Of all the legal tax dodges in Australia, it’s hard to go past superannuation.

As noted this week by The Australian’s personal finance writer, Anthony Keane, “hundreds of thousands of dollars extra can end up in your pocket – rather than ATO coffers – if you use superannuation and tax rules to your advantage. Legally, of course”.

The superannuation system has literally been designed to favour of the wealthy.

The 15% flat tax on most superannuation contributions and earnings means that higher-income earners receive far more superannuation tax concessions than lower- and middle-income earners.

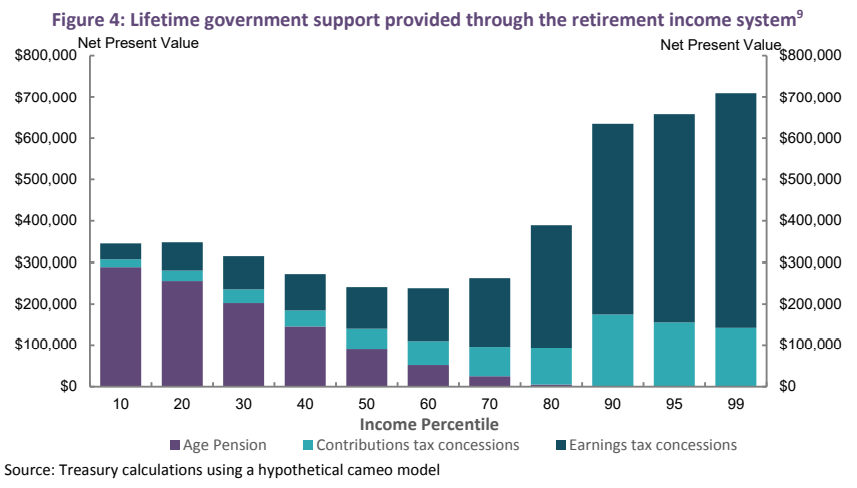

As illustrated in the Treasury chart below, Australian taxpayers spend at least twice as much supporting the retirements of the top 1% of income earners as they spend on somebody receiving the age pension:

That is, the top 1% of income earners are projected by the Treasury to receive more than $700,000 in superannuation concessions over their working lives. That’s roughly 14-times the $50,000 of concessions received by the bottom 10% of income earners.

It is no surprise, then, that there are more than 10,000 people in Australia with $5 million or more in their super accounts receiving at least $70,000 a year in tax concessions.

Because of these enormous tax breaks, Australia’s superannuation system has evolved from promoting retirement self-sufficiency to preserving family assets to pass on to children.

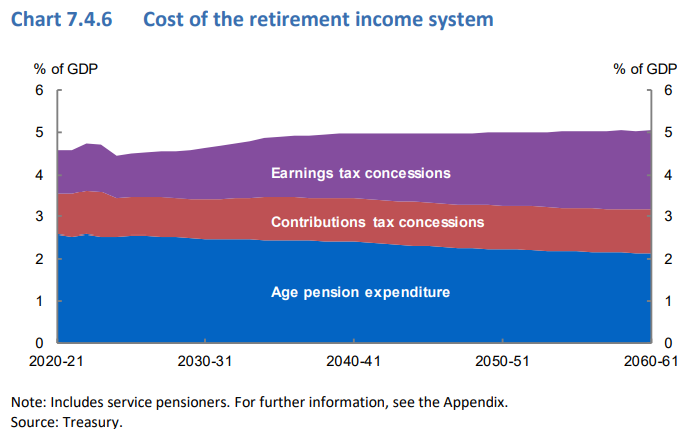

It has also meant that over the long term, superannuation tax breaks are going to become a bigger budget cost than the age pension, according to the Treasury:

The superannuation system basically takes the disparities in working-life incomes and magnifies them in retirement, enshrining inequality in the process.

At a minimum, further scheduled increases in the superannuation guarantee should be cancelled by the federal government, since they will only worsen the above inequalities and further damage the long-term sustainability of the federal budget.

Preferably, the compulsory superannuation system should be abolished altogether, with the billions in budget savings redirected into lifting the Age Pension, which is Australia’s true retirement safety net.