A property market slump remains a tail risk, but the tail is getting fatter – From a medium-term perspective, the current inventory and incoming supply can be mostly digested by rising demand amid ongoing urbanization and upgrading of living conditions. But in the near term, China’s housing market suffers from demand over- drafting and supply mislocation, and there are signs that a correction is around the corner. We expect government policies to be geared toward supporting demand while avoiding another construction boom that could disrupt the medium-term supply/demand balance. In the absence of supportive policies, property investment growth may fall to single-digit this year, dragging GDP growth to below 7%.

Houses are not tremendously oversupplied from a medium-term perspective – We estimate total house supply at 8.8bn sqm during 2014-20, taking into account GFA to be completed and existing house inventory. During the same period, demand from new and existing migrant workers and upgrading of dilapidated houses may reach 7.7bn sqm. With supply/demand ratio at 1.15 and investment demand not considered in the analysis, the prospective supply can mostly be digested. Japan’s experience indicates China may not enter a prolonged bear market in 10 years.

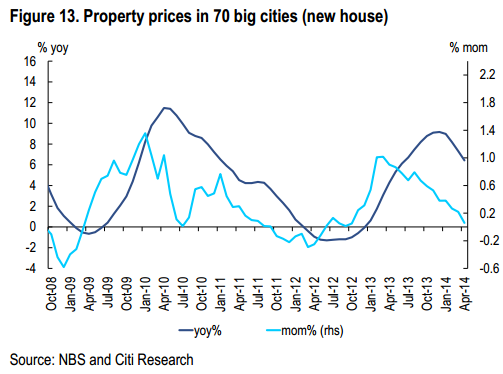

But in the short term the risk of a market correction is rising – House demand appears to have been over-drafted, as price increases fueled expectation of further appreciation, leading to GFA sold consistently higher than GFA completed in recent years due to pre-sales. Meanwhile, supply increased faster in smaller cities while the population tends to move to large cities. Entering 2014, there are increasing signs of an impending market correction, reflected in sluggish numbers on house inventory, sales and prices, new starts, land acquisition and investment.

Property investment slowdown would put downward pressure on growth – Since property investment accounted for roughly one-fourth of total FAI and FAI made up nearly half of China’s GDP, property investment directly contributes about 12% to GDP. We now estimate that total property investment may decelerate to about 14% this year, a main factor that would slow GDP growth to an estimated 7.3% in 2014. If residential new starts drop by 25% this year in the absence of policy support, GDP growth may fall below 7%.

We expect government to take targeted policies to support house demand – Policies could include: (i) increasing land supply in 1st tier cities; (ii) relaxing home purchase restrictions; (iii) linking hukou with house purchase; (iv) making mortgages more available and less costly; (v) government purchase of commodity houses to meet social housing targets. We expect 70-city average house prices to decline MoM as early as in May, and see prices cuts necessary to improve affordability and unleash potential demand.

A reasonable assessment with the exception that this is not a tail risk. It’s a reality.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.