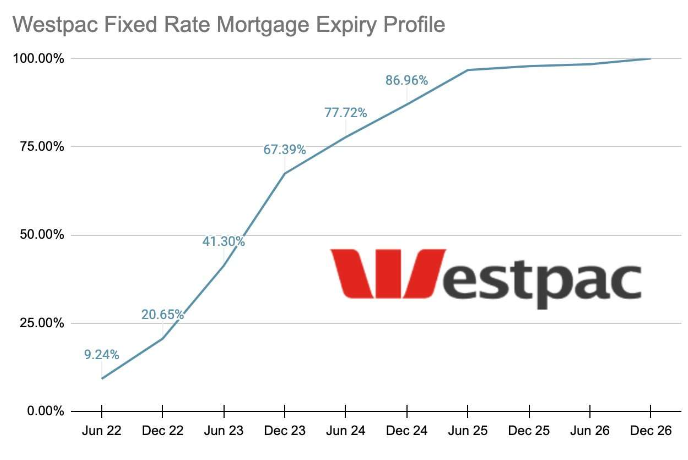

The ‘fixed rate mortgage cliff’ approaching in 2023 has been well documented and is best illustrated by the below chart from Westpac, which shows that by the end of 2023, the share of fixed rate mortgage holders that have not been hit with rising interest rates will plummet from 80% currently to around one-third:

Most fixed rate borrowers have yet to be hit by rising mortgage rates. That will change in 2023.

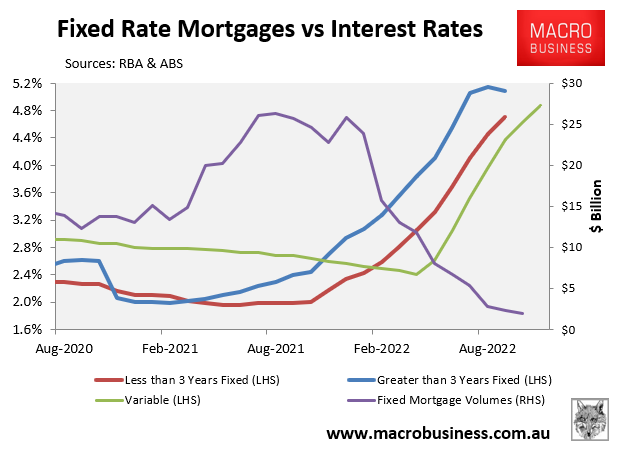

As illustrated in the next chart, there were huge volumes of mortgages taken out over the pandemic at rock bottom fixed interest rates of around 2%:

Borrowers took advantage of cheap fixed mortgage rates over the pandemic.

As the bulk of these fixed mortgage terms expire next year, borrowers are facing more than a doubling of their interest rates irrespective of whether they opt for a new fixed or variable mortgage.

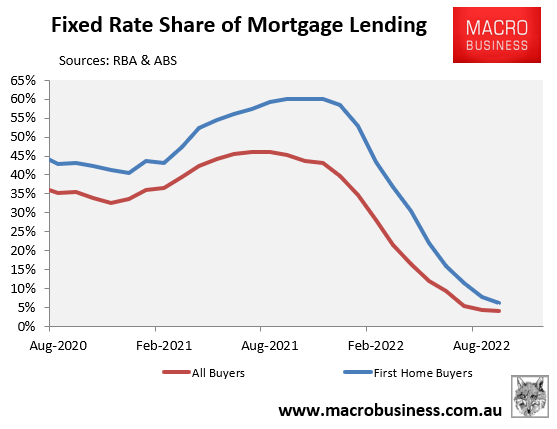

Recent first home buyers are most exposed, given their share of mortgages that were fixed rose to 60% over the pandemic, versus a peak of 46% across the broader market:

First home buyers dominated fixed rate lending over the pandemic.

Recent first home buyers are typically the most highly leveraged and sensitive to interest rate rises. Indeed, they are considered the ‘canaries in the coal mine’.

But because most recent first home buyers are still locked in at the very low interest rates that were offered at the earlier stages of the pandemic, large numbers of these households are yet to feel the impact of the Reserve Bank’s aggressive monetary tightening.

This will obviously change next year when the bulk of these fixed mortgages expire and are reset to rates that are at least double what they are currently paying.

Many recent first home buyers will face a toxic combination of negative equity and extreme mortgage stress.