The Commission of Audit’s (COA) report, released yesterday, notes that without reform to Australia’s tax and expenditure system, Australia “faces 16 consecutive years of budget deficits with net debt rising from $190 billion today to $440 billion by 2023-24″.

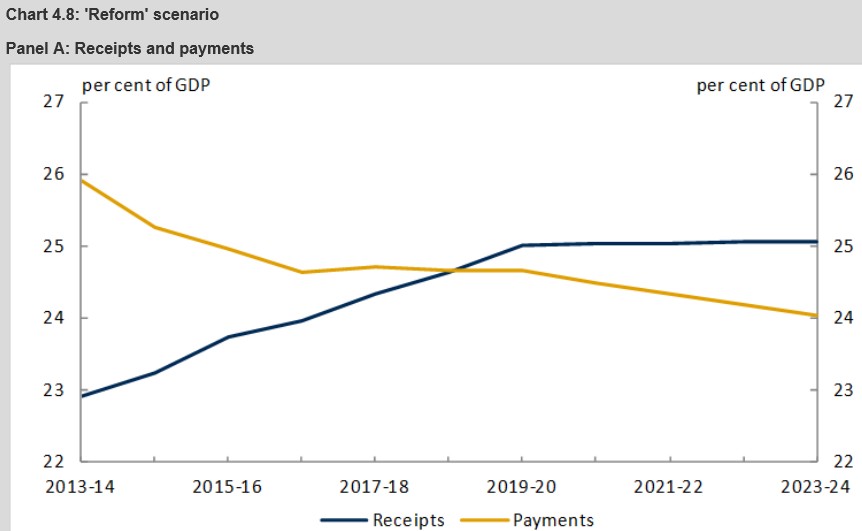

Accordingly, its 86 recommendations are designed to save the Budget between $60 to $70 billion per year within ten years, with additional savings from the reduction of debt, in the process bringing the Budget back to surplus by 2018-19 (see next chart).

.

. However, there are strong reasons to believe that the Budget would not return to surplus, even in the event that the COA’s recommendations were adopted in full.

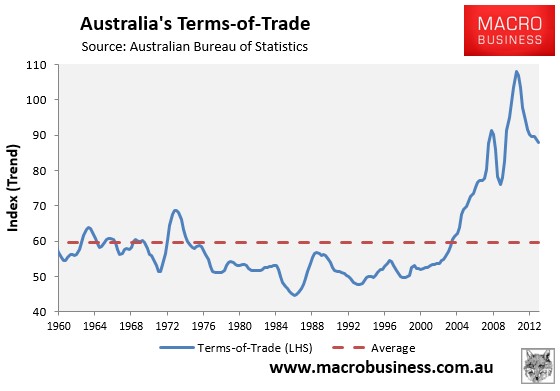

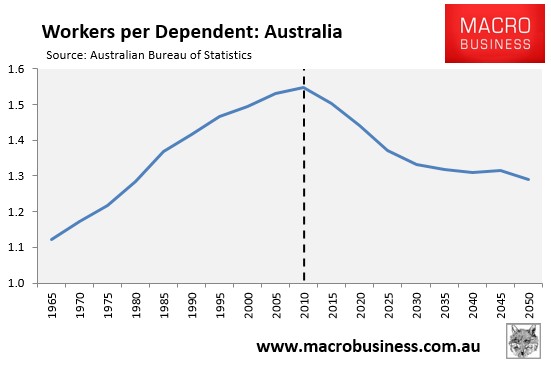

As argued by Business Spectator’s Callam Pickering, “tax receipts [are] assumed to return to 24 per cent of GDP (its average between 2000 and 2007) and total receipts (including dividends and other income) returning to 25 per cent of GDP”. However, “there are very real reasons why our tax base narrowed since the global financial crisis began and without tax reform it is not clear why revenue will head back towards its long-run average”. In particular, “the aging population will continue to hollow out the tax base”. In addition, “the terms-of-trade will fall over the forecast horizon”, which combined means that “without significant tax reform, receipts are unlikely to meet the commission’s assumption”.

Pickering is spot on. Tax receipts during the 2000 and 2007 were unusually high, juiced by the once-in-a-century commodity price (terms-of-trade) boom and favourable demographics, both of which are now reversing (see below charts).

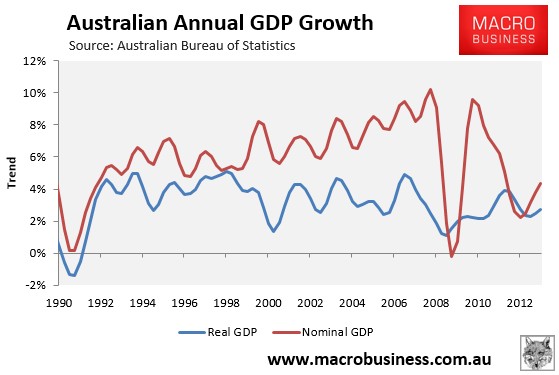

Nominal GDP is the dollar value of what’s produced and earned across the economy. It’s also the measure that drives taxation revenue. Due primarily to the inexorable rise in commodity prices and the terms-of-trade between 2003 and 2011 (with the exception of a brief collapse during the GFC), along with rising workforce participation, the Government enjoyed strong nominal GDP growth and booming tax receipts from rising personal and company taxes, not to mention increased capital gains taxes as asset markets boomed. However, since then, the terms-of-trade has begun to trend down, meaning that nominal GDP growth has been weak, as have tax receipts (see next chart).

The problem for the Federal Budget going forward is that the terms-of-trade is likely to continue to trend down towards its longer-term average, which will drag heavily on income growth and nominal GDP. As a result, personal and company tax collections will be soft relative to past experience, whereas Budget outlays could increase to the extent that weaker employment leads to higher welfare payments. These headwinds will of course be exacerbated by falling labour force participation brought about by population ageing.

The COA’s assumption that Budget taxation revenue will return to 24%, therefore, appears to be little more than a pipe dream unless fundamental reform is made to Australia’s taxation system. In turn, the Federal Budget is highly unlikely to return to surplus, heightening the prospect that the Government’s “temporary Budget debt levy” becomes permanent.