DXY is still firm:

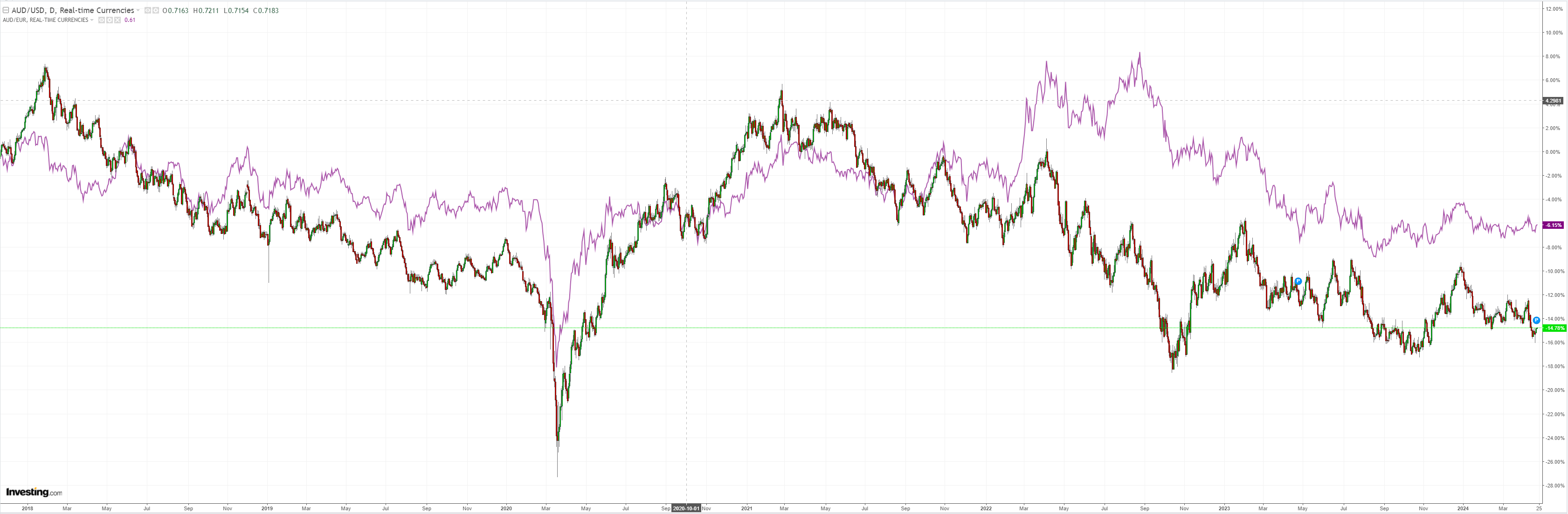

AUD bounced off the hammer candle:

North Asia is caput:

Brent is trying to hold. Gold puked:

Other commods paused:

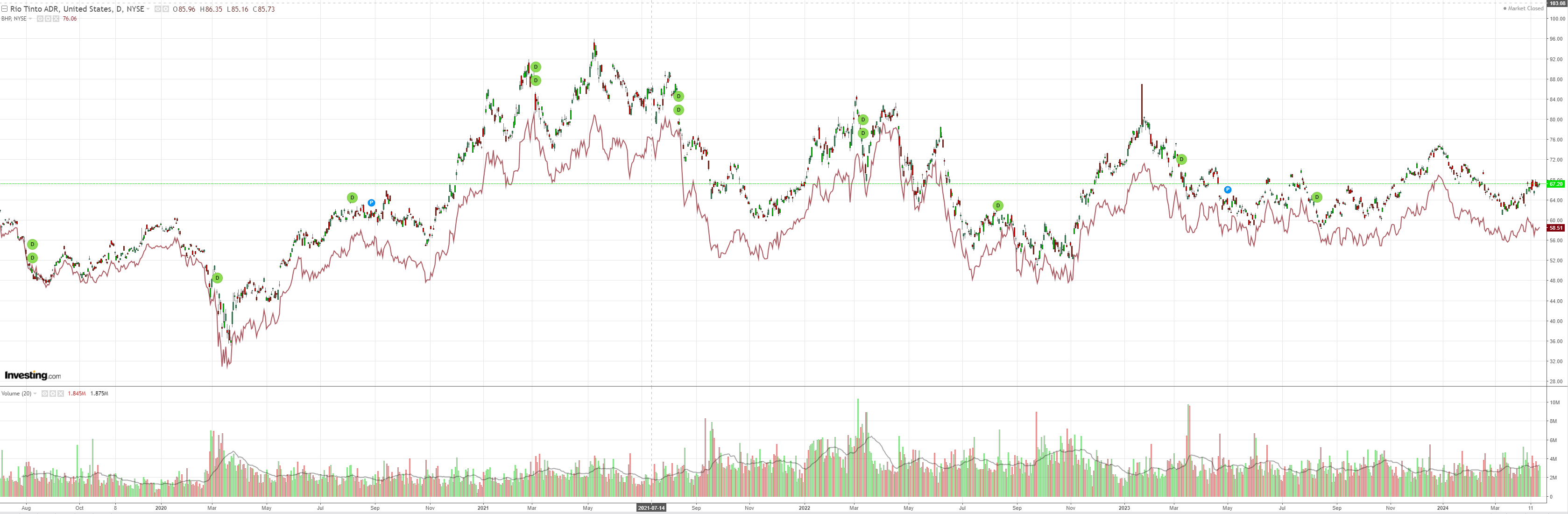

Miners meh:

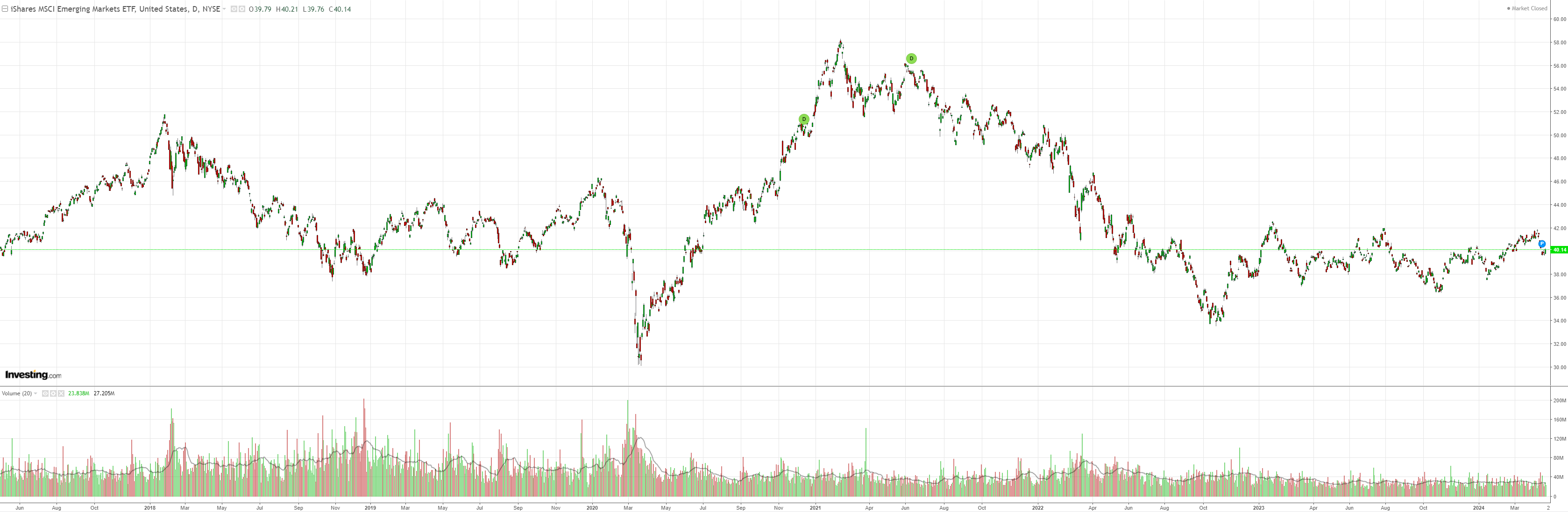

EM yawn:

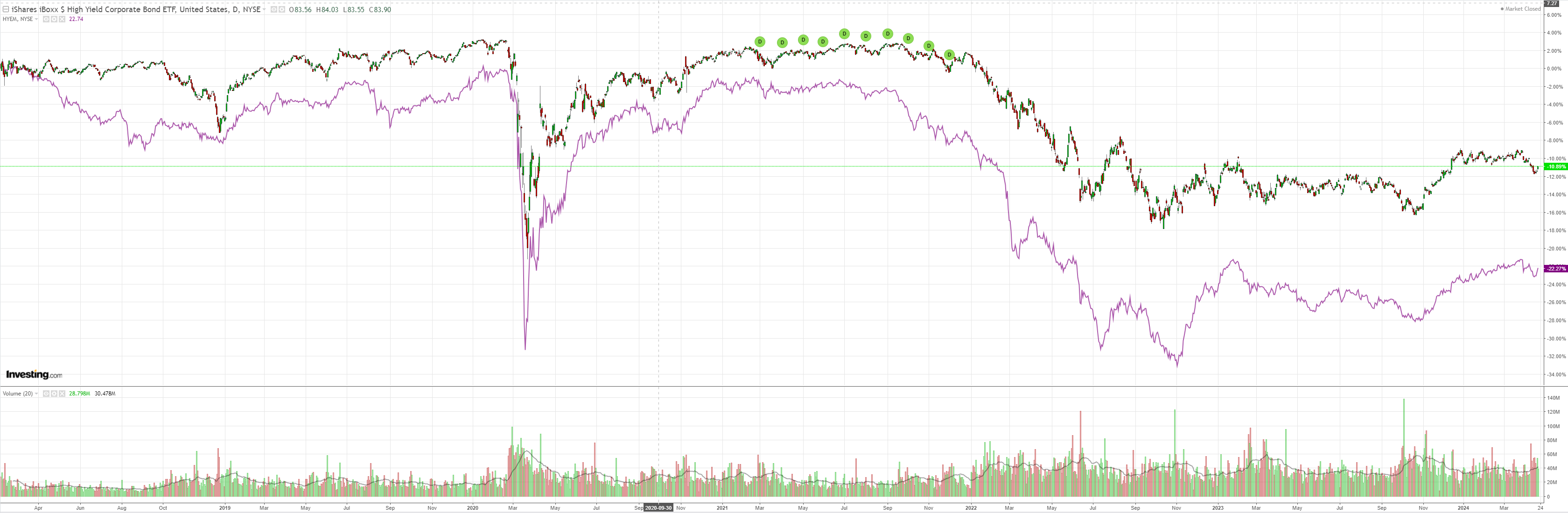

Junk is back. Good for equities:

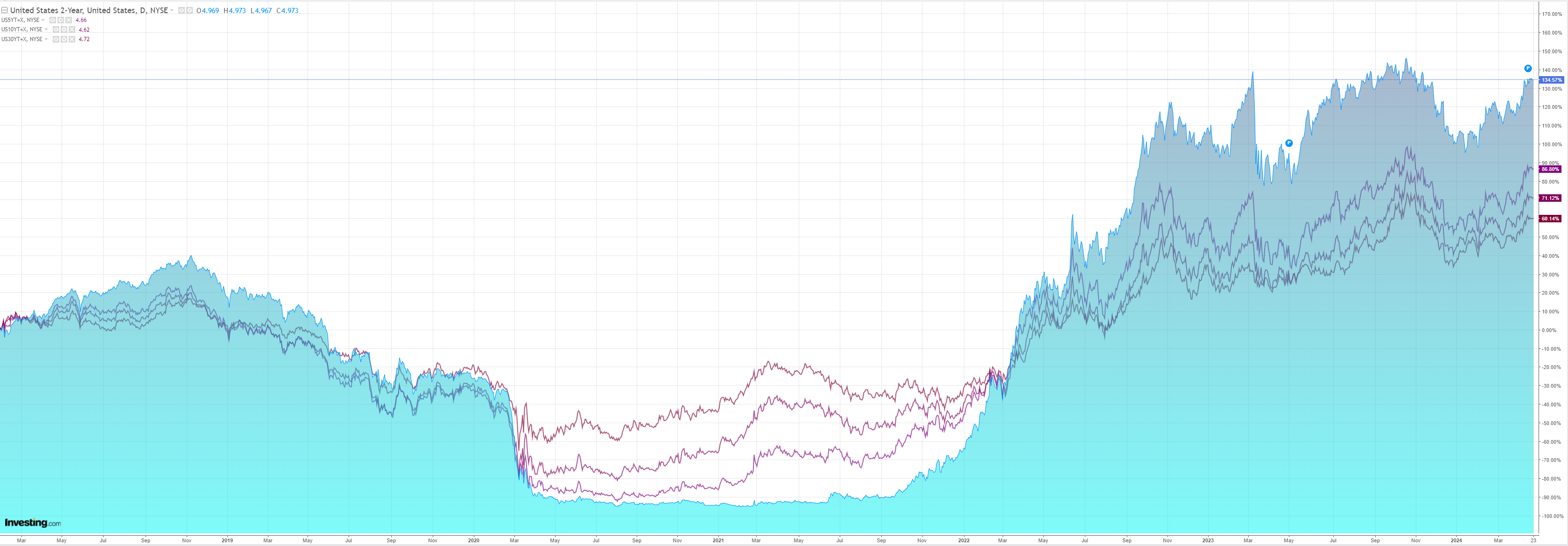

Yields soothed:

Stocks bounced:

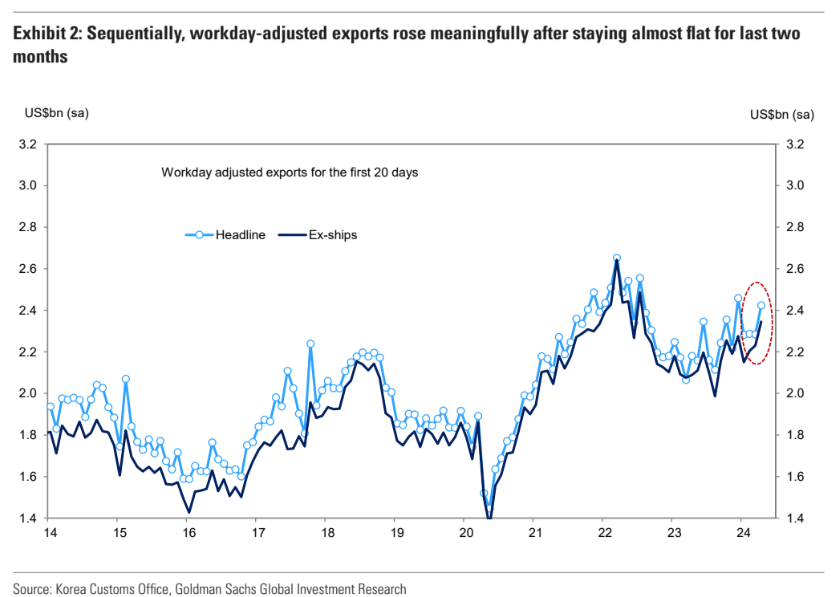

Korean March exports are showing a steady global industry lift is underway. Goldman:

Total 20-day exports during the 20 calendar days accelerated to 5.5% mom as from 3.7% the prior month. Exports gained broadly across major products except for ships which dropped 13.7%. In particular, auto exports gained sharply by 20.8% and alone accounted for a third of headline gains. Among non-tech products, machinery exports also sustained a robust gain of 8.2%, while exports of petroleum, steel and auto parts gained only modestly. Semiconductor exports slowed to 1.7% after rising nearly 4% in prior two months, while computer exports gained sharply for the second month, by 24.0%.

It has broadened out from chips now, so there will be some support for commodity currencies.

However, this is not “no landing.” We are steadily recovering from a soft landing, with headwinds mounting already in oil, Chinese property, and the Fed.

I expect China to remain weak and the other two to ease in due course as a modest disinflationary global recovery, led by the US, takes hold.

In this scenario, AUD is in little danger of breaking out of its mid-60s range in the near future.

Inflation will have to rev commodities for that, and even then, the incipient iron ore crash is a massive pothole.