The more I dig into yesterday’s superficially strong GDP result, the worse the underlying fundamentals appear.

While headline “real” GDP recorded quarterly seasonally-adjusted growth of 1.1% and annual growth of 3.5% – the best outcome since March 2012 – actual spending in the economy fell.

That’s right, real gross national expenditure (GNE), defined as the sum of all expenditure within the economy, both public and private (including on imports), fell by 0.3% in seasonally-adjusted terms in March and was up by only 0.9% over the year – the fifth consecutive quarter where annual growth in GNE was below 1%.

In trend terms, GNE was flat over the March quarter, and up by only 0.7% over the year – also the fifth consecutive quarter where annual growth in GNE was below 1%.

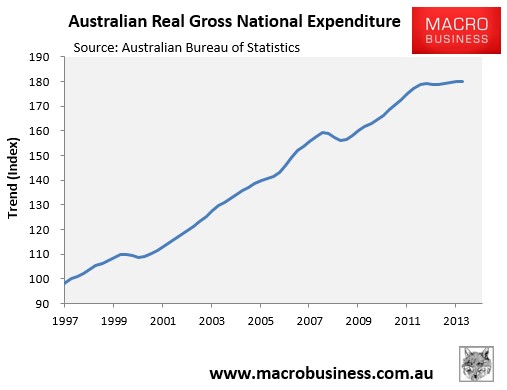

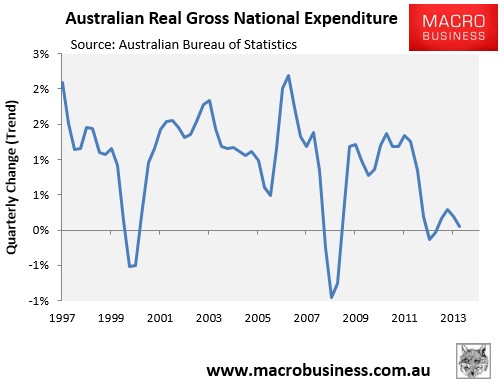

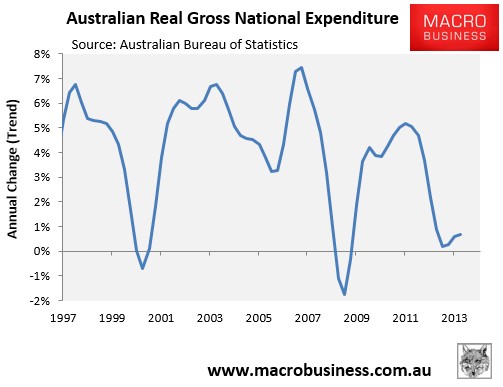

The below charts, showing the trend growth in GNE, highlights the current situation more clearly.

First, after rising strongly in the three years to September 2012, GNE has essentially flatlined:

Moreover, GNE growth has fallen over the past two quarters:

And remains in the gutter in annual terms – certainly well below the 3.7% average growth recorded in the decade to March 2014:

While the big expansion in export volumes is welcome, it does hide the fact that the domestic economy remains weak. Moreover, given the big post-Budget fall in consumer sentiment, the potential slowing of the housing market (i.e. slowing price growth, approvals, and lower auction clearances), and the expected accelerated falls in mining investment, stiff headwinds are likely to continue, weighing on both incomes and jobs.