Almost one-in-four retirees have no intention of using their superannuation nest eggs to pay for their retirements, according to a recent survey of more than 3,000 pensioners conducted by National Seniors and annuity provider Challenger.

The Australian Treasury’s Retirement Income Review also noted that superannuants have been unwilling to withdraw money from their savings and have instead relied entirely on the income from their investments to pay for their retirement.

As a result, Australia’s superannuation system has been transformed into a mechanism for wealth transfer and accumulation that has expanded inequality.

“Most people die with the majority of wealth they had when they retired”, the Review noted. “If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”.

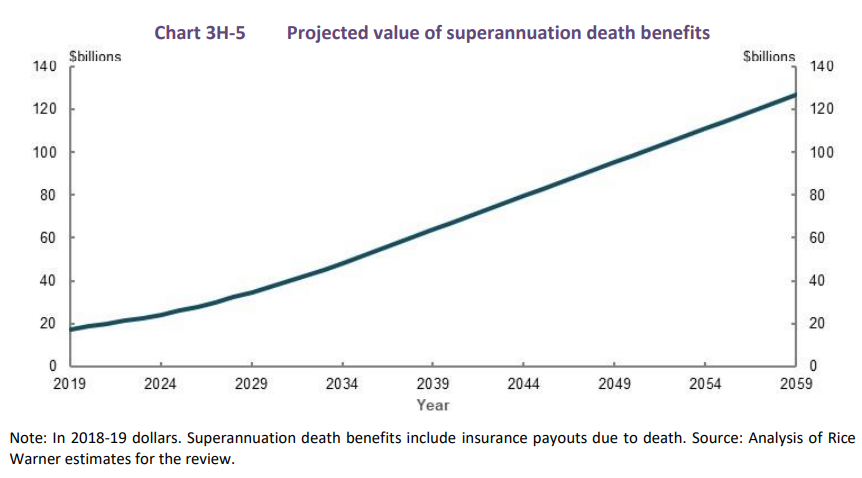

“Superannuation is intended to fund living standards of retirees, not to accumulate wealth to pass to future generations”, the Review argued before showing that “superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059”:

In a new policy report, the Financial Services Council (FSC) has called for changes in policy to prevent retirees from hoarding their super and to encourage them to spend their nest eggs. This includes offering more enticing retirement income options.

It wants easier access to financial advice, the elimination of barriers to the introduction of better retirement solutions, and potentially stronger means testing of the aged pension.

The FSC argues that retirees in Australia are currently drawing down 17% less income in retirement from their super “than what is optimal” and that a more efficient system could boost total benefits paid out to Australian retirees by 10% a year — or $397 billion by 2050.

“A retirement system that is designed around the needs of retirees, providing them the products and advice they need at retirement, and encouraging them to enjoy their savings in retirement, will enhance the long-term sustainability of the superannuation system and take pressure off future tax settings”, FSC CEO Blake Briggs said.

“Realising the superannuation system’s potential to maximise living standards in retirement and higher retiree spending would take the load off a Federal Budget with a 2% structural deficit partly due to increasing health and aged care pressures that could be better met from individual savings”.

I agree with the FSC’s position.

Super nest eggs were never meant to be hoarded so they can be passed to one’s heirs after death. They are intended to be drawn down in retirement.

Consider a newly retired person with $500,000 in superannuation funds who receives a conservative return of 5% per year (comprising both interest and dividends).

This retiree would earn $25,000 year (or 5% of $500,000) if they were to fund their retirement only through investment returns. But if the principal is also reduced, $38,200 would be made available over a 20-year period to pay for their retirement.

Put simply, retirees should be forced to draw down their superannuation. This is far more egalitarian and affordable than continuously lifting the superannuation guarantee at the cost of billions to the federal budget.