On negative gearing, the BCA has called for the quarantining of investment losses so that they can only be deducted against investment income, not unrelated wages and salaries, with net losses carried forward:

Any changes to negative gearing should be considered in the context of the tax treatment of other savings – where housing is just one asset class. As stated in the Henry review, a more neutral tax treatment of savings would ‘encourage households to seek the best pre-tax return on their savings and to invest their savings in assets that best suit their circumstances and risk-preferences’…

Any changes to negative gearing or other arrangements should align with the overarching objective of promoting more efficient savings and undistorted investment allocation…

A more neutral, concessional treatment of other forms of capital income could be achieved via a dual-income tax approach. This would be more equitable (particularly for those people who are constrained to save via interest-bearing deposits) and economically efficient.

Under a dual-income tax approach, interest and other property expenses could only be offset against rental income, which would still be taxed at a concessional rate. Losses would be carried forward until properties were sold and (concessional) capital gains tax paid. This would offer immediate revenue savings (depending on the discount on rental income), offset by lower capital gains tax receipts in future.

Any changes to negative gearing would need to be phased in or grandfathered to avoid fire sales of properties and negative impacts on existing borrowers. The impact on rental markets would need to be assessed.

The BCA also backs lowering the CGT discount, which is too generous:

Advertisement

There is value in exploring the Henry review proposal to reduce the capital gains tax discount to 40 per cent, but only in the context of longer-term changes to establish more consistent concessional taxation of all savings income. The consequences could be severe if changes are made that do not take a holistic approach to the taxation of savings.

If changes were made, existing asset holdings would either need to be grandfathered or a gradual reduction in the discount phased in…

The cost of the discount is significant

In 2015-16 the CGT discount on assets owned by investors for at least 12 months is estimated to be around $6 billion…

The current discount of 50 per cent may be generous, particularly in a low-inflation environment…

A way forward

Explore reducing the capital gains tax discount to 40 per cent, but only as an initial step towards more consistent concessional taxation of other forms of savings income (for example, in moving towards a dual-income tax system). Existing asset holdings would either need to be grandfathered or the reduction in the discount phased in. Grandfathering would push out savings for many years.

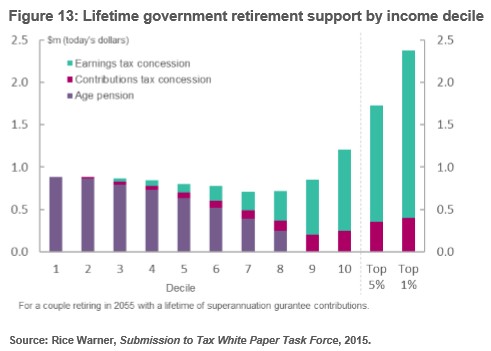

Some other highlights from the BCA report include backing reforms to superannuation concessions, noting that the system should encourage comfort in retirement but not “large-scale wealth accumulation”:

There are concerns that the superannuation system allows high-income earners to accumulate wealth at concessional tax rates and that the system is not cost effective.

The distribution of total concessions is skewed towards the highest-income earners…

In the Business Council’s view, the dual purpose of the retirement income system should be to provide for comfortable living standards during retirement, and to reduce reliance on the age pension.

Concessional tax treatment of superannuation should remain. However, there should be reasonable limits on the total balance of superannuation accrued through concessions. The tax system should facilitate superannuation balances large enough to provide for comfortable living standards during retirement, not large-scale wealth accumulation.

Any reforms must be undertaken with a clear sense of how the changes will achieve these policy goals, and a careful and holistic analysis of the interactions between the three pillars. Appropriate transitional arrangements that account for the long-term horizons over which retirement decisions are made will be necessary…

There are modest steps which could make superannuation fairer and more sustainable

Initial changes to the tax treatment of superannuation should include:

Advertisement

adopting clear objectives for the superannuation system to guide policy changes.

some tightening of annual concessional and non-concessional contributions… Caps should be indexed and carefully calibrated so they do not undermine building comfortable retirement incomes addressing impediments to greater use of annuities.

Tightening of concessional tax treatment of superannuation should be accompanied by more consistent concessional treatment of non-superannuation savings income.

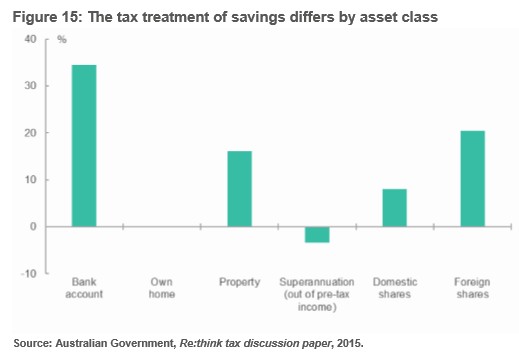

The BCA also wants more neutral treatment of different classes of savings:

Currently, capital income from different forms of investment in Australia is taxed very differently, some at concessional rates and some not, leading to inefficient investment allocation and perceived unfairness.

Ideally, income from savings should be taxed at a lower rate than current income to counteract the compounding effects of taxation, which generate higher effective marginal tax rates that erode the value of savings and discourage deferring consumption to the future.

There would be efficiency gains from more consistent concessional treatment of different forms of savings income such as capital gains, rental income and interest on savings deposits.

Advertisement

It also backs switching stamp duties for land taxes:

A broadly applied, well-designed land tax is efficient and has little impact on incentives to invest, work and save. The marginal excess burden of a broad-based land tax is estimated to be negative – that is, raising land taxes would deliver an economic benefit. The benefit would be even larger if the revenue is used to remove more economically harmful taxes like stamp duties.

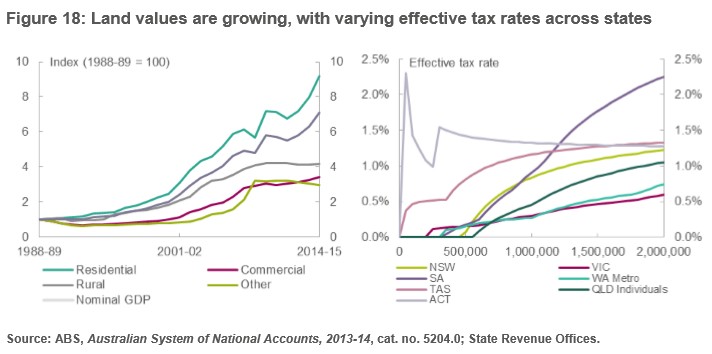

Currently around 60 per cent of the value of land is exempt from land tax. Exemptions apply generally to owner-occupied housing and land used in primary production. Land tax largely applies to a limited range of commercial and investor-owned residential land and holiday homes. Significantly, these exemptions exclude from the tax base the land with the fastest recent growth in value.

There are also large variances in the land tax rates and base across states. For a property valued at $600,000 the effective land tax rate varies from 0 to 1.39 per cent, with a range of rates and thresholds.

As a rule of thumb, an effective tax rate of around 0.2 per cent could be applied to all land (no exemptions) to raise the same amount of tax revenue as today.70 In 2013-14, states raised $6.4 billion in land tax on land valued at about $1.7 trillion,71 but total land values were $4.2 trillion…

The land tax rules should be harmonised across states and the base expanded. Uniform rates would be ideal, but it would be possible for states to continue to set the land tax rates so they can adjust to their particular circumstances.

These reforms are difficult and transitional arrangements would need to be carefully designed to manage the switch from taxing property and insurance purchasers to all owners of property…

Ideally, a reformed land tax would only apply to the unimproved value of the land, so there is not a disincentive to improve the land. Council rates could be used as the base for a low-rate broad property levy.

There may be circumstances where the land owner is asset-rich but income-poor (for example, some retirees). An optional loan arrangement system could be introduced so that the tax is paid when the property is sold, with interest imposed on the outstanding amount. Such arrangements currently exist for some local government rates.

Overall, the BCA report is good, and is effectively a throwback to the Henry Tax Review’s recommendations.

There are, however, some howlers in the report, including the below critique of Labor’s negative gearing plan, which is nonsensical (my emphasis):

Advertisement

Limiting negative gearing to new dwellings would distort the housing market. Currently, most negatively geared properties are existing dwellings, presumably reflecting demands in the rental market and that new housing will always be a relatively small share of the total housing stock.

If negative gearing is confined to new dwellings, investor demand will shift to new dwellings, pushing up prices of new dwellings in the short term (given a less than perfectly elastic supply response) and crowding out owner-occupiers. The price of the existing housing stock will decline immediately. The availability of rental accommodation in existing dwellings will also tend to decline and rental prices increase. Owner-occupiers will shift to the existing housing stock.

Overall there would be a likely decline in demand for housing… Only expanded supply of housing can increase the housing stock and keep a lid on prices.

The BCA obviously has not thought Labor’s plan through. Overall rental supply would be increased as the construction of new homes is boosted, thus pushing down rents overall. There would also be no impact on rents for existing homes, because any reduction in rental supply brought about by Labor’s policy would be matched by a corresponding drop in rental demand as renters shift to becoming owner-occupiers. It’s not rocket science.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.