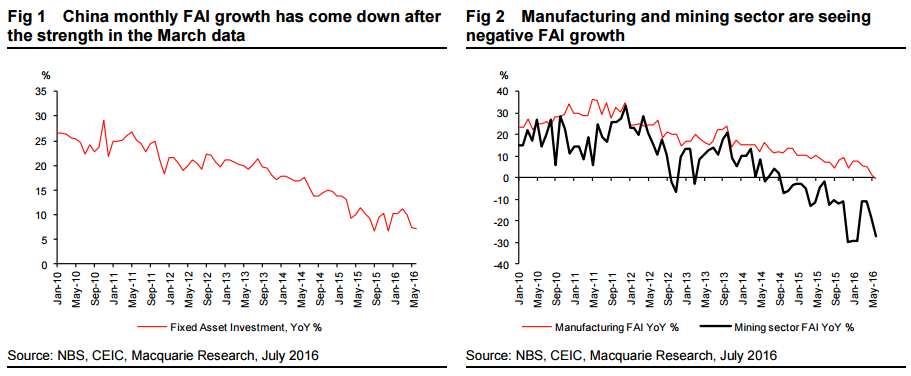

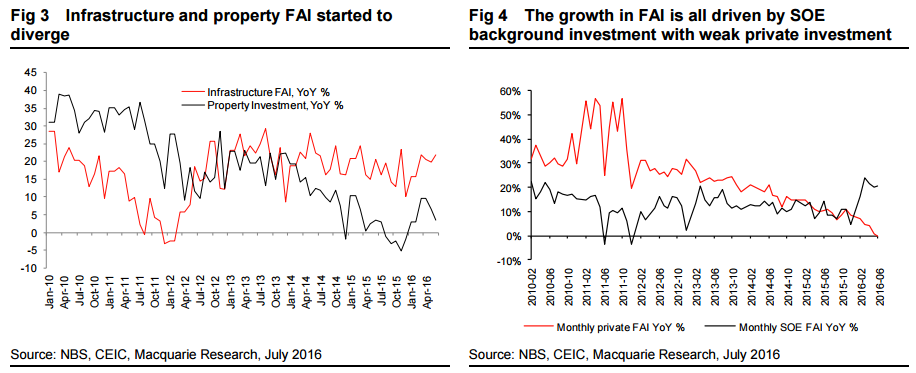

China FAI growth rate continued to slow in June, with YoY growth falling from 9.6% in Jan– May to 9% in Jan–June. Calculated monthly gives a clearer picture on its trend, which shows the FAI growth rate peaked in March at 11.2% YoY, dropped dramatically in May to 7.4% YoY and further declined in June to 7.3% YoY. If we look at the breakdown of FAI, we see the March pickup in FAI growth was mainly driven by infrastructure investment, which increased from 15.7% YoY in Jan–Feb to 22% YoY, and also property investment, which jumped from 3% YoY in the first two months to 9.7% in March. Meanwhile, investment from manufacturing was in a downtrend from the start of the year, and mining sector FAI continued to contract rapidly (Fig 2).

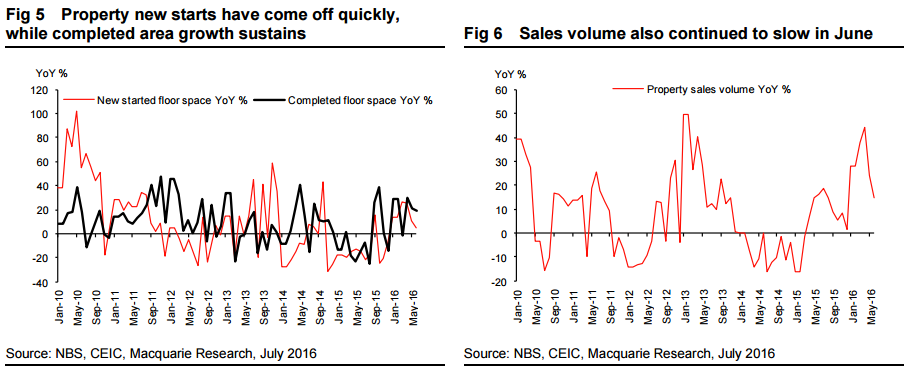

However, as property investment growth rate fell to 6.6% YoY in May, total FAI also started to fall back despite infrastructure investment holding at around 20% YoY. This divergence became more apparent in June, when we saw property investment further drop to 3.5% YoY from 6.6% YoY in May, while infrastructure growth rebounded modestly, from 19.8% YoY to 21.8% YoY. This is in line with the results from our recent steel survey, where construction orders have weakened despite infrastructure remaining strong.

A big concern is that private investment, which accounts for more than 60% of China FAI, showed no improvement in June despite government efforts to boost this sector. Indeed the growth rate of private sector FAI was calculated to be flat YoY last month, compared with the 20% YoY growth from SOE background sectors (Figs 3 and 4).

Turning to the property sector, similarly to the slowdown in property FAI, new started floor space growth dropped from 10.6% YoY in May to 4.9% YoY in June, a big drop compared with more than 20% YoY growth in March and April. Looking in more detail we can see the drop was led by commercial building, including office and commercials, while residential was in a better situation but at a similar trend. Despite the slowing growth trend, starts remain well above our target of -3% YoY for 2016 as a whole.

Contrary to new starts, floor space completion remained strong in June, rising 18.8% YoY in that month. This means developers may be ramping up construction in order to sell before house pricing deteriorates, as notably floor space under construction went into contraction YoY in June. Property sales volume also slowed last month, down from 24.2% YoY in May to 14.6% YoY in June.

In terms of implications for metals demand, we believe the government will maintain robust levels of infrastructure investment in order to underpin the economy, particularly as the property market begins to slow and given ongoing concern about property inventories in lower-tier cities. Sustained infrastructure investment will be positive for metal demand, but the importance of property in the metals industry chain means there is still cause for concern. Time will be needed for manufacturing and other private sectors to regain confidence and cash flow to boost investment, and for many industries they still need to go through “supply-side reform.” This means the stronger-than-expected China metal demand in 1H may be difficult to sustain in 2H, although a further policy easing can be positive for market sentiment and boost short-term restocking demand.

That is precisely right though destocking is likely before restocking as demand falls.

This is an economy well advanced into “helicopter money” as the government orders banks to lend to infrastructure projects with the support of the central bank (notwithstanding new avenues for bond financing). The loans will never be repaid, at some point they’ll be taken to the woodshed and shot.

It works as a way of supporting China’s glide slope to lower and less commodity intensive growth so long as restucturing, reform and the shifting of income to households to support consumption is transpiring in the broader economy.

Advertisement

That’s the real worry, that the support is preventing the restructuring.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.