongst Australians about the implications of Western and American relative decline.

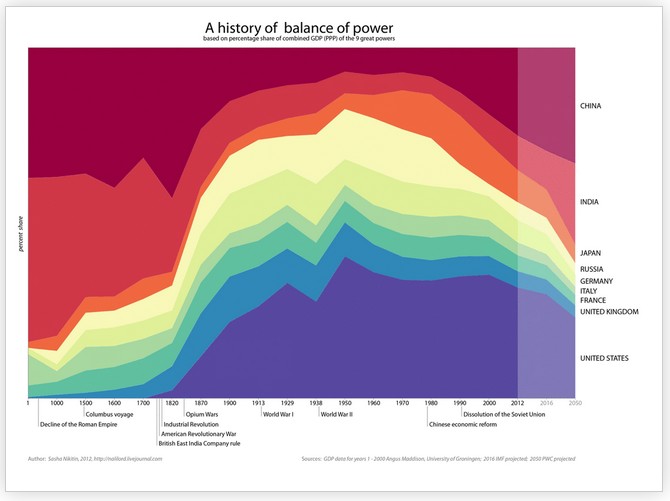

The Great (Re)convergence

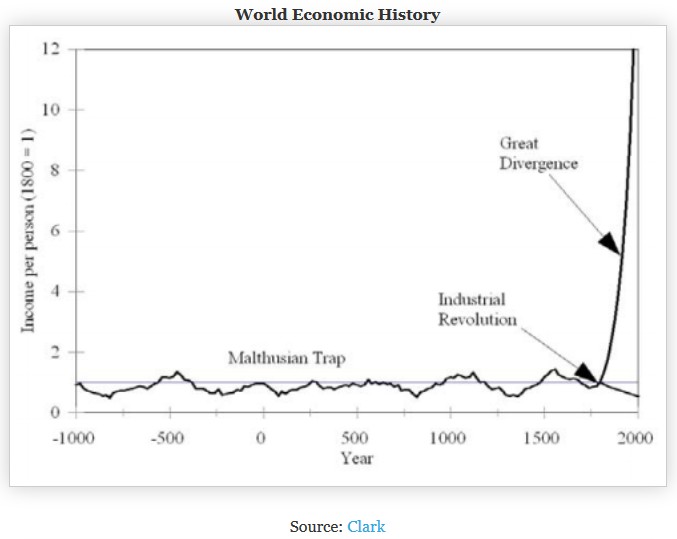

The rise of developing Asia has been a major component of the so-called rise of the rest, which has led to the reversal of the great divergence between the advanced and developing economies that began with the industrial revolution. The great convergence is profoundly reshaping the world economy. Given that the world economy on the eve of the industrial revolution was dominated by Asia – particularly China and India we should perhaps consider the current period as the great reconvergence.

Gregory Clark in A Farewell to Alms outlines the Malthusian world (from the Stone Age to 1800), which he argues exhibited “a counterintuitive logic” where:

anything that raised the death rate schedule –war, disorder, disease, poor sanitary practices, or abandoning breast feeding – increased material living standards. Anything that reduced the death rate schedule – advances in medical technology, better personal hygiene, improved public sanitation, public provision for harvest failures, peace and order – reduced material living standards.

In other words, vice equalled virtue and virtue equalled vice. Even gradual improvements in technology increased population and therefore did not lead to lasting increases in living standards. Hobbes, Clark contends, was wrong; man was better off in his natural state.

The Industrial Revolution, whose most remarkable feature is the “all-pervading rise in incomes per person”, changed all that and led to a remarkable divergence between rich and poor countries. The gap between the living standards of the rich and poor countries grew from 3-4:1 before 1800 to 40-50:1 in the late twentieth century.

The commercial revolution from the late fifteenth century shows that global economic weight is not necessarily an indication of global power. Asia’s dominance of the world economy until the early nineteenth century could not stop it from being overrun by European colonial powers from the sixteenth century. Economic dominance was overcome by military superiority.

Gross economic weight is clearly not everything, but there can be no doubt that economic relativities are changing, which provides the possibility that the West’s period of dominance is coming to an end.

Growth in Asia since the 1960s has been nothing short of remarkable. Economic success, however, was far from universal. Until the late 1980s, authoritarian capitalist states and authoritarian communist states divided Asia. Countries under US tutelage embraced an authoritarian form of capitalism with a strong developmental ethos. The success of capitalist economic development provided a stark contrast to the failures of the socialist centrally planned development model.

China attempted to collectivise and control economic development from the centre, Vietnam struggled with war and its aftermath, and India fostered autarkic import substitution policies that led to stunted growth. Even before the end of the Cold War, the Communist and insular states realised that shifts in economic direction were vital if they were going to replicate the high growth rates of capitalist Asia. China began its long march to capitalist dynamism in 1978 and Vietnam switched economic direction in the mid-1980s.

By the early 1990s, Japan appeared to be set to overtake the US economy, but unfortunately the 1990s were a decade of stagnation after the excessive property and stock market boom of the late 1980s. In the late 1990s, the region suffered a severe financial crisis which threatened to derail Asia’s rise, but by the early 2000s it was clear that the crisis was only a temporary set back on Asia’s phenomenal economic rise.

From the mid-1990s, China became the major economic story in the region because of its sustained high growth rates. China’s continuing growth during the economic crisis that began in 2007 cemented Asia’s place as the centre of world economic dynamism. Growing regional production networks initially developed by Japan in the 1980s, followed by South Korea, Taiwan, Singapore and Hong Kong and now centred on the Chinese economy have reinforced Asian dynamism. Despite assertions about decoupling, final goods demand from outside the region still matters for Asian growth.

In recent years, many analysts have argued that India will join China as a major Asian success story. Developing Asia has been joined by other emerging economies to transform the world economy since the 1980s. The countries of Eastern Europe, Brazil and South Africa have led to the great reconvergence.

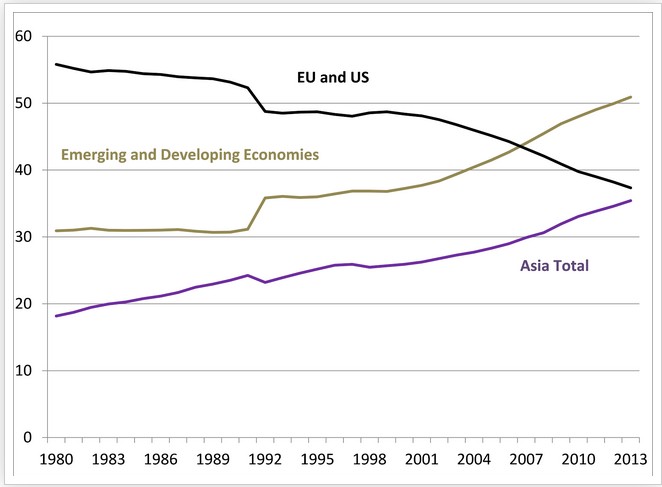

Emerging market and developing economies now account for over 50 per cent of the world economy on a PPP basis, surpassing the total weight of the developed economies. This is a remarkable change from 1990 when the emerging market and developing countries accounted for a little over 30 per cent. Since 1990 emerging and developing economies have been on an ever-upward trajectory, with the global crisis beginning in 2007 thus far affecting mainly the United States and Europe.

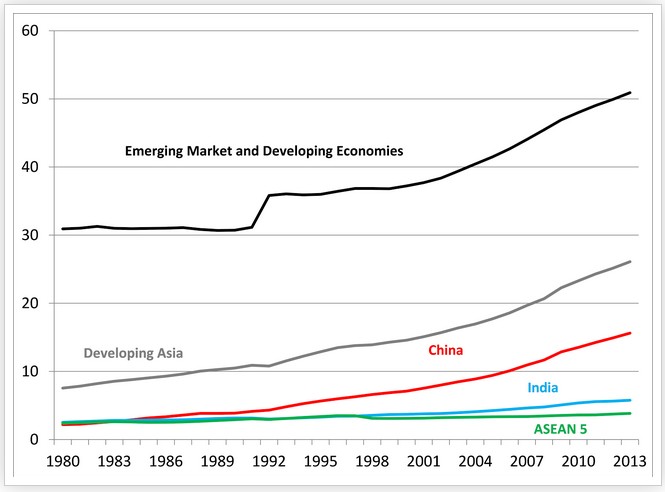

The bulk of the increase in the emerging and developing country share has been accounted for by developing Asian economies, particularly China.

The Asian economies combined – both developed and developing – are approaching the economic weight of the European Union and United States combined. Given projected relative growth rates Asia should overtake the EU and US in the near future. The EU and the US combined has declined from 55.8 per cent of the total in 1980 to 37.4 per cent in 2013.

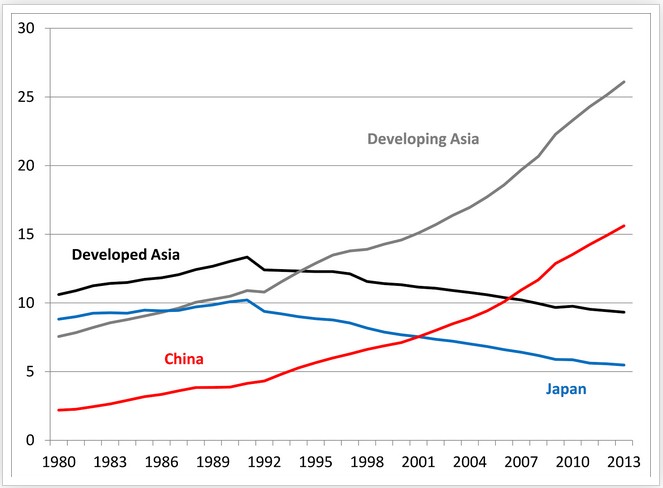

The rising economic weight of Asia has mainly been a result of rapid growth in China, although India and the ASEAN 5 have also contributed. China’s increased weight has been at the expense of Japan. (Developed Asia includes Japan, South Korea, Singapore, Taiwan and Hong Kong)

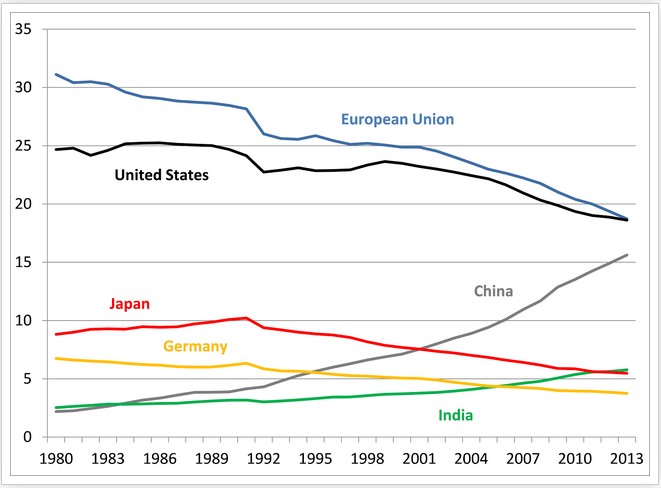

Comparing the top 5 plus the EU we can clearly see the significant changes to relative weights since the early 1990s. These trends have been strengthened since the global crisis. The advanced capitalist countries have lost ground to China and India.

The Future

Ideas about an Asian ascendancy are not new. US President, Theodore Roosevelt, writing in 1903 argued that: “The Atlantic era is now at the height of its development and must soon exhaust the resources at its command. The Pacific era, destined to be the greatest of all, is just at its dawn.” (Yahuda) War and the dilemmas of decolonisation made Roosevelt’s prediction premature, but the post-war world has seen Asia rise to the world’s most dynamic economic region. The general assumption today is that the Asian ascendancy will continue, even if the breakneck speed of growth moderates in coming years.

Japan, unlike the East Asian “tigers”, seems to have grown both through high rates of input growth and through high rates of efficiency growth. Today’s fast-growth economies are nowhere near converging on US efficiency levels, but Japan is staging an unmistakable technological catch-up.

Advanced economies

Composed of 35 countries: Australia, Austria, Belgium, Canada, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hong Kong SAR, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Malta, Netherlands, New Zealand, Norway, Portugal, San Marino, Singapore, Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Taiwan Province of China, United Kingdom, and United States.

Major advanced economies (G7)

Composed of 7 countries: Canada, France, Germany, Italy, Japan, United Kingdom, and United States.

Other advanced economies (Advanced economies excluding G7 and euro area)

Composed of 14 countries: Australia, Czech Republic, Denmark, Hong Kong SAR, Iceland, Israel, Korea, New Zealand, Norway, San Marino, Singapore, Sweden, Switzerland, and Taiwan Province of China.

European Union

Composed of 27 countries: Austria, Belgium, Bulgaria, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Slovak Republic, Slovenia, Spain, Sweden, Romania, and United Kingdom.

Emerging market and developing economies

Composed of 153 countries: Afghanistan, Albania, Algeria, Angola, Antigua and Barbuda, Argentina, Armenia, Azerbaijan, The Bahamas, Bahrain, Bangladesh, Barbados, Belarus, Belize, Benin, Bhutan, Bolivia, Bosnia and Herzegovina, Botswana, Brazil, Brunei Darussalam, Bulgaria, Burkina Faso, Burundi, Cambodia, Cameroon, Cape Verde, Central African Republic, Chad, Chile, China, Colombia, Comoros, Democratic Republic of the Congo, Republic of Congo, Costa Rica, Côte d’Ivoire, Croatia, Djibouti, Dominica, Dominican Republic, Ecuador, Egypt, El Salvador, Equatorial Guinea, Eritrea, Ethiopia, Fiji, Gabon, The Gambia, Georgia, Ghana, Grenada, Guatemala, Guinea, Guinea-Bissau, Guyana, Haiti, Honduras, Hungary, India, Indonesia, Iran, Iraq, Jamaica, Jordan, Kazakhstan, Kenya, Kiribati, Kosovo, Kuwait, Kyrgyz Republic, Lao P.D.R., Latvia, Lebanon, Lesotho, Liberia, Libya, Lithuania, FYR Macedonia, Madagascar, Malawi, Malaysia, Maldives, Mali, Marshall Islands, Mauritania, Mauritius, Mexico, Micronesia, Moldova, Mongolia, Montenegro, Morocco, Mozambique, Myanmar, Namibia, Nepal, Nicaragua, Niger, Nigeria, Oman, Pakistan, Panama, Papua New Guinea, Paraguay, Peru, Philippines, Poland, Qatar, Romania, Russia, Rwanda, Samoa, São Tomé and Príncipe, Saudi Arabia, Senegal, Serbia, Seychelles, Sierra Leone, Solomon Islands, South Africa, South Sudan, Sri Lanka, St. Kitts and Nevis, St. Lucia, St. Vincent and the Grenadines, Sudan, Suriname, Swaziland, Syria, Tajikistan, Tanzania, Thailand, Timor-Leste, Togo, Tonga, Trinidad and Tobago, Tunisia, Turkey, Turkmenistan, Tuvalu, Uganda, Ukraine, United Arab Emirates, Uruguay, Uzbekistan, Vanuatu, Venezuela, Vietnam, Yemen, Zambia, and Zimbabwe.

Developing Asia

Composed of 28 countries: Bangladesh, Bhutan, Brunei Darussalam, Cambodia, China, Fiji, India, Indonesia, Kiribati, Lao P.D.R., Malaysia, Maldives, Marshall Islands, Micronesia, Mongolia, Myanmar, Nepal, Papua New Guinea, Philippines, Samoa, Solomon Islands, Sri Lanka, Thailand, Timor-Leste, Tonga, Tuvalu, Vanuatu, and Vietnam.

ASEAN-5

Composed of 5 countries: Indonesia, Malaysia, Philippines, Thailand, and Vietnam.