In February 2009 after I came back from holidays in Yamba I sat down with a mentor and mapped out how we thought the crisis would manifest over the coming years. I had a massive advantage over many investors and traders in that in my research I had stumbled upon a book written in 1996 by a Historian named David Hackett-Fischer. Professor Hackett-Fischer had written a history of inflation going back to the 1200’s, but in doing so he had mapped the economic history of the globe during that period. When reading that book, sitting on the couch after surfing Angourie, I was struck not that this book, “The Great Wave: Price Revolutions and the Rhythm of History” was about inflation but rather that it was a rolling history of the crises of the western world over the past 800 years and that this crisis we were in was probably going to be long lasting and that it would have several phases.

So back in my old office on the second floor Steve and I mapped out how we thought things would go.

- First stage was what we had already seen, Government rescue;

- Second stage was bounce After the government rescue;

- Third stage was recognition that the bounce wouldn’t be followed up and that Government finances were now in trouble;

- Fourth stage was recognition of this fact and the imploding of belief that Governments of the world could actually save the world and back down we would go.

- Fifth stage was then the cleanup, which could take years.

Our view was that the world would lack aggregate demand and probably go through a period of deflation and that ultimately, some way down the road between 5 and 15 years, inflation would come back with a vengance.

Implicit in this discussion was that the United States would not escape unscathed from the carnage.

In truth we were wrong, we expected all that has happened since April this year to happen in the last quarter of 2010 but we did expect it to happen, nonetheless.

Why have I spent so much time saying all of this when I guess you want to know what we think will happen as a result of the US credit rating downgrade? Because this was always going to happen, so it is important to have a historical perspective and as David Hackett-Fischer told me, not to panic, because we will get through this. In the mean time markets are likely to be in a funk for a while and capital protection is paramount, the world economy has to heal. That is the process.

So what does it mean for currencies?

First thing we need to do is evaluate the palybook that traders and investors have been using over the past 25 years and see if it still holds.

Play 1 – Government’s run currency markets:

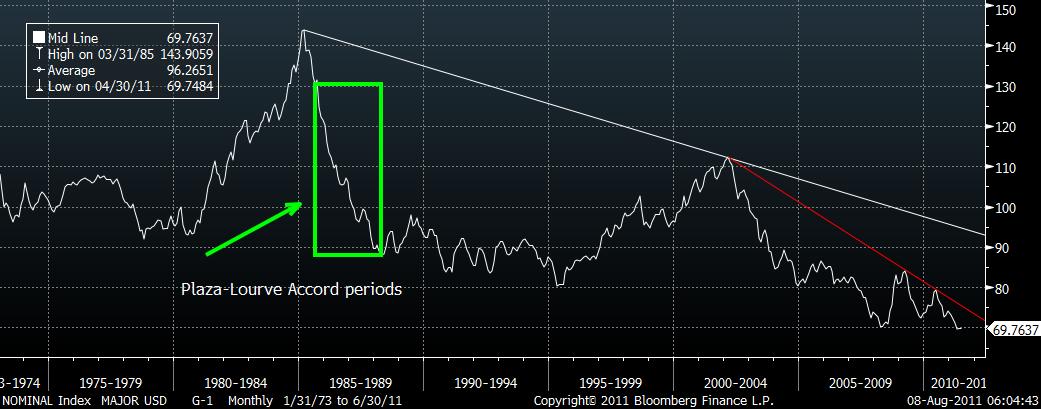

1985 Plaza Accord – G7 Agreement to weaken the USD

An agreement was reached to weaken the USD against the JPY and DEM (German Deutschemark) after it was deemed that the USD was too strong. The combined selling of the big central banks and Treasuries had the desired impact of improving the competitiveness of the US economy helping both the current account deficit and the recovery from recession

1987 The Lourve Accord – G7 goes back the other way

The Plaza Accord was a little too successful and the USD drop over 50% versus the JPY and DEM. In Paris in February 1987 the big economies of the world moved together to halt the action of the Plaza Accord by moving into the market.

As you can see in the chart above the action stopped the speed of the decline but it did not halt the decline as the USD continued to weaken for years.

Play 2: The emergence of currency as an asset class 1988 onwards

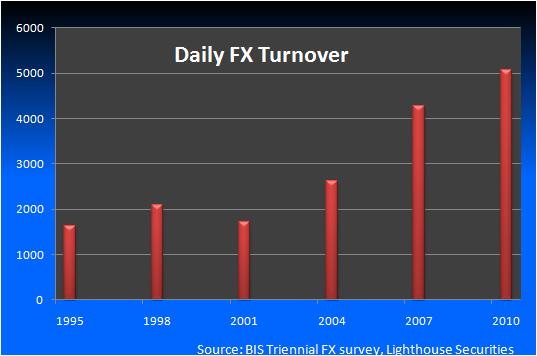

In 1988 John Taylor started what is now the worlds biggest currency hedge fund – FX Concepts. In 1991 Pareto Partners began and revolutionised the “currency overlay” space. These companies were, and still are, at the forefront of currency management and trading as an impact on FX rates.

In the period since these companies, and others, came to the fore FX turnover has sky-rocketted from under $500 billion a day in 1989 at the first BIS triennieal survey to $5.056 trillion USD in April 2010.

FX rates increasingly went from representing economic fundamentals such as current account balances to trading as an asset class and thus off the back of “investment” fundamentals such as opportunity for capital gain.

1995 – USD reiterates a strong dollar policy

In many ways I cut my tetth as a portfolio manager in the bond market rout of 1994. But as a result of this sell off the USD came under pressure and was at risk of a Plaza Accord style rout. Lloyd Bentsen, the US Secretary of the Treasury at the time, coined the phrase that “a strong dollar was in the interests of the United States”. Up until recently this was the lowest level the USD/JPY had fallen to.

1997-98 Asian Crisis and Russian Default liberates emerging currencies

The Asian crisis was fractious and volatile at the time but it had the impact of forcing a number of Asian currencies off their fixed, basket or crawling pegs and exposed them to market forces. These currencies now trade in large volumes but are also suffering under the weight of USD weakness, more on that below.

1999 – Introduction of the EUR, currencies disappear, but the market deepens

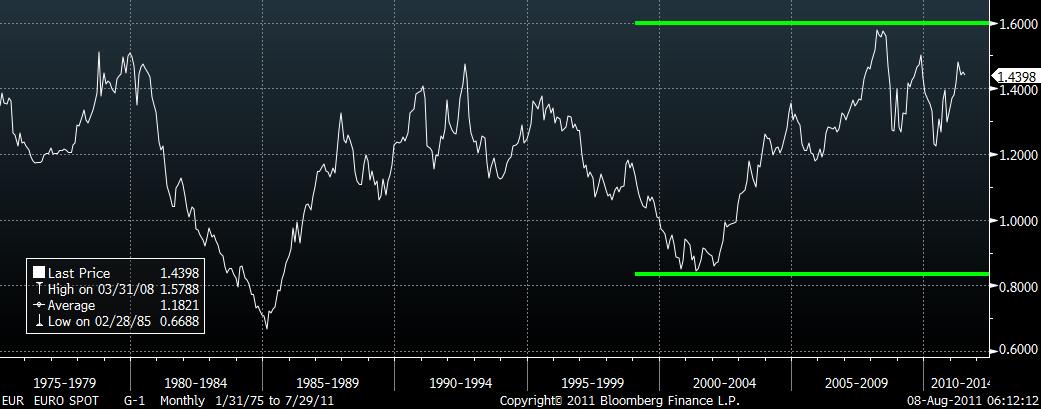

I was in the Westpac dealing room in Sydney as the currency strategist at 5am on the first trading day of 1999 when the EUR was launched to much fan fair and expectations on the future of the single currency. It rapidly climbed after the inital launch to 1.19 before crashing all the way back to 75 necessitating intervention to support it in 2001.

The EUR replaced the currencies of the sovereign nations who joined it, thus eliminating currency volatility for these nations, but not currency volatility per se as you can see in the range since the introduction, something like 83 big figures of more than 100% from the lows. As we have all learned since 2007 taking away of the flexibility of the exchange rate to adjust to shocks also takes away its ability to insulate individual economies where necessary.

The introduction of the EUR had, in my mind at least, the unintended consequence by eliminating many of the tradable European currencies and crosses but equally of deepening the trade in what was left. The deepening and increased liquidity then aided in increasing speculation,as the chart above of turnover shows.

Play 3: 2001 to 2008 (pre- Lehman and when many denied this was a real crisis)

The Greenspan put was alive and well after the NASDAQ crash and it was, unfortunately, reinfoerced after September 11 2011. The low rates and seemingly benign economic conditions of the so-called “great moderation” saw an increase in what Minsky had called many years before “money manager capitalism”.

Investment metrics and currencies as a full blown asset class replaced economic fundamentals. Market forces, fear, panic and loathing were as important as current account deficits and economic fundamentals. Turnover increased materially and intervention by governments and central banks while still maintaining an impact lost its ability to move FX rates in a lasting manner.

But growth currencies were still growth currencies and always traded as a default move away from the bigger currencies of EUR, JPY and USD.

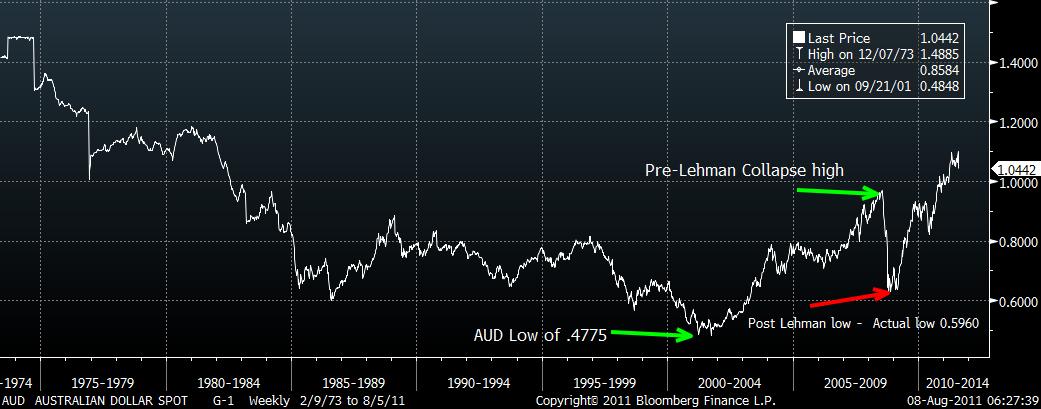

There were broad ranges for currencies during this time. The AUD/USD had a low of .4775 on April 19th 2001 (where was EUR) and a high of .9856 in July 2008.

Play 4: GFC post Lehman September 2008 till QE2 August 2010

In the few days after Lehman Brothers collapsed the AUD actually rallied 6 cents from 0.7802 to around 0.8519 cents before collapsing to 0.5960 in November 2008. Risk went off everywhere and the safe havens of the CHf, JPY and USD benefitted.

But as risk assets came back so did the risk currencies and the rally in risk saw the USD weaken up until the Summer sell-off of 2010 before QE2 began.

Play 5: August 2010 – May 2011

QE 2 starts to debase the USD, regardless of Treasury Secretary Geithner’s hollow re-affirmation of the strong dollar policy. Growth AND safe haven currencies appreciated together. Gold too lifted as a “hard” currency and EUR benefited because of USD weakness. The CNY gradually began appreciating but not enough to take the weight of global adjustment.

Play 6: May 2011 – August 2011

Safe Haven currencies and gold appreciated, growth currencies stalled in sideways trading. Despite this and overly late to the station, talk emerged that growth currencies like the AUD and NZD were the new safe havens.

So what’s the next play in the book? Is it the The Hail Mary, no one knows what to do and runs to their home currencies or, as some assert, do they simply switch to a new version of safe haven and exit the USD now that the United States has lost its AAA rating.

The first thing to do is recognise that currency markets have often had to deal with phase transitions over many years so this is nothing new. Currencies have both evolved and grown as markets and any notion that there is a stasis in FX is tenuous at best. So this is not a shock for currency traders – many bets will have already been laid. S&P’s action is simply recognition of where the FX market had already headed.

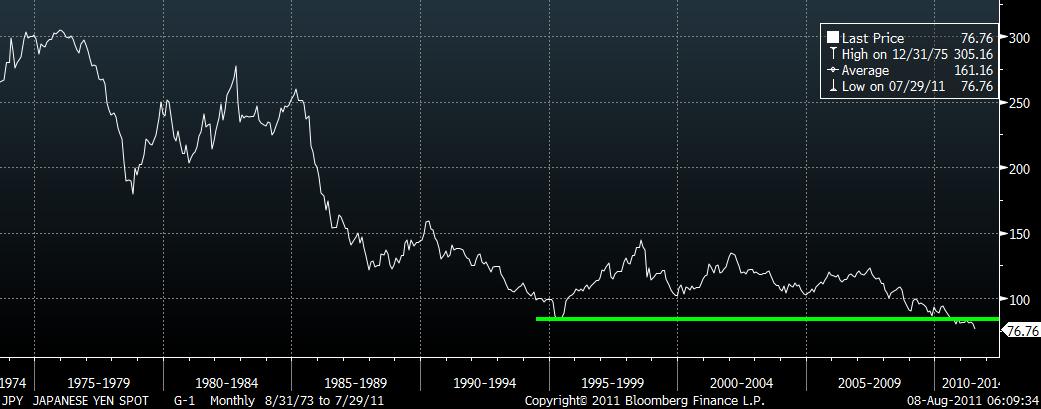

For the USD I would argue that the AAA rating matters less than investors perceptions about what is going on in countries and asset markets relative to each other. Remember that Japan lost its AAA rating from S&P in 2001 and has been in recession for 2 decades yet its currency is super strong against the USD and very strong versus the EUR. Sure you can argue that the composition of Japanese debt is different, and that it runs a current account surplus but investors are not only driven by what S&P, Moody’s or Fitch say.

For FX markets the key is not what the ratings agencies have done, the key is that for the second time when faced with a crisis partisan political consideration got in the way of a decent resolution. In the post Lehman world the failure to pass TARP the first time froze markets and saw risk go off, the USD was a beneficiary. This time I would argue that the US political class has dealt itself a blow from which it will be hard to recover and shined a light on the fact that Uncle Sam is on an unsustainable debt binge path. Crucially however, as S&P pointed out US politicians have not the inclination nor the wit to deal with the issues confronting them.

Uncle Sam is unlikely to default anytime soon but this is not the behaviour becoming of the world’s reserve asset leaders. So, we have another phase change as FX investors probably don’t see the USD as the gilt edged, risk free investment that it once was.

But what does it all mean for us in 2011?

If 2008 is any guide don’t be surprised if the “growth” currencies actually appreciate in the coming days, perhaps weeks. Of course they should if only for the fact that the USD is the other side of the bi-lateral cross. As I noted above the AUD rose after Lehman before it crashed – it could do the same here. But this is not like 2008 nor 2009 – it is potentially much worse.

Politicians the world over are struggling to grapple with the aftermath of the collapse of Lehman Bros., the necessary bank rescues, moribund economies, high sovereign debt positions and no appetite nor fiscal space to deal with it. The future of the global economy is not looking too bright at present.

Westpac’s Head of Currency Strategy, Rob Rennie said the following in a note to clients over the weekend,

We have maintained a risk averse view on financial markets and argued that traditional risk currencies like the AUD and NZD were becoming increasingly vulnerable. Traders have been lulled into a false sense of security, buoyed by Asian central bank demand. Some have started to argue that these currencies were becoming ‘safe havens’. This view is myopic at best, dangerous at worst. S&P’s moves can only add to the rising sense of risk aversion. The US economy has slowed too, and arguably through its “stall point”; European growth is being put increasingly at risk by the deepening sovereign crisis. Asia is also weakening. None of this can be good news for pro-cyclical currencies like the AUD and NZD. If the US$ does sell off Monday morning in Asia, lifting all currencies including the A$ and NZ$, we would expect such gains to be quickly reversed.

I agree. With the proviso that neither Moody’s nor Fitch follow S&P. In such an event, investors will be in unchartered territory as they lose their risk free anchor. What do they price off now, which country is the new benchmark. Which currency is big enough to act as the global reserve?

EUR is big enough but hardly in the shape to be a reserve currency, Swissy and gold are acting as reserve currencies but aren’t big enough to cope with demand so their value just shoots higher – this is an impediment to reserve status. China is the obvious next choice but is not ready, willing or able to satisfy this role as its economy and markets are still developing. It’s day will come however.

So I’m left with the feeling that this action by S&P is just another factor amongst the myriad factors that impact FX markets. Sure, if countries such as China act on their rhetoric over the weekend about the unsustainability of the US’s borrowing binge the USD may collapse.

But for me it is the global economic outlook which is far more important now than S&P’s rating. As Steve and I mapped out back in 2009 we are probably in stage 4 of the crisis – the recognition that Governments can’t fix things.

Ultimately don’t be surprised if the politicians try to manipulate currency markets again to try to reinforce the status quo. Unless they re-regulate they will have little sustainable impact. Merkel and Sarkozy are certainly of this bent, Europeans seem to think they can negotiate their way through everything, even while achieveing nothing as has been in evidence for the past year or more. The US is less inclined to follow this path and the Tea Party would never vote for something like re-regulation.

Over the medium to longer term we are in for a volatile time, to say we may see currency chaos is no understatement, but this is nothing new. Long term structural changes are happening in the values of the globes two biggest currencies – the AUD will be caught in the backwash.