The Australian Treasury’s Retirement Income Review complained that superannuants have been highly reluctant to draw down their nest eggs. Instead, they rely on their investment returns to fund their retirements.

In the process, superannuation has morphed into a wealth accumulation and transfer scheme that is increasing inequality, according to the review.

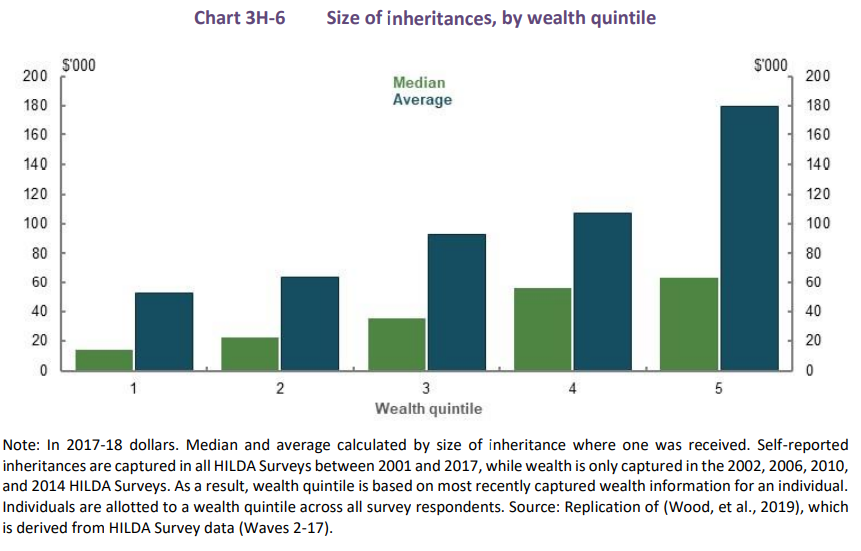

“Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests”, the review noted.

“Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”, the review warned.

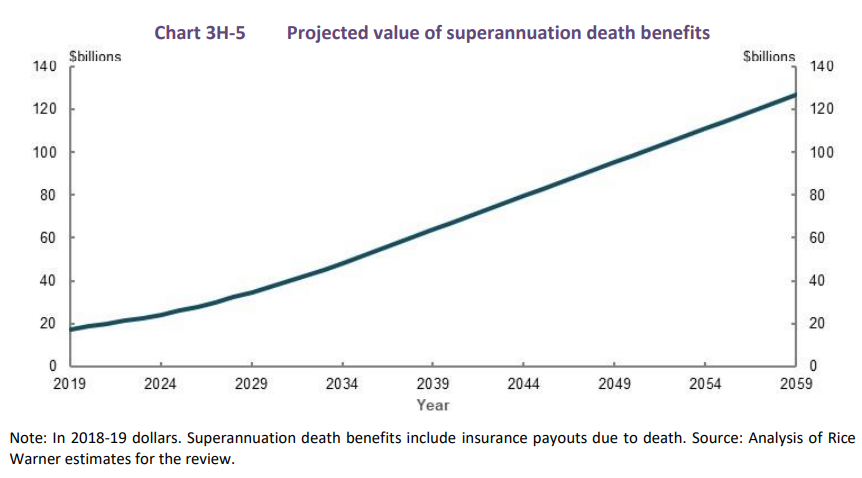

The review produced the below chart showing that “superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059”:

These inheritances are also unequally distributed, with “wealthier people tending to receive larger inheritances than those with lower wealth”. Therefore, superannuation inheritances “increase intragenerational inequity”, according to the review:

Recent research from Morningstar showed that “hundreds of thousands of Australians have no intention of running down their super to $1 on the day they die”.

Instead, Australians are using their superannuation “as more of a tax-advantaged savings vehicle than a source of retirement income”.

This research cites a bunch of surveys showing how the overwhelming majority of assets an average retiree enters retirement with remains unspent upon their death.

These surveys also show that most retirees wish to maintain most or all of capital rather than spend their capital to fund retirement.

When asked why they are choosing to maintain capital, nearly half nominated “for beneficiaries”.

Thus, the superannuation system is being used primarily as a tax effective tool to accumulate wealth to pass onto heirs, rather than as a genuine retirement instrument.

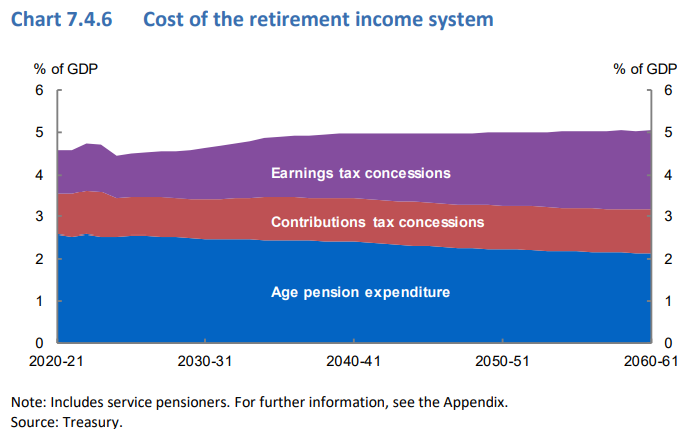

Superannuation concessions are projected to cost the federal budget more than the aged pension by 2060, according to the Australian Treasury:

Given this huge fiscal cost, alongside the negative equity impacts, the federal government must take concerted action to rein the superannuation system in.

It should start by abandoning further scheduled increases in the compulsory superannuation guarantee, alongside implementing strict accumulation caps and making superannuants draw-down their nest eggs.

Because maintaining the status quo will only worsen the long-term sustainability of the federal budget and increase inequality.