Arrium sits on the cusp of voluntary administration essentially because its board and two generations of management have failed to identify and then cull the steel elephant in their midst.

The weary bull elephant in question is the Whyalla Steelworks and it has been plain enough for half a decade at least that it had to go. And this is not just informed retrospection.

From the earliest days of what was so very nearly an acutely timed diversification up and down the steel manufacturing industry, it was apparent that Arrium should have been planning an exit from raw steel making at Whyalla.

Even through the best of the steel cycle over the past decade or so, Whyalla struggled to make an acceptable return on capital. In 2009, when Arrium’s steel business last made anything like an acceptable return on its investment, Whyalla was struggling to remain relevant. And that was, and is, not for want of trying.

…The problem Arrium has with steel is not that it is a wholly bad business but that the company has burned too much precious time and capital attempting to secure a steel-making legacy that has consistently failed to justify that investment.

But the reason Arrium launched this last-ditched defiance of it lenders’ demands is that the leadership remains obsessively concerned for the fate of Whyalla. Arrium believes that the first thing the bankers’ preferred administrator would do would be to shutter an obviously unfinancial Whyalla.

There is some rather selective memory here. In 2012 ARI rejected a takeover bid from Korea’s Posco at 75 cents per share. It wanted the steel business. It is not publicly known but is a fact that there was another counter bid in the market at an even higher price that was also focused particularly on rejuvenating the steel business. It is not Whyalla that has killed ARI, it is calamitously stupid management choices.

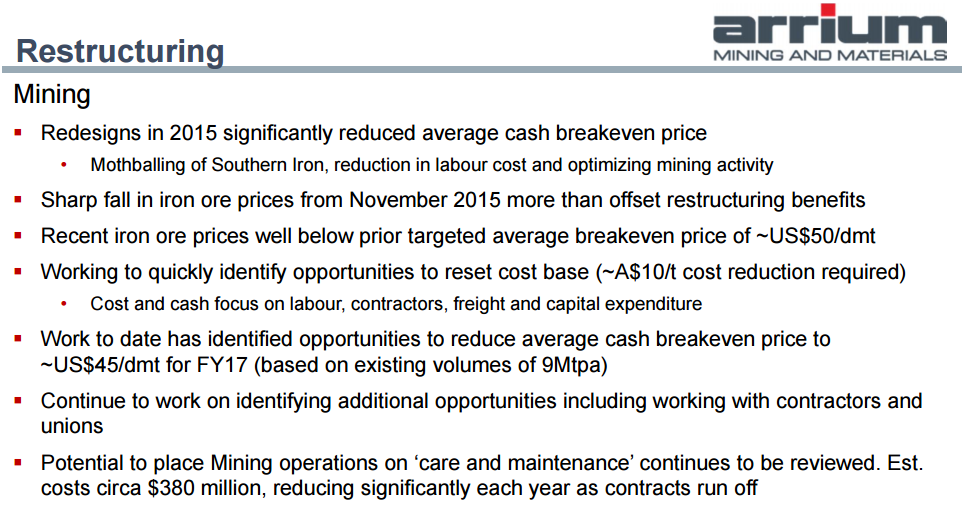

Even today it is the iron ore business that is much harder to restructure successfully than the steel business:

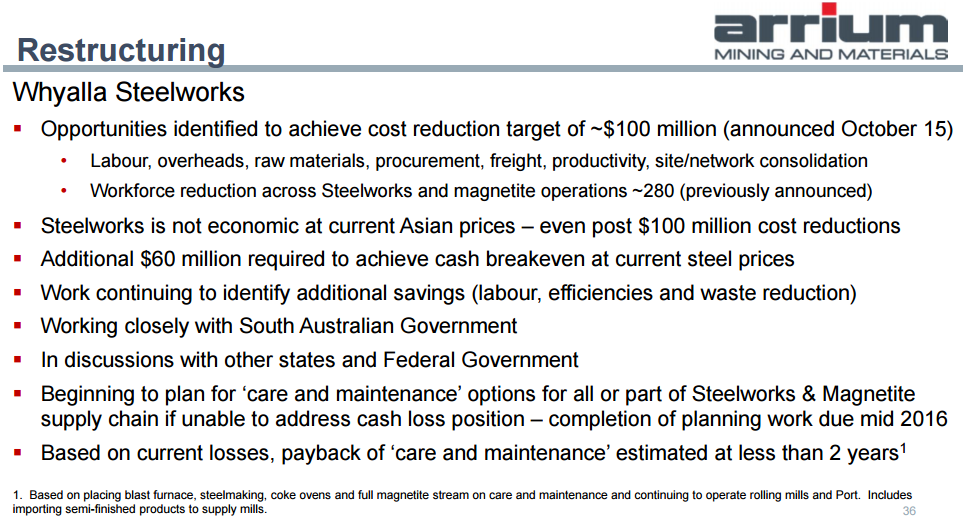

Steel needs to find $60 million in savings, will benefit from the global spread of anti-dumping trade protections and a lower currency over time and, as Bluescope is showing, with sensible investment and cost-out could make loads of money. The iron ore business on the other hand is doomed with a best case of $380 million to restructure and a break even at $40, roughly double where the iron ore price is headed in the next two years. As well, in ARI’s recent labour cost cut vote, it was iron ore miners that rejected pay cuts not steel workers. Moreover, as the iron ore price continues to collapse the steel business will see much better margins so long as it is not mining the dirt.

Arrium’s only viable future is steel but, alas, it appears the great Australian consensus can only see value in a hole in the ground.