This week, the Albanese Government released a consultation paper to enshrine an objective for superannuation in law.

That objective will be to “preserve savings and deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way”.

The consultation paper also notes that “there is a significant opportunity for Australia to leverage greater superannuation investment in areas where there is alignment between the best financial interests of members and national economic priorities”.

Several commentators have questioned the merits of Labor’s proposed superannuation reforms.

The Australian’s Judith Sloan warned that Treasurer Jim Chalmers believes super funds must serve societal purposes as well as investing for individuals. That is, they should invest in initiatives such as social housing and the care economy.

“The Treasurer essentially sees superannuation funds akin to an arm of government”, according to Sloan.

“He cites the examples of affordable housing, climate, the care economy and digital economy. He praises the involvement of industry super funds in social housing even though only one fund has announced a modest investment, with the other funds waiting for more information”.

The Herald-Sun’s Terry McCrann likewise warned that Treasurer Jim Chalmers has his sights on the biggest pool of money in the nation – the superannuation of ordinary Australians.

Specifically, Chalmers’ reforms would enable super funds to invest in projects that “boost housing supply, manage climate change and spur digital transformation”.

However, McCrann argues that super funds can do those things now, if it makes sense as an investment and will grow the super fund member’s balance.

Former RBA governor Bernie Fraser believes the federal government’s legislated objective for superannuation should include allowing people to use part of their accumulated savings to buy a home.

Fraser contends that there is no more comforting thought for Australians than knowing that they will have somewhere to live when they retire.

He has also questioned the government’s proposal to allow super funds to invest in social projects, noting that they tend to have low returns.

Brendan Coates from the Grattan Institute questioned whether investing in affordable housing schemes would be at odds with super funds’ requirement to act in their members’ best interests.

David Murray, who chaired the 2014 financial services inquiry, likewise added that super funds would already have exposure to affordable housing schemes if they were deemed to be attractive investments.

For mine, the bigger issue with Labor’s superannuation changes is that they do nothing to fix the critical flaws in the system.

Most notably, the bulk of superannuation concessions go to where they are not needed (i.e. high income earners).

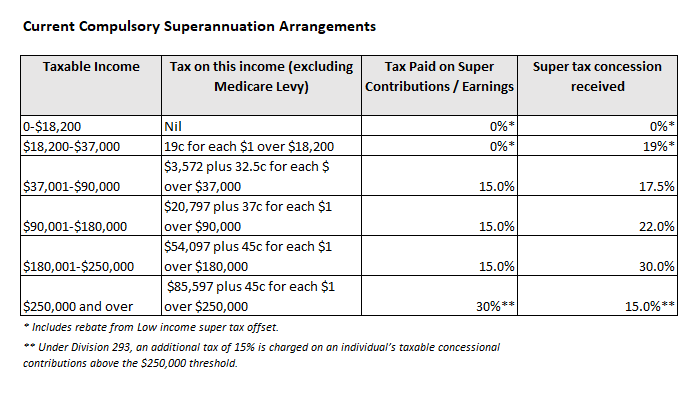

The 15% flat tax on superannuation contributions and earnings generally means those higher up the income scale receive the largest tax concessions:

Superannuation tax concessions generally favour higher income earners.

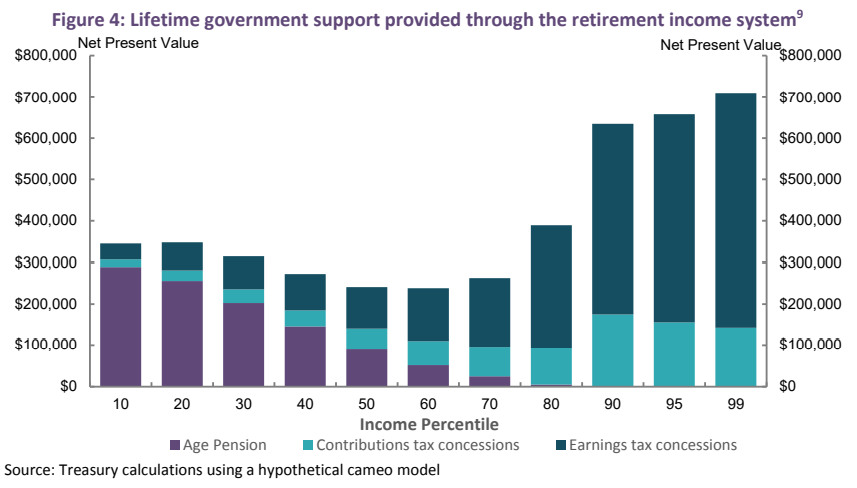

Futhermore, because the size of one’s superannuation nest egg is a function of how long one works and how much they earn, the lifetime taxpayer support provided through Australia’s retirement system is heavily skewed towards higher income earners, as illustrated in the below Australian Treasury chart:

The wealthy receive far greater retirement support than the poor.

It should ring alarm bells that Australian taxpayers spend more than twice as much supporting the retirements of the top 1% of income earners than they spend supporting someone on the aged pension, according to the Treasury.

For example, the top 1% of income earners are projected by the Australian Treasury to receive more than $700,000 in superannuation concessions over their working lives. That is roughly 14-times the $50,000 of concessions received by the bottom 10% of income earners.

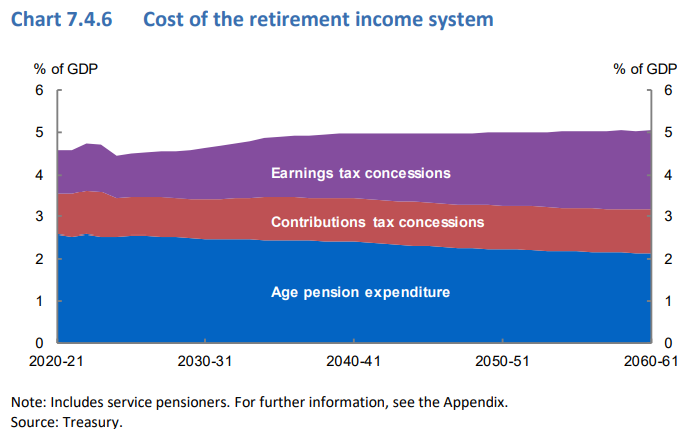

The above imbalances are one of the primary reasons why superannuation tax breaks will cost the federal budget a whopping $52.5 billion in 2022-23, almost as much as the aged pension.

Worse, the Intergenerational Report projected that Australia will spend more on superannuation concessions than providing the aged pension by around 2040:

Superannuation to cost more than the aged pension by 2040.

Finally, the Treasury’s Retirement Income Review warned that Australia’s superannuation system has transformed into a wealth accumulation and transfer scheme that is actually increasing inequality.

“Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests”, the review noted.

“Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”, the review warned.

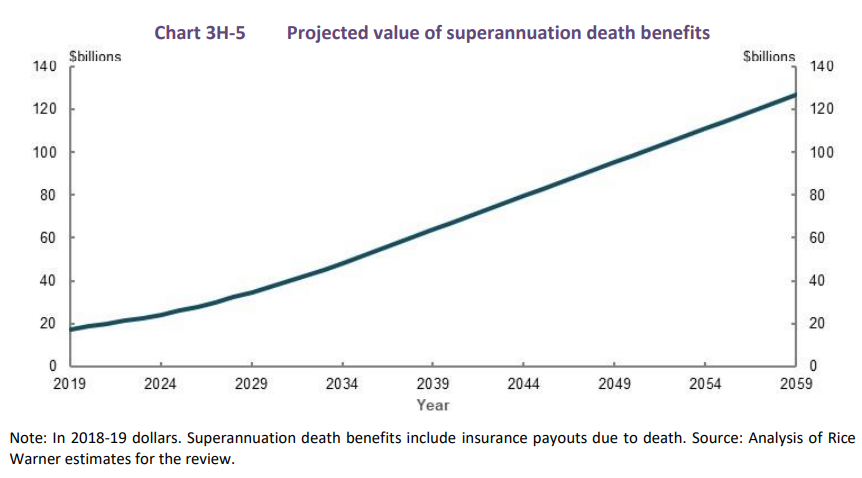

The next chart tells the tale. It shows that “superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059”:

Superannuation inheritances growing fast.

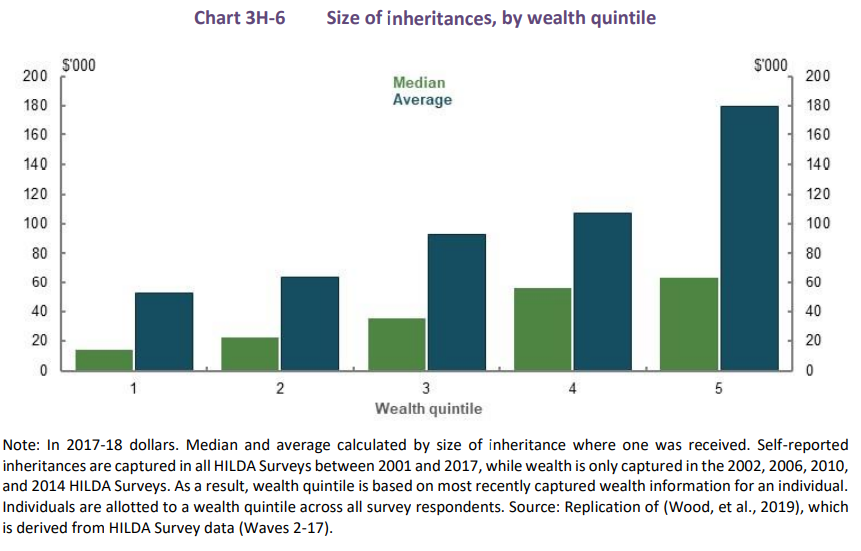

These inheritances are unequally distributed, with “wealthier people tending to receive larger inheritances than those with lower wealth”. As such, superannuation inheritances “increase intragenerational inequity”, according to the Retirement Income Review:

Superannuation inheritances increasing inequality.

Put simply, Australia’s compulsory superannuation system fails almost every policy mark, including:

- It is poorly targeted and largely misses those most in need (i.e. lower income earners).

- It costs the federal budget more than it saves in aged pension costs.

- It entrenches inequality by encouraging tax avoidance and wealth accumulation by the rich and their heirs.

Unless the Albanese Government addresses these fundamental flaws, Australia’s superannuation system will continue to fail, effectively taking the disparities in working-life incomes and magnifying them in retirement, thereby enshrining inequality.

Instead of undertaking the required root-and-branch reform, Labor has instead chosen to double down on the system’s failures by raising the superannuation guarantee to 12%.

In the process, Labor has chosen to increase superannuation’s cost to the federal budget.

That, in turn, will require other taxes to be higher than necessary, or will require other social programs (e.g. the aged pension) to be cut to make way for ballooning superannuation concessions.