The Albanese Government yesterday announced that it will increase the concessional tax rate for superannuation balances of more than $3 million from 15% to 30%.

The tax reform will be included in the May budget and legislated during the current term of parliament; although it will not take effect until 1 July 2025, after the next federal election.

The super changes are expected to hit about 80,000 individuals, or 0.5% of the population. And the changes are expected to shave around $2 billion off the $51 billion annual cost of superannuation concessions.

Predictably, shadow treasurer Angus Taylor has described the changes as another broken election promise, since Labor had ruled out changes to the super tax regime during the 2022 election.

Meanwhile, Aware Super CEO Deanne Stewart and HESTA CEO Debby Blakey have urged the government to use some this $2 billion ‘windfall’ to boost the retirement savings of women and people on low incomes.

Blakey argues the government should act now to deliver a fairer and more equitable super system, noting the gender super gap means that on average women retire with around a third less super than their male counterparts.

My view is that Labor’s changes are positive, but do not go nearly far enough.

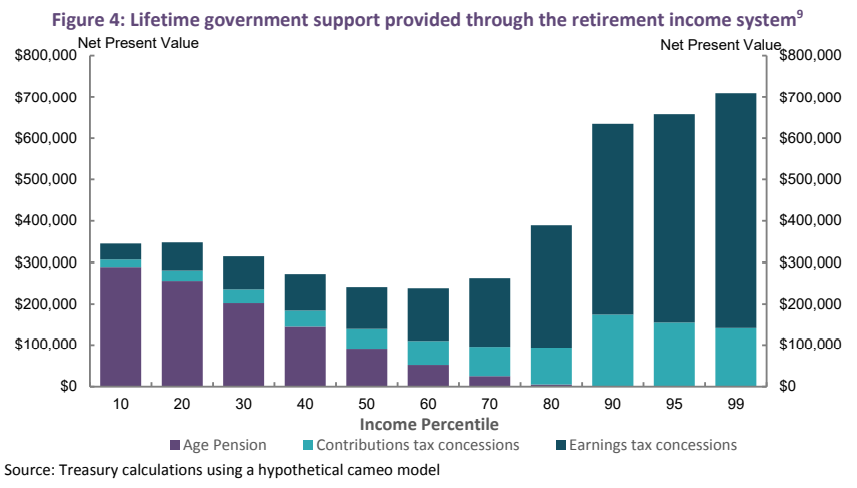

While they will slightly improve the equity and sustainability of the superannuation system, the lifetime taxpayer support provided through Australia’s retirement system will still be heavily skewed towards higher income earners:

And because the size of one’s superannuation nest egg will continue to be a function of how long one works and how much they earn, women will continue to retire with much smaller superannuation savings.

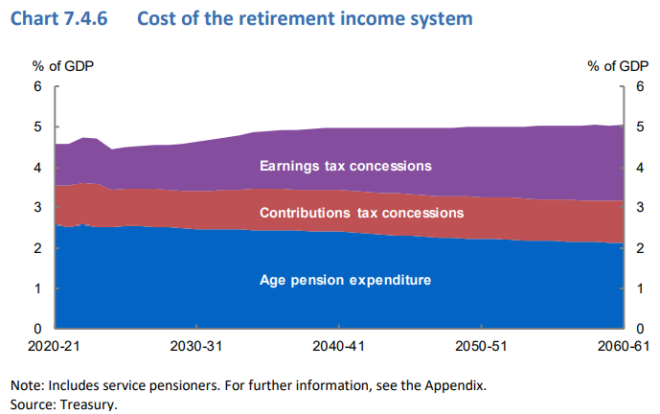

The cost of superannuation concessions to the federal budget will remain huge. and will continue to rival that of the aged pension, irrespective of these modest changes:

Australia’s compulsory superannuation system will, therefore, continue to miss on almost every policy mark:

- It will remain poorly targeted and miss those in genuine need.

- It will continue to cost the federal budget far more than it saves in aged pension costs.

- It will continue to reduce workers’ take-home pay.

- And it will continue to entrench inequality by encouraging tax avoidance and wealth accumulation by the rich and their heirs.

Basically, the superannuation system will continue to take the disparities in working-life incomes and magnify them in retirement, enshrining inequality.

Rather than following Aware Super’s and HESTA’s proposal of using the $2 billion of super concession savings to prop-up the balances of low-income earners and women, it makes more sense to unwind superannuation concessions altogether and to plough the many billions in budget savings into a more generous universal aged pension.

The aged pension suffers none of superannuation’s flaws and should be considered Australia’s genuine retirement pillar.

The aged pension is universally available for those most in need. It is not based upon how much one works or earns prior to retirement. And the pension is not subject to market risk.

Such bold reform would sadly never happen because the superannuation industry has grown too large and powerful and would destroy any government that tried to rein it in.

So instead, the Labor Party has doubled down on the flawed and broken system by raising the superannuation guarantee to 12%, against the advice of the Henry Tax Review and the Retirement Income Review.

In turn, Labor has explicitly chosen to increase superannuation’s cost to the federal budget.

The upshot is that other taxes will need to be higher than necessary, or the federal budget will need to make spending cuts elsewhere to make room for the growing cost of superannuation concessions.