From Bloomie:

China is succeeding in making its currency less predictable. Investors are paying the price.

Clients of U.S. commercial banks have lost about $2 billion this year on $332 billion of options betting the yuan would appreciate, while Chinese companies lost $3.5 billion on $150 billion wagered on a benchmark forwards contract, according to data compiled by Morgan Stanley and the Depository Trust & Clearing Corp. inWashington. These contracts, when including bearish bets, account for more than a third of global trading in the Chinese currency.

After almost a decade of gains, speculators had come to regard the yuan as a one-way trade, leading to a surge in capital inflowsthat stands to leave the country vulnerable to a sudden shift in investor sentiment. Policy makers responded by selling the yuan and widening its trading band, encouraging a record 2.4 percent quarterly decline that was the biggest among Asian currencies.

“The depreciation was engineered to burn the fingers of speculators,” said David Loevinger, a former senior coordinator for China affairs at the U.S. Treasury and now a Los Angeles-based analyst at TCW Group Inc., which oversees $132 billion. “The People’s Bank of China wants two-way volatility embedded in the market.”

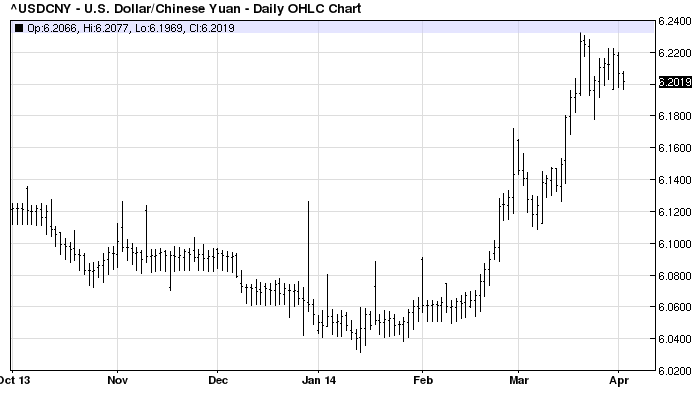

The PBOC has fixed its rate at marginally higher levels over the past few days, including today with a reference rate at 6.1493 (vs. prior set at 6.1503) but the currency continues to trade at the upper end of the band suggesting ongoing capital withdrawal:

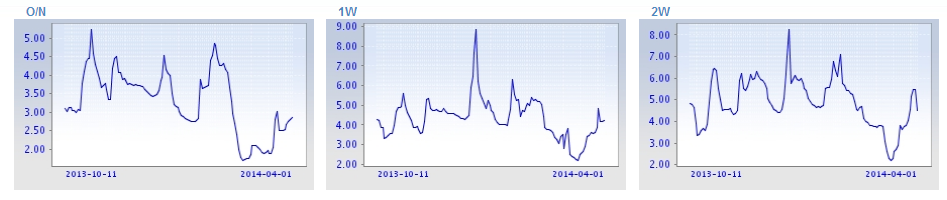

Looks like mission accomplished for now which, all things equal, should mean slower credit, which is in evidence in tightened interbank markets: