The Association of Superannuation Funds of Australia (ASFA) has urged the federal government to implement measures aimed at reducing the gender retirement savings gap.

ASFA has proposed the introduction of super entitlements for parental leave pay and a $5,000 “super baby bonus” for new parents.

“As we celebrate International Women’s Day, ASFA is calling for long-overdue action to protect the retirement outcomes of women who take time out of the workforce”.

“There is strong support among Australians for policy action”, ASFA senior policy adviser Helena Gibson said.

Women would keep “falling through the cracks” of the superannuation system, she said, as long as these “clear, persisting gaps remained”.

Teal MP Zoe Daniel has also advocated paying super on parental leave, describing it as a “significant step forward for women’s equality”.

ASFA is clearly talking its book with this proposal as it would see taxpayers pushing more money into the superannuation system, beefing up finds under management and investment fees.

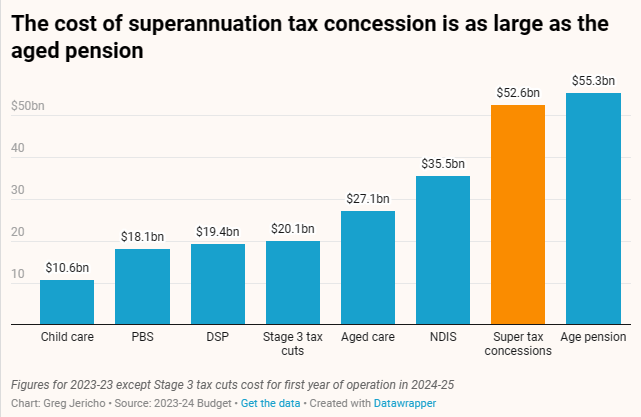

Superannuation concessions already cost taxpayers an extraordinary amount, and ASFA’s proposal would see that cost increase further.

Super concessions cost almost as much as the aged pension.

Let’s get real here. The reason why women accumulate less superannuation savings than men is because of the inequitable way that concessions are distributed, which disadvantages low paid workers irrespective of gender.

Most superannuation contributions/earnings are taxed at a flat rate of 15%. Accordingly, those on low incomes receive minimal concessions, whereas those on higher incomes receive the biggest tax concessions.

And since women generally earn less than men over their working lives – because they tend to work in lower paid professions (e.g. nursing and teaching), work part-time, or take time out of the workforce to raise children – women accumulate lower superannuation balances.

The logical solution to improve equity is to reform the superannuation system to make concessions equitable by targeting them at those who need it most, specifically lower and middle income earners.

The system should be made progressive overall so that lower income earners – be they male or female – receive a better deal.

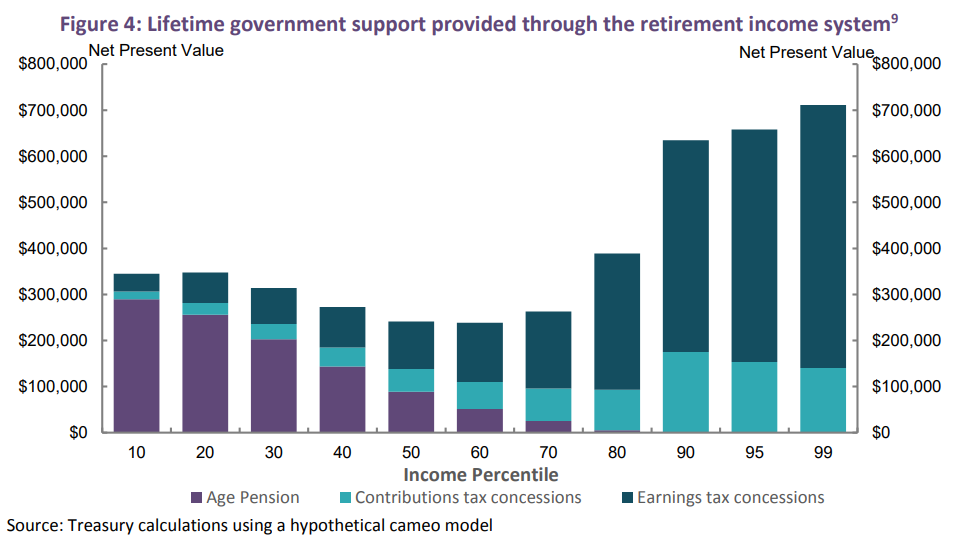

The federal budget would also benefit from a more equitable distribution of concessions given superannuation is currently being abused as a tax avoidance scheme by the wealthy (mostly men) who would never have relied on the age pension anyway, as highlighted clearly in the next chart:

Superannuation concessions are skewed to high income earners.

According to the Australian Treasury’s own modelling, the top 1% of income earners will receive more than $700,000 in super concessions over their working lives, dwarfing the $50,000 received by the bottom 10% of income earners.

Indeed, the welfare of women (and lower income earners more generally) would be greatly improved if superannuation concessions were abolished entirely and the tens-of-billions in budget savings were instead directed into boosting and broadening the age pension, which is available to everyone regardless of gender and is far more equitable and efficient.

Sadly, such bold reform would never happen because the superannuation industry has grown so large and powerful that it would kill any government that dared rein it in.

So instead, we get policy gimmicks like the one proposed above by ASFA that are clearly designed to feather fund managers’ nests by pouring more taxpayer dollars into the system.