An expected slowdown. After the strong 4M16, the full set of REI data points to slower growth in May, as expected. Although the growth may slow further in June, along with the high-base effect, we believe the market is overly bearish on full-year growth. Even if we assume 0% growth in the rest of the seven months, home sales should still increase by 14%, and GFA sold should increase by 9%. New starts should be up 6% while REI should gain 2%. These suggest that the sector is still in an upcylce like 2013.

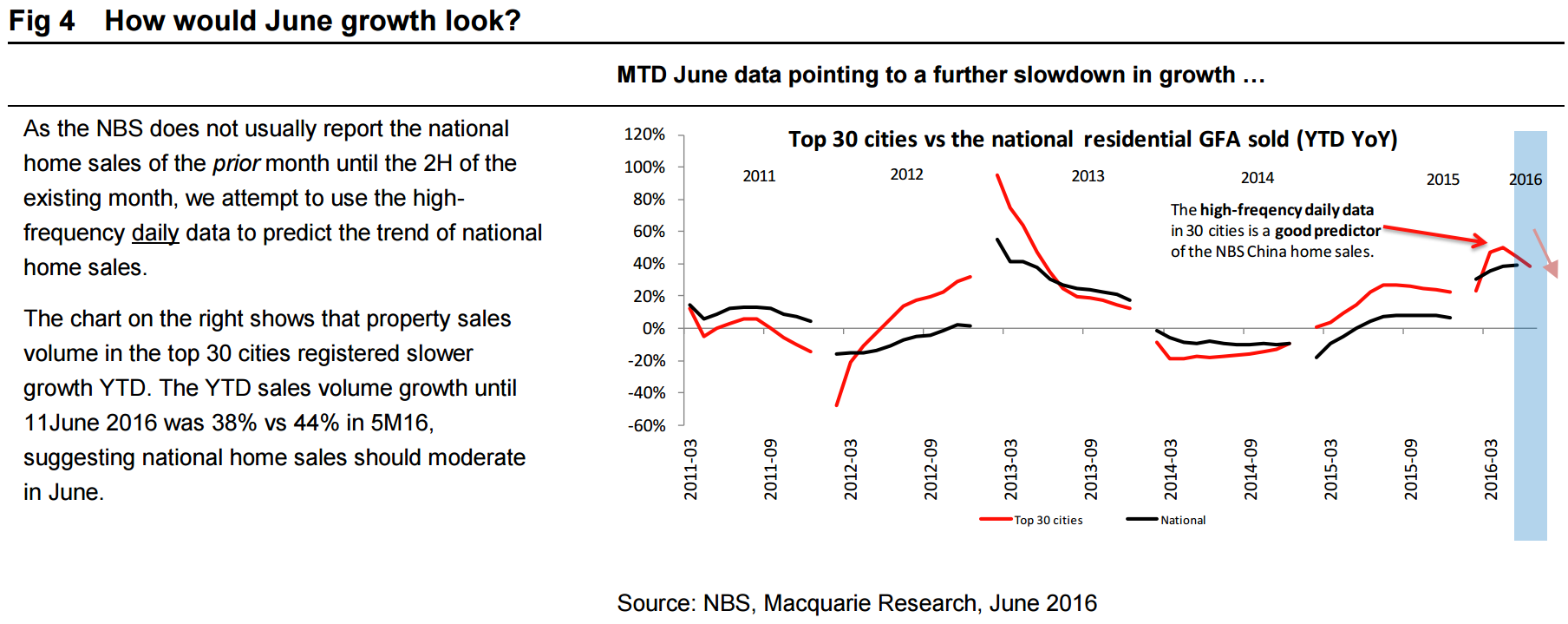

Home sales slowdown, especially Eastern China… The slower sales growth in 5M16 to 50.7%, vs 54.1% in 4M16 was mainly due to the larger slowdown in Eastern China, where growth decreased to 39% YoY in May from 71% YoY in April, reflecting cool down measures in some T1 cities and some T2 cities taking effect. However, non-residential sales were robust. In 5M16, sales of offices registered faster growth, up 73% YoY vs 60% YoY in 4M16. Sales of retail units rose 21% YoY in 5M16 vs 15% YoY in 4M16.

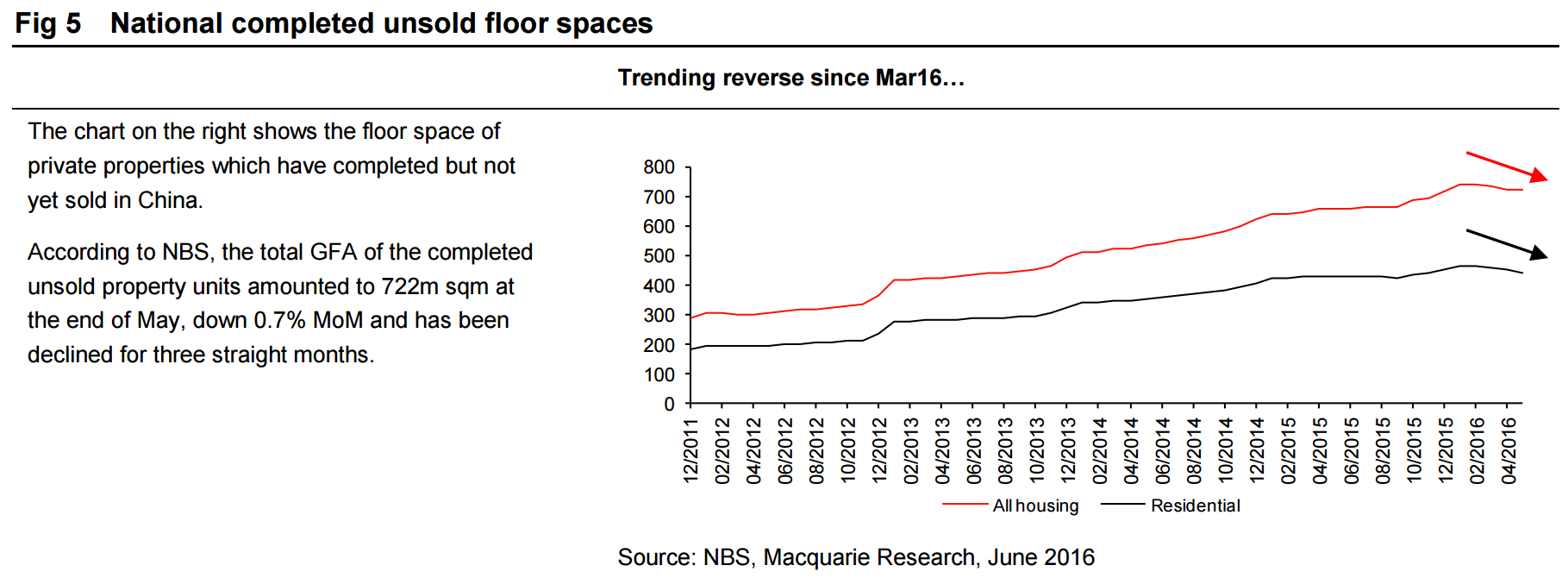

Inventory clearance on track. The strong home sales have been mainly driven by growth of GFA sold (5M16: ASP +13.1%, GFA+ 33.2%) which is in sharp contrast to the recovery in 2015, which was slightly more ASP-driven (2015: ASP +7.4%; GFA +6.5%). In particular, ASP growth in 5M16 was slower than the 14.2% growth in 4M16, suggesting more contribution by home sales in lower-tier cities. Completed unsold GFA (Fig 5) declined for three consecutive months, down 0.7% MoM to 722m sqm at the end of May. Because of soaring land prices, land sales (Fig 11) surged by 104% in value in May but merely increased by 1% in GFA. This suggests that new starts are unlikely to keep the growth strong, although REI, which measures the value of growth, may stay relatively robust.

Inventory clearance “on track”. Sure, if a barely perceptible slowing in the uptrend and more recent reversal upwards is “on track”. And this is only tiers 1&2. In the tier 3&4 cities there is no change.

Chinese realty will slow as the year runs on and floor space under construction will slow with it. I still expect new starts growth to fall away all year and gross floor space under construction to end flat.

The short answer to the question is China clearing it’s housing glut is “no”, that will only happen when prices fall enough to make property affordable.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.