The RBA appears to have rolled out board member John Edwards to counter yesterday’s government leak that it was annoyed that the bank had allowed the dollar to rise beyond forecasts. From the AFR:

Speaking after The Australian Financial Review revealed the government’s anger at the Reserve Bank’s decision to drop its easing bias, which has been blamed for boosting the dollar, Dr Edwards said Australia was in the grip of a “bountiful” mining and energy export-driven revenue surge.

…“It’s very difficult to expect rhetoric to have an impact on economic forces which are running in the opposite direction,” he said.“If you’ve got a mood going on in the currency, then rhetoric alone is not going change it.”

…“The currency argument is that a fall in the terms of trade should see lower exports and therefore less demand for the Australian dollar,” Dr Edwards said. “It’s not working out like that. In fact US dollar revenues have increased [for local mining companies].”

“And the balance of trade has for several months been positive, once again. And that means, in terms of what happens in foreign exchange markets, you wouldn’t necessarily expect to see a weaker dollar if it’s associated with, effectively, a boom in exports.”

…Opposition spokesman on finance Tony Burke said the government’s anger about the Reserve Bank was extraordinary. “After years of both sides of politics agreeing on the need to have an independent Reserve Bank, Joe Hockey has decided his political needs are more important than the independent status of the bank.”

The dollar has turned for a number of reasons, the volumes boom being just one and probably the smallest. The current trade surplus will disappear in the next few months as much lower bulk commodity prices filter through to quarterly contracts, despite volume growth. The trade deficit will grow further over the next twelve months as iron ore goes much lower. Equity markets, too, are underestimating the impact of falling iron ore prices on earnings with RIO and FMG both holding up better than they should given their prospects. In short, markets are not discounting the future that is coming. That could be seen as a “mood”.

That attitude comes from four combined shifts in Q1 in global circumstance which really amount to one thing. The US recovery has again disappointed, pushing back rate hike expectations. China has hit the stimulus accelerator again (albeit mildly), the EU is clearly in the process of entering the money printing race as deflation looms, and Japan’s Abenomics burst is slowing and requires more money printing to get going again.

In short, we’re traversing an echo period of competitive monetary devaluation in which the US dollar is held down, commodity-intensive emerging markets are seen as the growth driver and real assets are seen as value protection. This is putting upwards pressure on all of the commodity currencies, and gold, not just the Australian dollar. Here is the Aussie versus the Brazilian real:

Or the South African rand:

Or the Norwegian kroner:

I could have chosen just about any commodity currency and the charts look the same (with the exception of Chile, where copper is all that matters).

So, as we wring our hands, there are several points to make. The first is that we aren’t losing competitiveness against commodity competitors, for the most part. It’s against the manufacturing and service economies that we’re losing production.

There are two questions then. How long will it last and can anything be done about it?

These kinds of global flows will have their way. Money managers have, for the time being, decided that China is going to keep growing at breakneck speed and the US is going to under-perform (or they over-bet on the opposite late last year and are covering positions). But the macro truth is most probably the opposite – the US should accelerate out of its winter slump and China will keep slowing in the medium term – so these flows will likely reverse again in the next six months.

Second, can anything be done about it? Well, yes. Something should have been done about it three years ago. Macro themes are a part of the story but the underpinning investment calculus is the interest rate spread. The countries benefiting most from the renewed push into commodity currencies are those with higher interest rates, or the prospect of them, and it is here that the RBA has stuffed up.

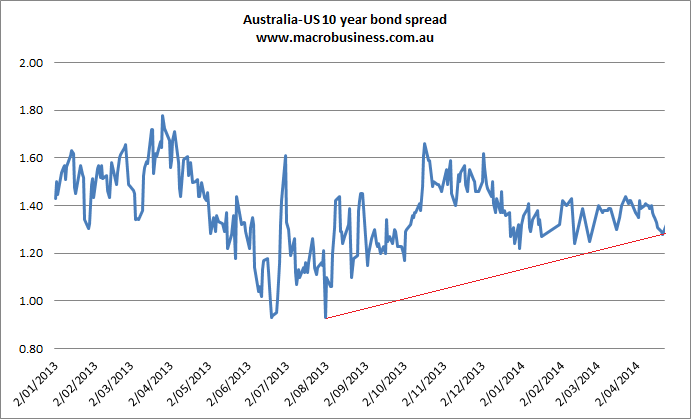

When it began slashing interest rates two and half years ago, the RBA explicitly targeted a housing boom. Now it has a growing bubble on its hands and hence interest rate markets are pricing interest rate rises in the next twelve months, long before the real economy is ready for them given the long unwind ahead in mining investment. That has global hot money flows pursuing the carry trade into the Australian dollar as the interest rate spread has climbed a long way off last year’s lows:

What the RBA should have done was introduce macroprudential tools, which would have insured that housing credit was controlled in this recovery cycle and interest rates could be another 50-100 bps lower. The recovery we should have had is in tradables with support from housing construction, not the other way around.

It could still be done and would have an effect. But the risk now is that it would work too well and cause a housing bust, just as we head of the mining capex cliff.

Likewise, Joe Hockey need not wait for the RBA. He too can have his lower dollar quite easily. He could shift negative gearing to new dwellings only. That would stall house prices and offer the opportunity for rate cuts to close the carry trade spread. He could install Tobin taxes on hot money inflows, which would help take the edge off and raise extra revenue. He could slash and burn in the Budget and force interest rates and the dollar lower.

However, Joe Hockey is mostly innocent (even if his Party’s previous policies are not). Competitive monetary devaluation has been a global reality for five years. The RBA and former Labor government ignored it, preferring to pat themselves on the back and see movements in the dollar as the result of Australian (and their own) exceptionalism. Now they’d rather play a blame game than address their own blunders. As such, we’re still swaggering unarmed through the global currency war.