Find below the new Westpac-BREE China and resources mega-almanac the introduction to which is sounding very gloomy indeed:

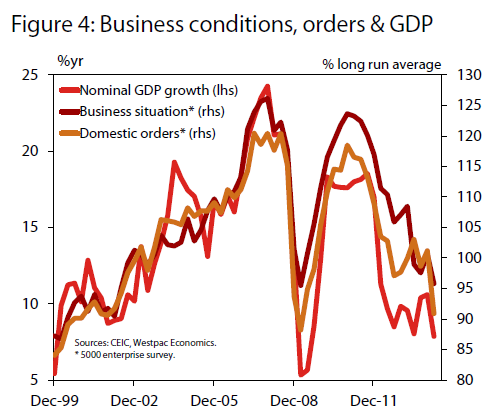

The Chinese economy grew at a rate somewhat below its potential early in 2014. The general impression left by the flow of data since the previous edition of CRQ has been one of outright deterioration. The respectable performance observed in the second half of last year, which at the time we suspected would be the peak for growth momentum in the current cycle phase, has been confirmed as such by the weak March quarter.

Growth in heavy industrial capacity slowed in early 2014, having managed to stabilise in the second half of 2013. Outlays on utilities projects have been disappointing in the year to date, given such spending looked somewhat underdone across the previous year. Countering that, investment in transport infrastructure was resilient in the March quarter, counter to expectations of a decline in growth.

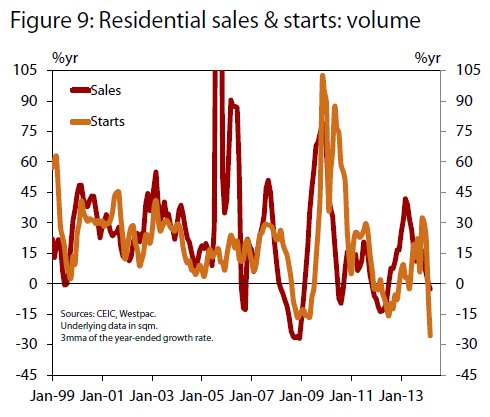

Real estate investment has been weaker than anticipated so far this year. Housing starts ended 2013 with some momentum, which promptly evaporated in early 2014. Developers have been hurt by weaker sales. This has hindered their ability to move stock and control their liquidity in the tighter monetary environment. Housing prices and sales turnover have both been under downward pressure. The secondary dwelling market has shown the most obvious strains, but the market for new dwellings has not been able to stand completely aloof.

The heavy industrial sector has just completed a poor first quarter. Inventories rose sharply from December through February, with production plans slow to adapt to a slowdown in sales. As of March, output and sales have moved closer into line, implying that the worst is now past from a sequential growth perspective.

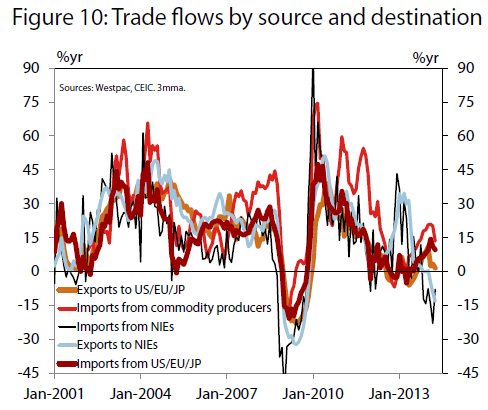

China’s exports to advanced markets are still growing faster than its total shipments, with Europe’s contractionary influence lessening and the US and Japan both now growing at reasonable rates. China’s imports from commodity producing countries are rising faster than its overall import bill, while imports of machinery and components for assembly are both looking sluggish.

In terms of external finance, the exchange rate depreciated in the March quarter as the People’s Bank prepared the ground for a doubling of the USD/CNY trading band. The year to date weakness in the CNY follows a 7.8% real trade weighted appreciation over 2013.

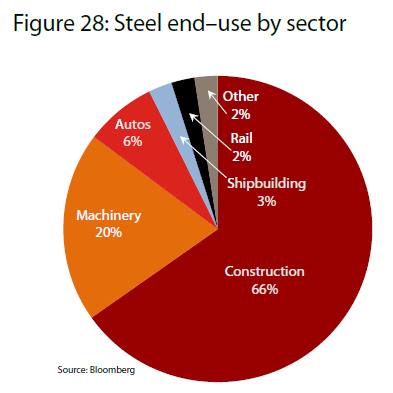

Despite the moderation in economic growth rates, China’s resources and energy use maintained an upward trajectory in 2013. Steel production increased by 9% to a record 775 Mt, contributing to iron ore imports reaching a record 820 Mt. Notwithstanding the implementation of policies to curb coal use, coal consumption also increased 2.6% to 3.61 billion tonnes in 2013.

Australia continued to play an important role in meeting the growth in China’s consumption, with increased export volumes registered across most commodities. Australia exported a record 442 Mt of iron ore and 42 Mt of thermal coal to China in 2013. Imports are playing an even more important role in meeting China’s overall mineral and energy demands, and in many commodity markets Australian producers have increased their market share in volume terms. This factor has mitigated the impact of lower prices on overall export earnings.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.