Meet the new face of Australian rent seeking, from The Australian:

David Mackay, the former chief executive of global breakfast cereal giant Kellogg Co, says Australia risks missing an opportunity to revive its manufacturing base unless it starts making long-term investments in the consumer goods industry.

Mr Mackay, an Australian who ran Kellogg for four years, said Australia needed to lower its cost base and attract the right kind of foreign investment to help the nation’s food businesses grow.

“We are so well positioned if you think about the population in Asia, and yet we may not be galvanising the true ability we have,” Mr Mackay told The Australian Financial Review.

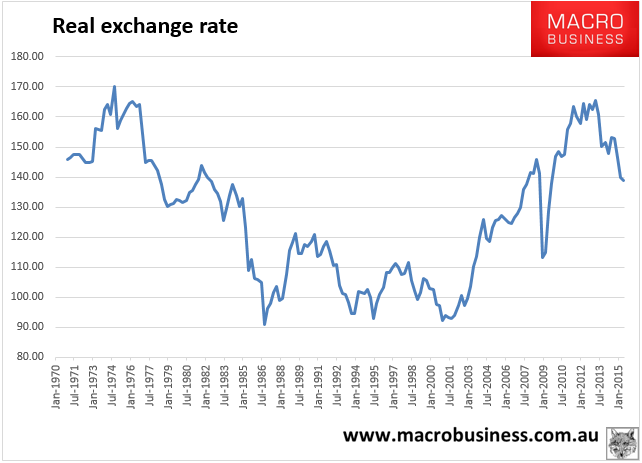

Good to see. Though I see no need to pick a winner in food. Let’s just improve competitiveness for the economy and all sorts of new miracles will transpire in the tradables sector. The real exchange rate remains at nose bleed levels:

I will admit, though, that it’s almost reached that point in the cycle when my arguments for real exchange rate repair have become moot. The Aussie dollar is going to fall so much further (well under 50 cents) as the commodity shakeout enters its denouement so competitiveness id going to rebound whatever we do at this point.

Still, it is worth noting that despite the sense of Mr Mackay’s words, his actions are another thing altogether, from The Australian:

As a real estate tragic, Mackay was drawn to the chairmanship of the Sydney-based agency after being introduced by recruitment industry veteran Geoff Morgan as founder John McGrath moved into a new phase of expansion, and assesses an initial public offering for the 69-office agency.

Mackay is wary of talk of a Sydney housing bubble, noting researcher Core Logic RP Data expects price growth in the city to ease to single-digits after surging growth during which prices rose 17.6 per cent in the year to August and 76 per cent since 2009.

“Clearly, it can’t be sustained or you end up with a bubble,” he says.

Mackay owns 10 investment properties apparently, some in the US, and is the new chairman of the soon to list McGrath Real Estate. This is ironic because it is Australia’s housing inflation model that is one half of why its real exchange rate is so high, hollowing out manufacturing.

So, as the great commodities reckoning rolls forward and the currency as well as real estate deflate for a time, Mr Mackay and Australia will need to ask themselves what they really stand for.

Will the chance to rebuild manufacturing capacity be seized or will it be squandered in a new real estate bailout that will, in all likelihood, be pushed vigorously by McGrath Real Estate?