In an interesting contrast to the Abbott Government’s do-nothing approach, the Conservative Government in the United Kingdom (UK) has announced that it will wind-back its own form of ‘negative gearing’ in a bid to give first home buyers greater access to housing. From The AFR:

David Cameron’s Conservative Party has handed down a budget littered with tax changes…

Galloping property prices, particularly in London, will be tackled by a restriction on tax relief for landlords who buy properties to rent them out. Landlords can now deduct their costs – including mortgage interest – from their earnings before they pay tax.

As in Australia, wealthier landlords receive tax relief at as much as 45 per cent, which is the top marginal tax rate. But from 2017 this tax relief will be reduced slowly to 20 per cent.

Chancellor George Osborne said the present system gave buy-to-let landlords a “huge advantage in the market” over people buying homes to occupy themselves.

It’s important to note that the UK is already far more restrictive than Australia in how it treats tax concessions for landlords.

In Australia, taxpayers can deduct their net loss on negatively geared assets (e.g. residential property and shares) against other types of income, including salaries or wages and business income. There are no restrictions on the number or types of assets held, and there are no caps to the amount of deductions (losses) that can be recognised in any one income year.

In the UK, by contrast, if a taxpayer makes a loss on an asset, that loss is quarantined to that asset class. If after applying the income losses in that asset class against the gains in that same asset class the taxpayer is still in an overall net loss position for the income year, then that loss can only be carried forward and utilised in future income years. Any unapplied losses can then be offset against the capital gain of the eventual disposal of the asset.

It follows, then, that Australia’s negative gearing system is already far more generous than the UK’s, since:

- There are no limits on losses recognised;

- The investor can apply losses against unrelated income (e.g. wages and salary);

- Losses are subsidised by tax refunds; and

- Losses are recognised at the individual’s marginal tax rate.

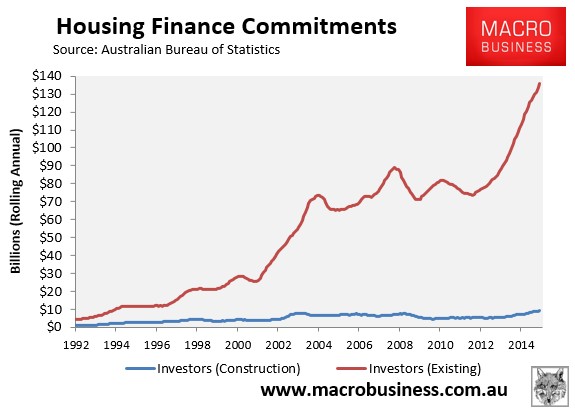

In turn, the loss of revenue to the Australian Government is greater than would occur under a ‘quarantined’ approach, like in the UK, and the amount of investment that takes place – primarily into existing housing (see next chart) – is higher than would otherwise occur.

There are obviously other major problems afflicting England’s housing market that prevent first home buyers from accessing affordable housing (most notably on the supply-side). Nevertheless, it is good to see a Conservative government take some action to reduce tax concessions for investor housing.

Tony Abbott should take a leaf out of David Cameron’s book.