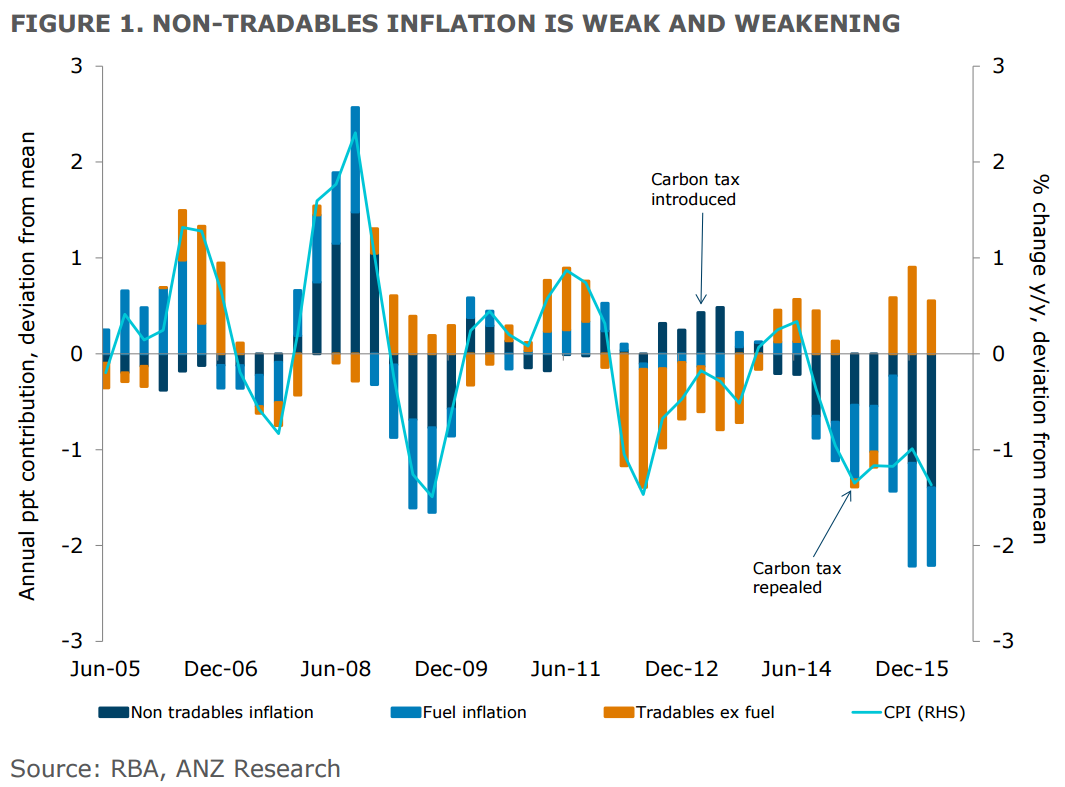

The ANZ has a nice study of the forces at work in Australian disinflation today. First, wider disinflation:

The weakness in the Q1 CPI came as a surprise to many. The RBA explained the low result as “broad-based weakness in domestic cost pressures, reflecting low wage growth, heightened retail competition, softer conditions in rental and housing construction markets and declines in the cost of business inputs”. Certainly the weak global inflation pulse and increased international competition are weighing on domestic prices (see our Economic Insight published 19 April 2016), but it’s the deceleration in non-tradables inflation that appears to have caught policymakers most off guard. Indeed, there has been a marked deceleration in non-tradable inflation in the past two quarters, with the drag relative to the mean contribution now more significant than any time in the past decade (see Figure 1). While tradable inflation is weaker than one would expect given the depreciation of the currency, it is contributing more than average to current inflationary pressures.

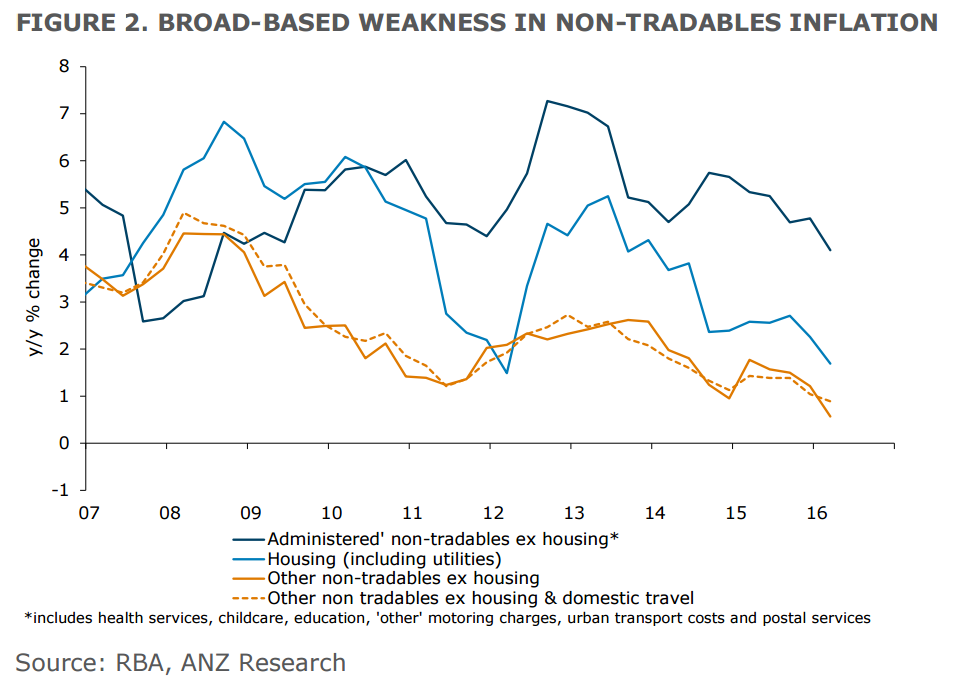

As we have written about previously, administered goods ‘are what they are’, while housing-related prices have moderated faster and further than expected. Indeed, housing inflation (which includes rents, new dwelling purchase prices, and utilities) moderated to 1.7% y/y in Q1 2016 from 2.6% y/y a year earlier. Rental growth is running at 20 year lows while new dwelling purchase prices have weakened substantially in the past two quarters (having been a key contributor to inflation in 2014-15).

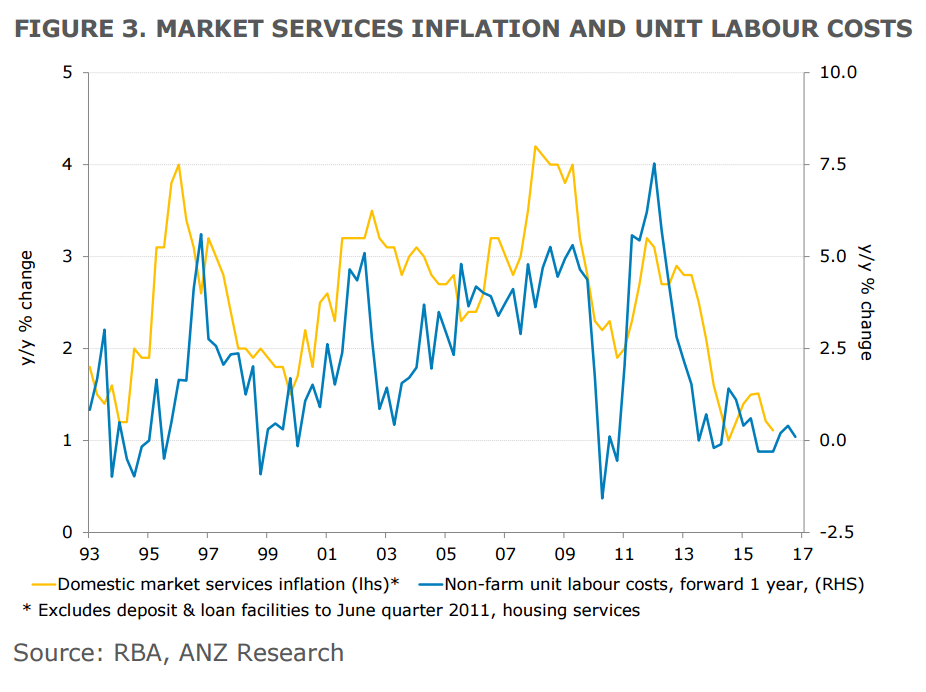

A more specific definition for ‘other non tradables’ is domestic market services. Given that services are labour intensive, it is no surprise that these prices have a strong relationship with wages (see Figure 3). As a result, the outlook for wages growth has been thrown into the spotlight.

Second, wages disinflation:

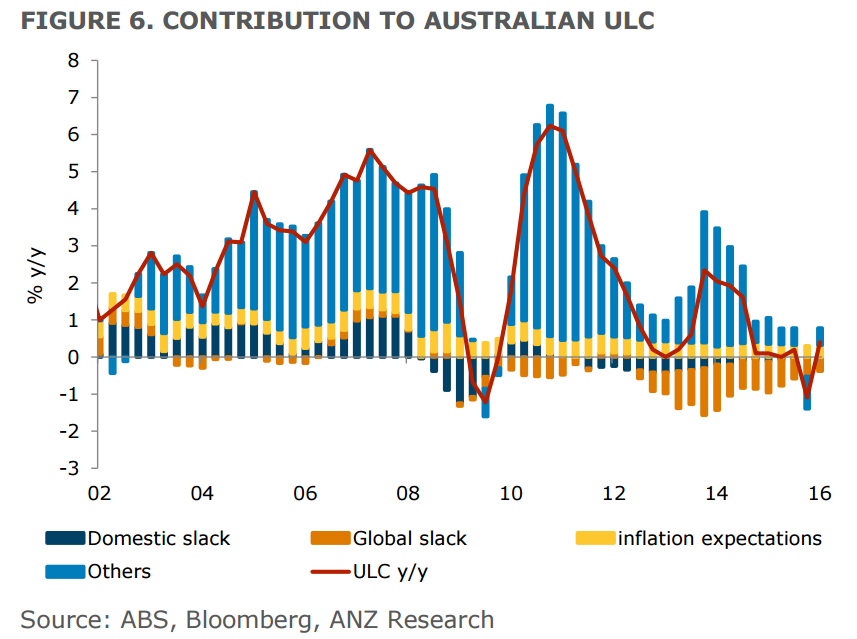

Wage pressures are partly being held down by domestic spare capacity. Although the unemployment rate has fallen, it remains above the 5-5¼% level generally considered as full employment…our modelling suggests that disinflationary tailwinds coming from overseas have been a sizeable drag on domestic wages since mid-2012 (see Figure 6). That drag peaked in early 2014 and has been diminishing since then.

This seems to me backwards. Most services are non-tradable so global pressures are not acting directly upon them. It is the other way around mostly as the mining boom (tradables) wage inflation spilled over into non-tradables wages but is now unwinding:

Advertisement

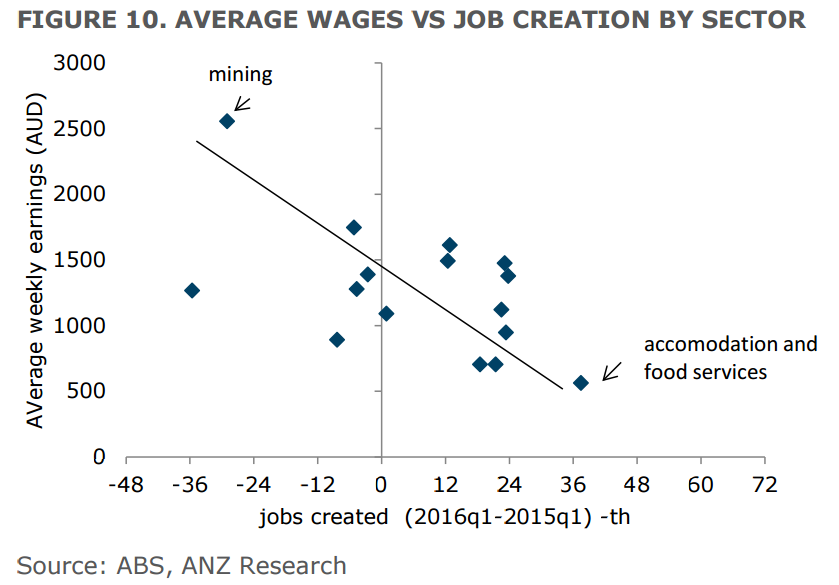

Industry composition. Job growth recently has been concentrated in lower-paid jobs in the services sector and this is proving to be disinflationary. The rebalancing towards services will likely remain a drag over the short term.

Thus the global impact in local wages in intensifying and has years yet to run as mining shakes out.

ANZ lists a range of other factors that are part of the weakening:

Advertisement

Flexibility. Non-standard flexible forms of employment – such as temporary, casual, or part-time work contracts – have become very common across advanced economies, especially after the GFC. In Australia, the share of part-time workers has jumped by roughly 30% over the last nine years. Flexible contracts make it easier to fill positions without having to raise wages and – by making positions more fragile – they cut workers’ bargaining power and raise job insecurity (Figure 11). In Australia, job insecurity spiked after the GFC, fully retraced courtesy of the mining boom, and has since deteriorated again as jobs growth switched towards the more flexible services sectors.

Demographics. Sluggish wage growth may also be driven by demographic shifts in the composition of the labour force. Specifically, the exit from full-time employment of (higher wage) baby boomers – as they increasingly retire or shift to part-time positions – is weighing on aggregate wages.

A lot of this is to be expected in a post-mining boom environment. I mean, we seriously overdid it:

Advertisement

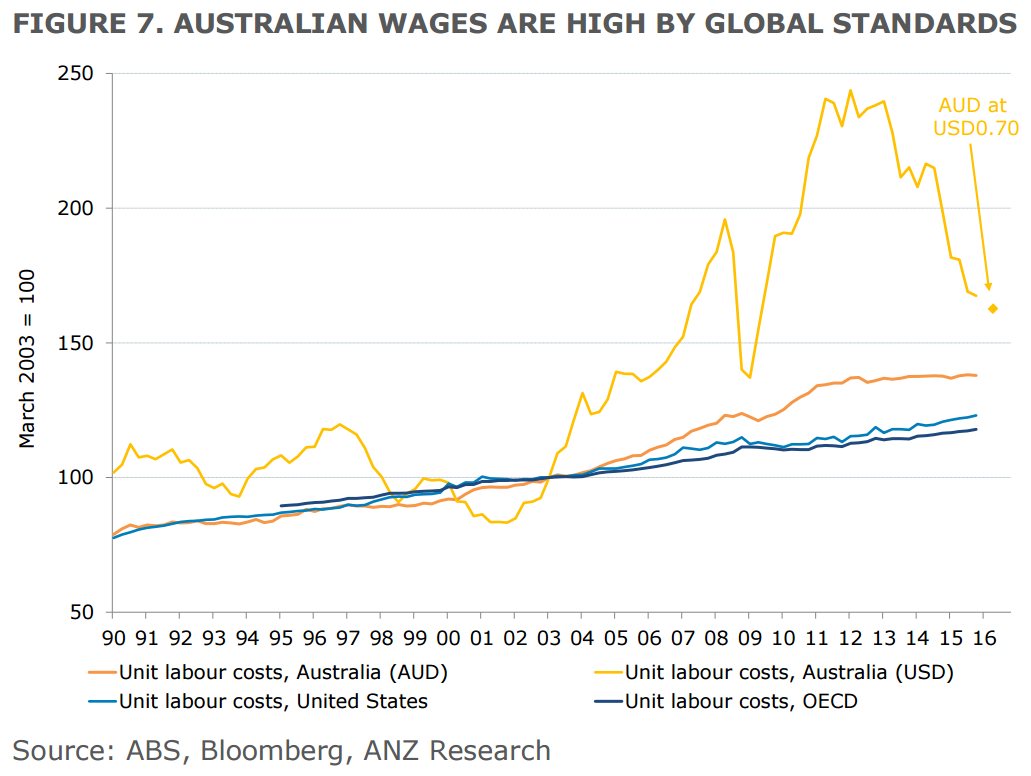

This is why I obsess over lowering the dollar. It absorbs an huge amount of the deflationary pain in repairing one’s competitiveness rather than doing it internally vis-a-vis Europe’s PIIGS.

That is also why authorities have made such a hash of the adjustment by at first denying the mining bust was happening and then inflating debt and asset prices to offset it when they found themselves behind the curve.

They thus levitated the dollar throughout, hammering tradable wages harder than otherwise and spilling it out more widely now. Worse, we now have the debt overhang to deal with and another adjustment to face in non-tradable sectors related to households once the post-mining boom adjustment abates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.