When I wrote the post Five Reasons to Fear an Australian Recession I discussed a possible convergence of five moderate shocks that could combine into one major blow. I’ve updated that post below in light of the iron ore crash.

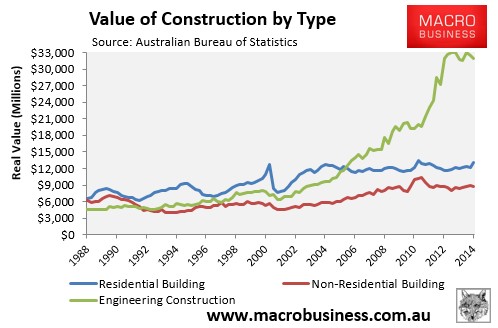

Consider. The structural backdrop for the economy is the mining investment cliff. Although it began two quarters ago, it is not until the second half of this year, probably Q4, that it begins to hit the employment market proper through the wind down of building and structures investment. It has a long way to fall after that (note the green line):

We’ve all known this for some time and interest rates have been cut to record lows to stimulate consumption to offset it. Last week that project received a boost in ABS capex intentions for the next year, which showed a little easing in the mining capex cliff and solid rebound in services investment. If it proves accurate then business investment would fall around 1% of GDP.

However, there are firm reasons to conclude that from here the intentions will erode. Mining expectations will come under intensifying pressure next quarter owing to the iron ore and coal crashes and sticky dollar. As well, the survey did not capture much of the Budget shock and early readings on retail suggest a material impact. The better services reading will also may pull back.

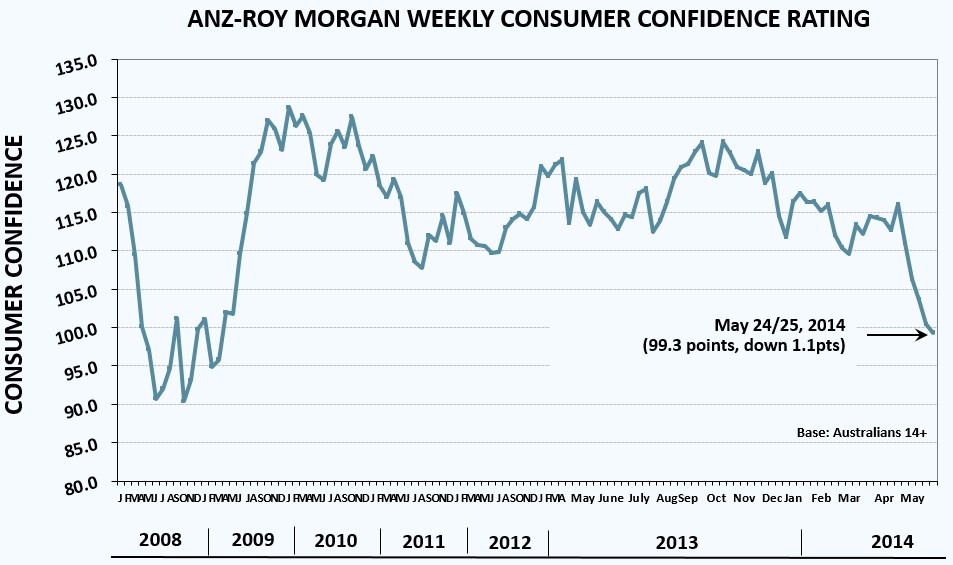

The second wave is the Budget, which has rocked consumer confidence to its lowest point since the GFC, and several weeks on shows no rebound:

Some component of the the big falls are “sticker shock” that will pass. But the structure of Budget cuts and the growing social conflict around it means that the political wrangling is likely to run right through to Q3 and the weight on confidence will be more enduring. There is also the unquantifiable impact of the loss of faith in the Government (which was economically material last year) and the possibility that consumers accept that there has been an epochal shift for the worse in Australia’s fortunes.

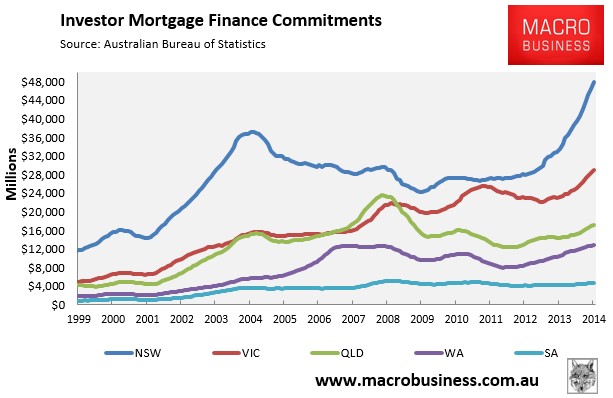

The other effect of low interest rates has been to fire up east coast property and the Sydney market has, frankly, entered a parabolic blowoff thanks to an investor mania (check out the blue line moon shot):

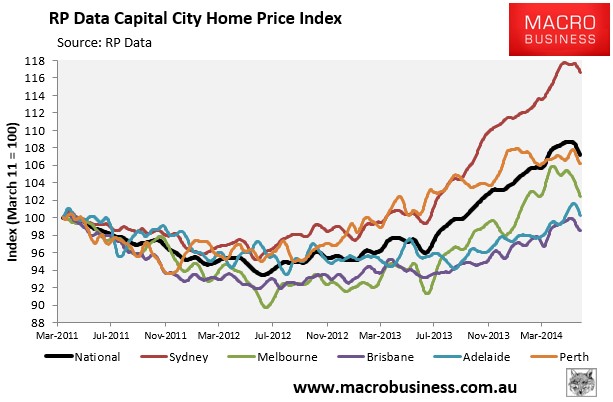

That is not the kind of pattern that deflates slowly. This is why the RBA is cautioning first home buyers to keep out of the market and warning that the bounce is “cyclical”. House prices growth usually weakens through winter and that has arrived right on cue:

The question is: will prices strengthen again in Q3 if consumer confidence remains suppressed? That’s my third wave. Sydney property is overheated and only needs a shock to send it into sharp reverse.

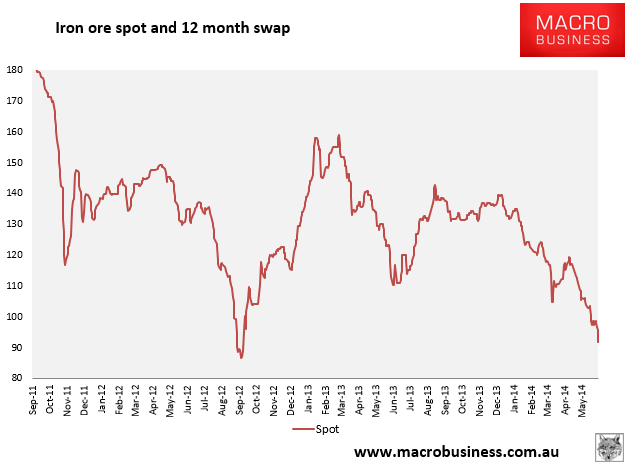

Such a shock is underway. Wave four is the iron ore price and mining equities, which are under intensifying pressure:

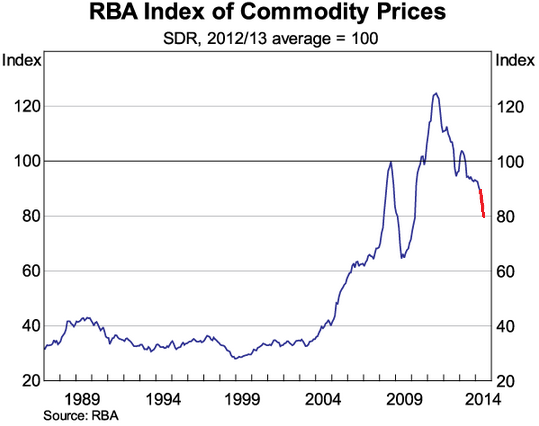

The iron ore market is very weak. You can read about that here. There’s a high risk of falls below $80 in the next month (before rebounding somewhat later in the year). That will mean all of the Budget’s estimated terms of trade (ToT) falls for next year are arriving instead before we even reach 2014/15. The RBA’s index of commodity prices is a good proxy for the ToT and will look roughly like this by year end:

This is going to make a mess of Budget revenues as corporate profits sink. By the time of the 2014/15 MYEFO in December the Budget will be sinking quickly into deeper than forecast deficit. The Abbott Government is already preparing further welfare reform and if its Budget has deteriorated in only its first six months of management – undermining it’s primary claim to govern – it will be very tempted to cut deeper into spending to reach the lower annual deficit target, weighing more upon growth.

An increasingly intense shakeout in the iron ore sector is also likely, which will involve restructurings and rationalisation. Predicting the timing of such is difficult for individual firms but it will begin in the second half of this year as the price falls below the costs of production for junior miners. The crisis will shift steadily down the cost curve as far as Fortescue Metals Group.

In sum, the iron ore price crash will hit household income via a number of channels.

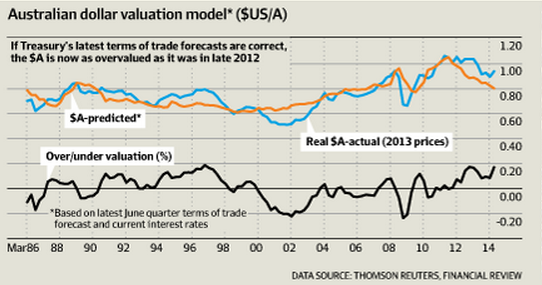

All of this is transpiring as the fifth wave is washing over everything already. It is the Australian dollar which is happily levitating far above fair value on the global chase for yield and preventing tradeable sectors from rebounding. Here is the AFR’s David Bassanese’s chart (which is similar to that used by Treasury and Goldman Sachs):

Remember, that’s fair value based upon commodity prices and interest rates overseas. It is still too high for the economy as it goes over a once per century mining investment cliff. In truth we need a much lower than fair value dollar for recovery. The high dollar is exacerbating mining and manufacturing woes, as well as rotting on the vine the low hanging fruits of recovery like tourism and education.

The possible convergence of these five negative waves in the second half would swamp the economy going into 2015. Consumer confidence leads house prices and if it remains weak as the external shock arrives, then Sydney and Melbourne housing could roll over just as mining-related job losses rise in WA and QLD as the Gorgon and QCLNG projects begin the construction wind down.

That’s an income shock, labour market stall and negative wealth effect plus public austerity. Headline growth will be supported by net exports but real activity in the national economy will resemble last year’s second half domestic demand recession only this time house prices will be stalling not taking off.

If the iron ore price crash does continue towards 80 cents then my October rate cut call will shift forward to August, with a possible follow up soon afterwards. I still expect the dollar to break into the low 80 cents range by year end.