While debate is raging over whether to give the states income taxing powers so that they can better fund health services. the Australian Greens have come up with an alternative plan to fund the revenue shortfall in health by phasing out the private health insurance rebate.

Here’s Greens leader, Richard DiNatalie explaining this plan last night on ABC’s Lateline:

TONY JONES: Alright. Now you want the Commonwealth to have even more skin in the game. You’ve come up with a plan costed by the Parliamentary Budget Office to save billions of dollars that’d be funnelled back into the public health system. How would it work exactly?

RICHARD DI NATALE: Well, what we had introduced under Howard was the – a range of measures to try and increase uptake of private health insurance. You had lifetime loading, you also had the private health insurance rebate. Now lifetime loading increased the coverage of private health insurance. The rebate did very, very little except waste a lot of money and not achieving its stated public policy objective, which was to take the pressure off the public hospital system. What we’re saying is that you’ve got now approaching $6 billion of taxpayer money that goes to subsidise people with private health insurance and it’s not achieving what we want it to achieve and that is taking pressure off the public system. Instead what you’ve got is a range of junk policies that have been created as a result of the incentives in the system.

TONY JONES: Well let’s have the discussion about what the impact of the private health rebate is. First, tell us what you’re going to do with it if you …

RICHARD DI NATALE: Yeah.

TONY JONES: Under your plan, what would you do with it?

RICHARD DI NATALE: Well, well, every cent goes back into the public health system and it’s enough to fund …

TONY JONES: So you’d cut it completely, get rid of it?

RICHARD DI NATALE: Well it would be phased out and every cent reinvested back in the public health system to fund hospitals, to fund primary care and to fund services like dental care. Let’s remember, this is worth close to $6 billion a year now and it’s not achieving anything in terms of the promise that was made, which was: we’re going to take the pressure off the public hospital system. What happens instead is that people with private health insurance still opt to use the public system, they’re given a whole range of ancillary benefits, a whole range of therapies, some of which are of questionable benefit, funded by the taxpayer, and then you have these incentives created which mean you’ve got these junk policies that do nothing except allow people to avoid paying the Medicare surcharge levy…

The Parliamentary Budget Office have costed the proposal. We know that it would save in the order of $10 billion if it’s phased out over four years and we’re proposing a phase-out with a 10 per cent reduction of the rebate per annum over the forward estimates. If you look at over the next decade, you are talking about savings in the order of $50 billion. That’s the quantum you’re talking about. It’s a huge reinvestment back in the public health system, back into hospitals, back into allied health care, dental services – all the things that we know are the cornerstone of good healthcare.

I believe there is a lot of merit in the Greens’ proposal.

Spending $6 billion a year (and growing) subsidising private health insurance is a poor use of taxpayer funds for several reasons (see Professor Lesley Russell’s article for a detailed examination).

First, like the first home buyers grant, such subsidies are likely to be inflationary and lead to higher health premiums, other things equal. Thus, taxpayers are paying through their taxes to keep private health insurance ‘affordable’, but are not achieving this outcome.

Second, the increase in services delivered in private hospitals has done little to ease the pressure on public hospitals and in fact waiting times for urgent procedures in public hospitals has increased.

Third, private health insurance has not improved quality and safety. The Productivity Commission found that the larger, most comparable public and private hospitals have similar adjusted premature death ratios. Team-based care in large public hospitals also tends to result in better care coordination.

Fourth, private patients are often ‘stung’ by unexpected costs that they thought they were covered for. For example, more than 20% of private care is paid for by patients’ out-of-pocket costs, which in 2014 averaged A$285 per hospital episode.

Fifth, the ACCC’s latest report to the Australian Senate on competition and consumer issues in the private health insurance industry found that Australia’s private health insurance industry is characterised by market failures due to asymmetric and imperfect information, as well as significant complexity.

The mix of levies, surcharges and rebates – and funds that constantly change their policies – make it difficult for even astute consumers to judge the true cost and value of their private health insurance. Many people know little about the policy they purchase – what it covers, how much it covers, whether it is good value and suited to their needs.

Sixth, around a quarter of people with private health insurance choose to use the public system. Accordingly, a significant proportion of the private health insurance rebate is effectively wasted as people purchase cover for financial rather than health reasons.

Finally, as explained beautifully by Ian McAuley, single national insurers tend to keep costs down.

The high financial overhead of private insurance in Australia means that only 84 cents in every dollar collected by private insurers is returned as benefits, with the rest going to administrative costs and corporate profits. By contrast, Medicare returns 94 cents in the dollar, even after the cost of tax collection is taken into account.

In the United States, which is highly dependent on private insurance, only 69 cents in the dollar are returned as payment for health services.

More importantly, competing private insurers have less ability to control prices demanded by powerful service providers. If one insurer tries to bargain hard with hospitals to keep prices down, the hospitals simply choose to do business with another insurer.

By contrast a single national insurer has the market power to push down costs and improve utilisation.

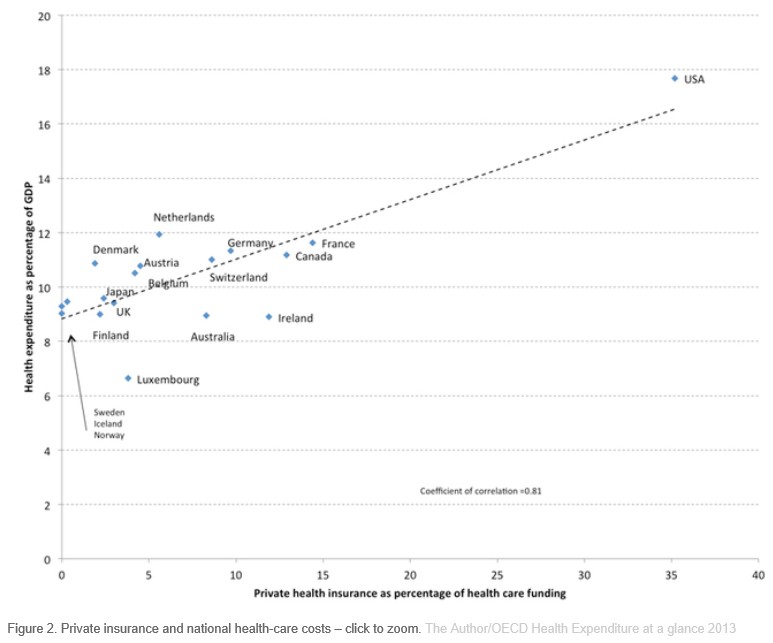

The below chart of health costs across 18 OECD countries highlights this point: single national insurers provide cheaper (and often better) health care than systems heavily reliant on private health insurance:

The Greens are right. Private health insurance is both an expensive and cumbersome way to achieve what Medicare and the tax system does better: effectively manage of health care costs and provide care to those that need it most.

unconventionaleconomist@hotmail.com