Westpac has released its superb Red Book for October:

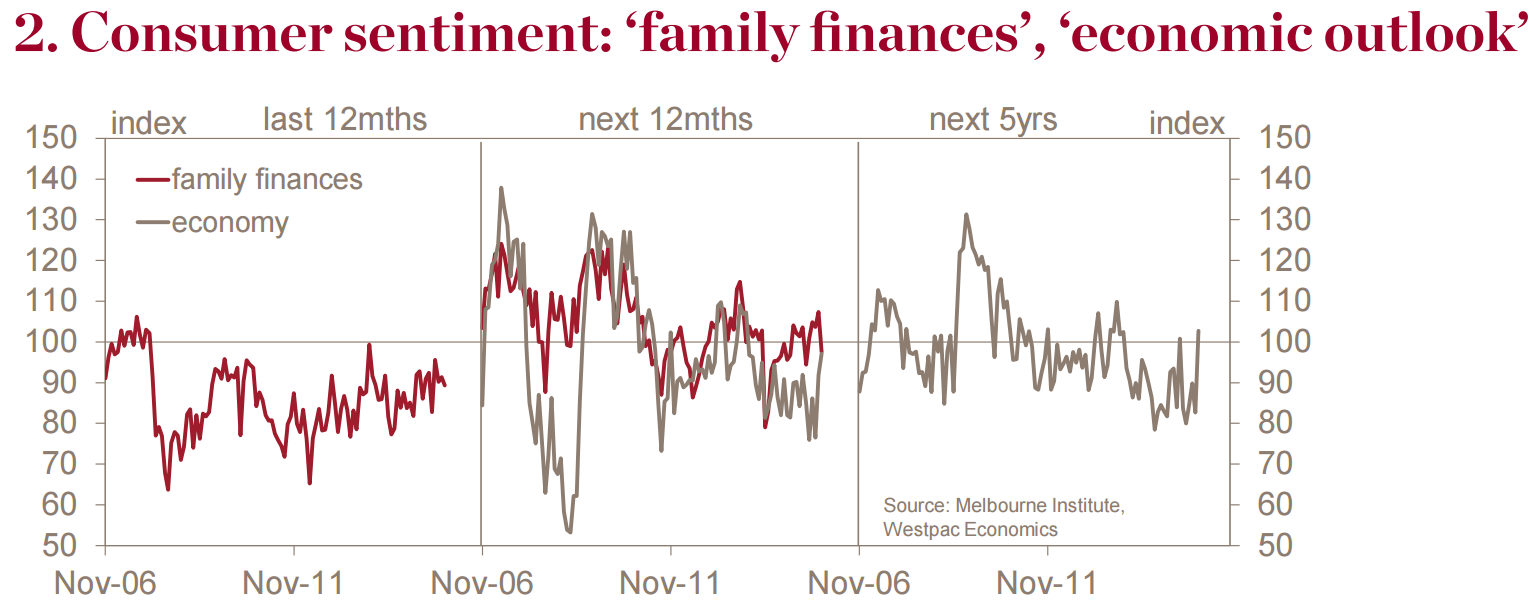

― The Westpac–Melbourne Institute Consumer Sentiment Index rose 3.9% in Nov from 97.8 in Oct to 101.7 in Nov. The gain was a surprisingly positive result, particularly given the major banks announced mortgage rate increases in the month.

― The component detail suggests the news on interest rates impacted negatively on assessments of family finances but was more than off set by a strong lift in confidence around the economic outlook.

― The improvement in economic confidence likely partly reflects the recent leadership change. In particular, our analysis indicates that the strong lift in the ‘economic outlook, next 5yrs’ sub-index is due to a mix of: improved assessments of ‘PM net satisfaction’ in opinion polls; an apparent ‘honeymoon’ effect following leadership transitions; and a more generalised lift in sentiment.

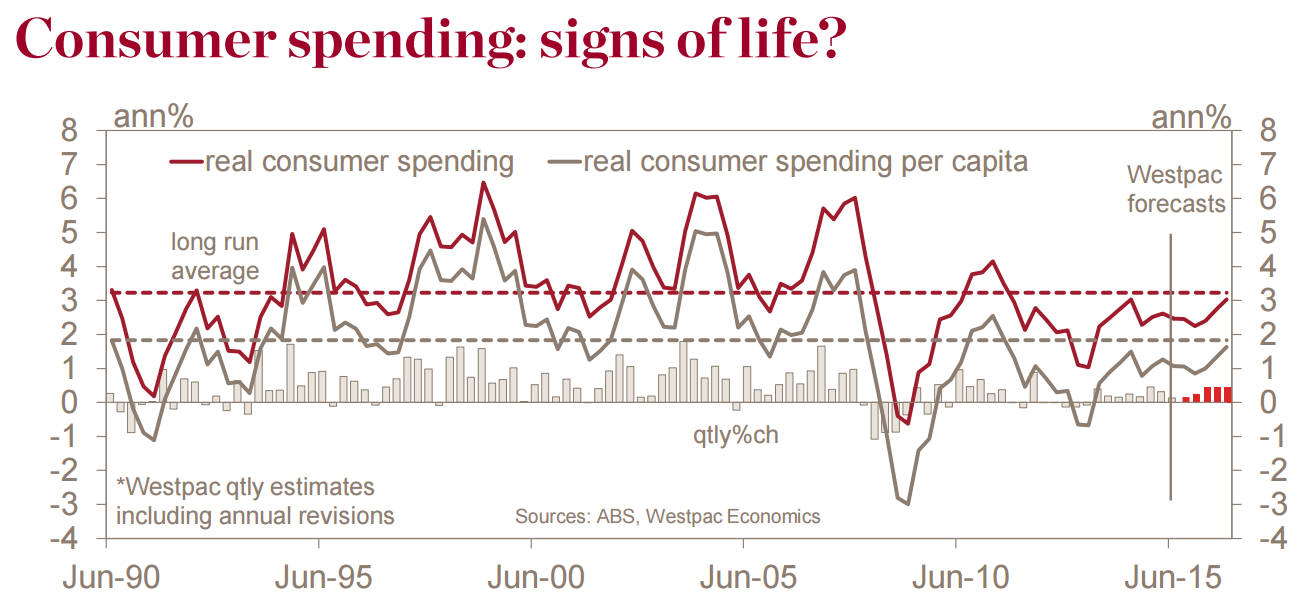

― Despite the positive headline, our CSI± measure – a modified sentiment indicator that we favour as a guide to actual spending – dipped 1.6% in Nov, reflecting the weaker view around family finances. The index suggests current subdued spending momentum will continue through the remainder of 2015 and into early 2016.

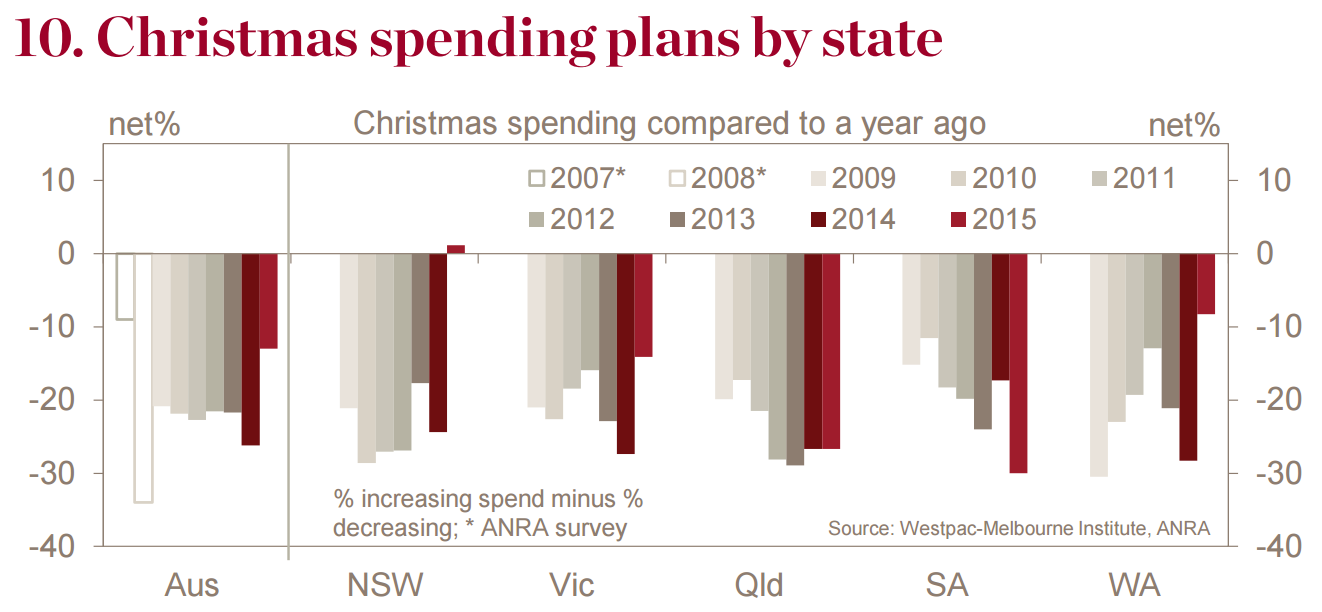

― Responses to our annual question on Christmas spending plans were much more upbeat. When asked directly about planned spending, 70% of consumers indicated they would be spending the same or more than last year. This compares to 62% this time last year and is the most upbeat response since 2007. Consumers in NSW reported particularly positive plans.

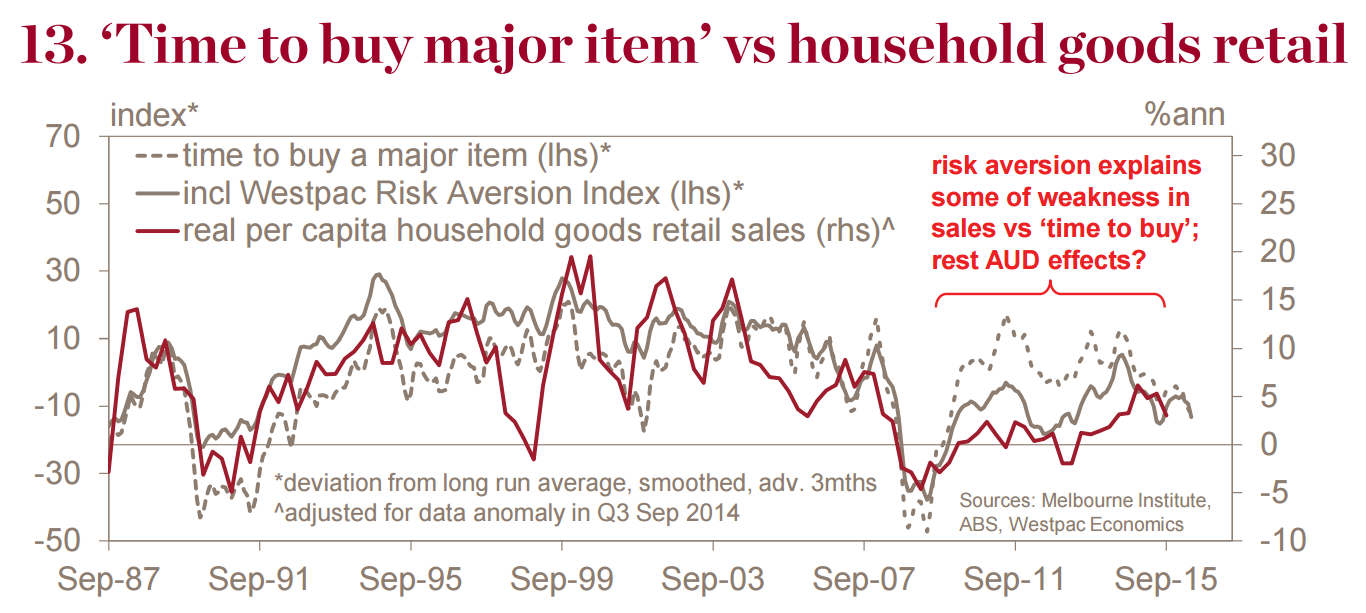

― Sentiment towards ‘big-ticket’ purchases also improved. The sub-index on ‘time to buy a major item’ rose 4.8% and has now recovered most of Sep’s sharp 13.5% drop.

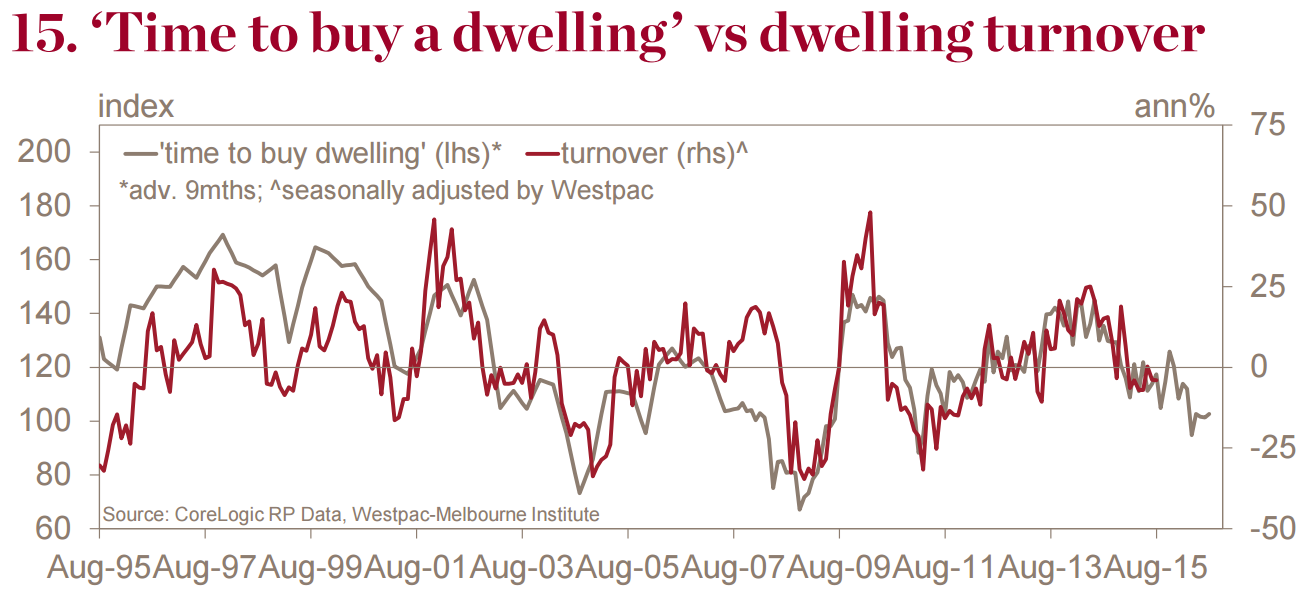

― Confidence around housing remains weak. The ‘time to buy a dwelling’ index lifted slightly by 1.4% but is still down sharply on a year ago and 29% below its 2013 peak. Current reads point to a significant decline in turnover nationally over the next year, but a mild downturn compared to previous corrections and likely to be mitigated somewhat by recent improvements in job security.

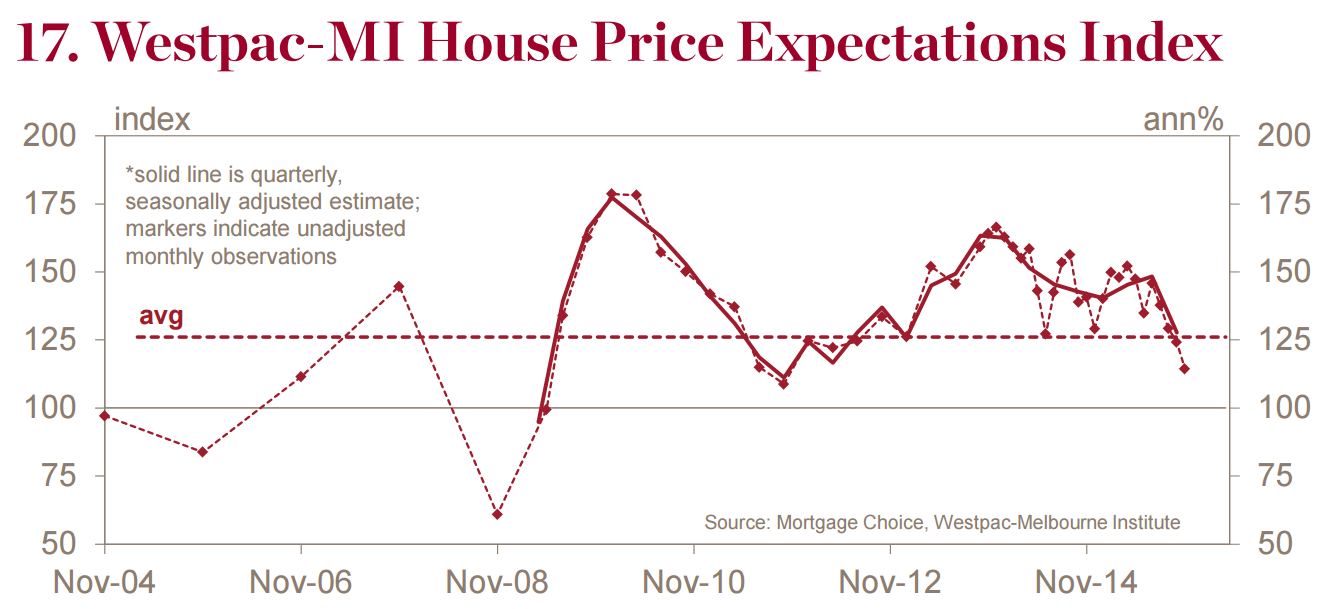

― The Westpac Melbourne Institute House Price Expectations Index also fell further, down 7.9% in Nov to be materially below its long run average. While the level is weak and momentum is negative, the index is still well above previous lows in 2008 and 2006.

― The Westpac-Melbourne Institute Unemployment Expectations Index rose 3.3% in Nov (recall that higher reads indicate a poorer outlook for unemployment). The increase should be viewed mainly as a consolidation of Oct’s sharp 13.7% fall with the net improvement in expectations over the last 2mths still leaving the index well below the pessimistic range that has prevailed over the last 2yrs.

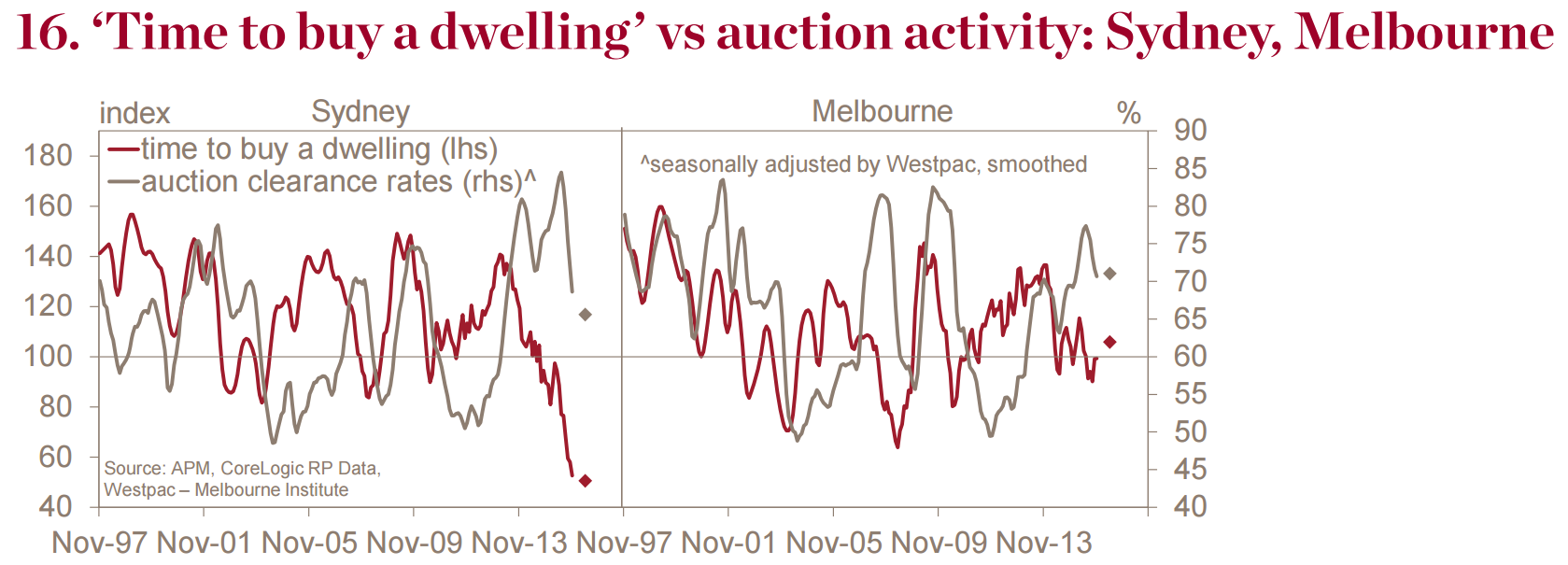

Westpac is reading this as a positive survey hinting at a turn in sentiment and spending. One look at those housing statistics is enough to weigh heavily against any such outcome. The approaching level of auction clearance rates suggested by the Sydney data is enough to worry about a looming moderate bust in prices. It’s even worse in Perth. No other city will stand up if that proves to be the case and spending will follow suit. Sure, unemployment expectations are off their peaks and there is some encouragement in the greater security being registered about the economy but if house prices roll, especially in Sydney, then all of those nice little hockey stick recoveries that Westpac is forecasting will invert.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.