Global equity markets did not react well to ECB President Mario Draghi’s intimation that last night’s easing measures may have been it for further cuts to the deposit rate. Despite the announcement of a larger than expected extension to the asset purchasing program and the inclusion of investment grade non-bank corporate bonds, equity markets were unimpressed. Nonetheless, the bruised European banking sector welcomed an end to further rate cuts into negative territory, credit default swaps pulling back significantly and a number of banking stocks closing the European session in positive territory.

Despite a negative open to the Asian session, cash markets and US and European futures markets have bounced into positive territory in the latter half of the session. Debt markets were far more upbeat on the ECB announcement and it appears that the more erratic equities market is now following the calmer lead of the bond market and moving higher. Indeed, the ECB announcement of expanding asset purchases into corporate debt opens up real opportunities for investment in European corporate debt, such as buying the IBCX (iShares Euro Corporate Bond Large Cap UCITS ETF) on the FTSE.

Gold is likely to come into some strong resistance as it approaches 2015’s highs around the US$1300 level

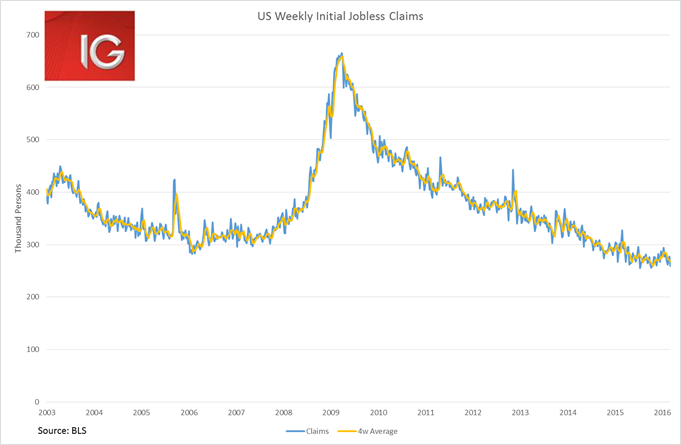

Gold rallied strongly overnight, benefitting from the volatility around the ECB decision. While the metal has had an incredible rally so far in 2016, a number of factors may begin to weigh on it. Continued outperformance from gold requires either an explosion of inflation or a reversal of the Fed’s December rate hike. US data has continued to improve of late, with WIRP pricing for a rate hike in July rising back over 50%. With oil increasingly looking like it has passed its cyclical low, energy’s deflationary impact on headline CPI is set to fade throughout the year. These developments mean that the Fed is likely to strike a noticeably more hawkish tone next week and make it clear to the markets that rate hikes could occur in June or July. As if to emphasise this case, US initial jobless claims overnight dropped to 259,000, their lowest level since October 2015.

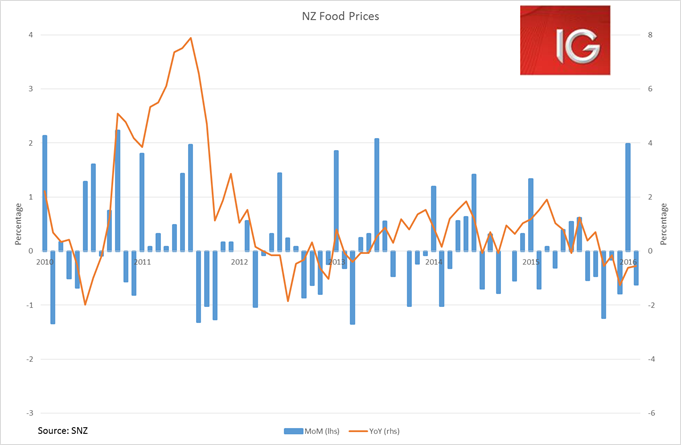

The need for yesterday’s RBNZ rate cut was given further credence with today’s release of February food prices. After surging in January, NZ food prices declined -0.6% MoM in February. This makes it the fifth straight month of outright YoY food price deflation in New Zealand, and does not bode well for New Zealand’s 1Q CPI performance. We think inflation is likely to be weak enough to warrant another cut by the RBNZ at their June meeting.