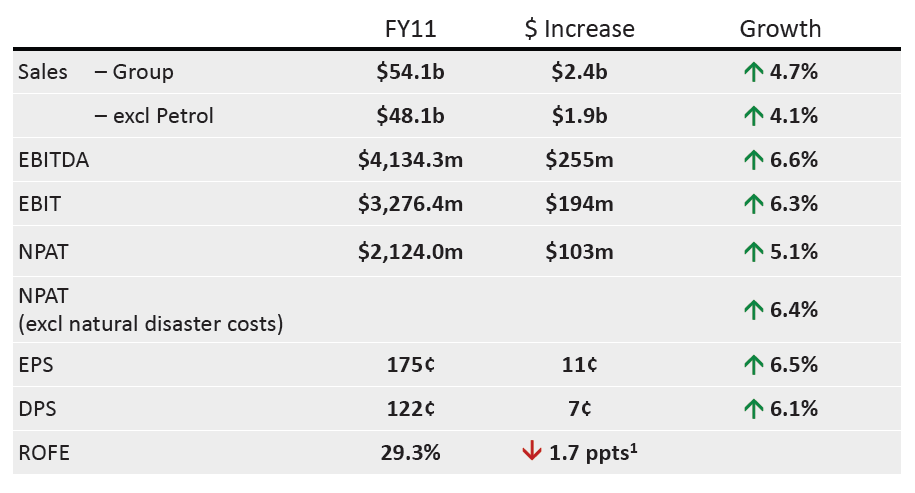

![]() Woolworths released their FY11 results last Thursday. The analysts presentation headlined with a 5.1% NPAT increase, which was at the lower end of the 5-8% range given in the last earnings guidance, which was in turn below the 8-10% growth forecast at the start of the year. As such, the share market reaction was harsh and WOW’s price fell by $2 over Thursday and Friday. Personally I think 5.1% growth for the dominant player in our supermarket duopoly is pretty good given the cautious consumer behaviour we’ve seen.

Woolworths released their FY11 results last Thursday. The analysts presentation headlined with a 5.1% NPAT increase, which was at the lower end of the 5-8% range given in the last earnings guidance, which was in turn below the 8-10% growth forecast at the start of the year. As such, the share market reaction was harsh and WOW’s price fell by $2 over Thursday and Friday. Personally I think 5.1% growth for the dominant player in our supermarket duopoly is pretty good given the cautious consumer behaviour we’ve seen.

The analyst highlights (taken from the presentation) are as follows:

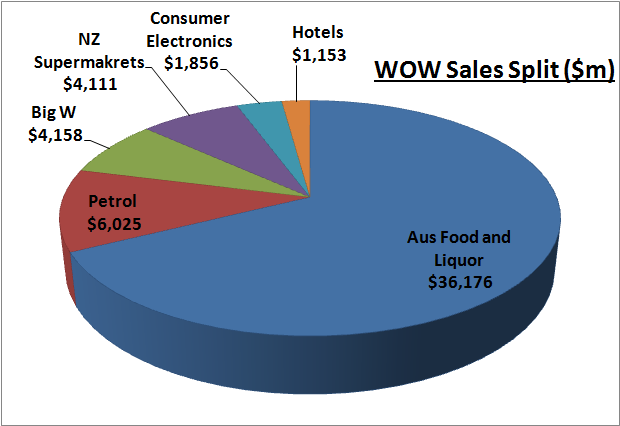

Segment Split up

The sales split by segment for FY11 is shown below.

Let’s take a look at the results by segment.

Australian Food and Liquor

- Sales growth of 4.3%

- EBIT growth of 7.5%

- EBIT margin of 7.4%, up 0.2% from 2010

- Total price inflation of 1.1% whilst food deflation of 3.6% was experienced in the second half of the year due to discounting measures

New Zealand Supermarkets

- Sales increased by 3.5% in NZD, but decreased 0.5% when converted to AUD

- EBIT was constant in NZD (increased by 1.1% in AUD)

- EBIT margin in AUD came in at 4.7%, an increase of 0.1% on 2010

- Total food price inflation of 1.4%, I presume in NZD

Petrol

- Sales increased 9.9%

- EBIT experienced an impressive 18% increase

- EBIT margin increased to 2.0% – up 0.2% on 2010

Big W

- Sales decreased slightly by 0.5%

- However, EBIT decreased 11.5% as a result of price deflation due to discounting and the strong AUD

- EBIT margin decreased to 4.3%, a drop of 0.5% on 2010

- Price deflation averaged 6% for the year

- WOW claims trading improved in the second half, with sales growth of 2% and EBIT growth of 5.7%

Consumer Electronics

- Sales increased 4.2%

- However, EBIT dropped 15.6%

- EBIT margin dropped from 1.8% in FY10 to 1.5% in FY11

- Cost of doing business actually improved during FY11, so the main culprits for the poor performance appear to be (once again) price deflation and the cautious consumer

Hotels

- Sales increased 4.4%

- EBIT increased 4.0%

- EBIT margin stayed pretty much the same at 16%

- WOW now owns 282 hotels and clubs

The Masters Venture

- None operating yet

- 15 – 20 planned for FY12

- Planned for a total of 120 stores within 5 years

- First to open in Melbourne

Comparison with Coles

Back in July I wrote a piece on the Wesfarmers sales results, so let’s do a little side-by-side sales comparison:

|

Coles |

Woolworths | |

| Total Sales: |

+ 6.3%, |

+ 4.1% |

| Food and liquor: |

+ 6.3%, |

+4.3% |

| Petrol/Convenience: |

+ 8.5% |

+9.9% |

| Big W v Kmart/Target: |

down 0.5% |

down 0.5% |

From the full-year Wesfarmers results, I was able to pull the following numbers for an EBIT comparison:

|

Coles |

Woolworths | |

| Food, Petrol, Liquor |

EBIT up 21.1%, |

+7.4% |

|

EBIT margin 4% |

6.4% | |

| Big W v Kmart/Target: |

EBIT down 16.1%, |

-11.5% |

|

EBIT margin up 6.1% |

4.3% |

It is easy to see why analysts say Coles has the momentum, with stronger sales growth in the dominant food, petrol and liquor divisions. However, EBIT margin in the same divisions is lower than WOW. This may be a result of Wesfarmers higher debt load, although at the end of FY11 WOW had increased their debt to similar levels (see below), so this gap may close come FY12.

Increased Borrowings

Woolworths increased its borrowings substantially in FY11, from $1.1b to $4.8b (a 237% jump). This puts borrowings per share at $3.98 vs FY11 earnings of $1.53 per share, which is ok but not as good as FY10 where earnings were greater than borrowings. However, debt levels look better when $1.5b in cash and equivalents is subtracted, giving net debt of $3.3b and a net debt to equity ratio of 45%.

The increased debt was used to fund a $700m share buyback program as well as “investment in property”, which I assume relates to the Masters hardware venture. Borrowing to repurchase shares is fine so long as the return on the buyback is better than your interest rate and debt levels aren’t too high. Given WOW’s return on equity (ROE) is has averaged 28% over the last 5 years, the buyback should prove to be a positive for shareholders.

As for the Masters venture, only time will tell.

Summary

All in all, I think it’s a solid result for WOW in a deflationary environment. Woolworths has kept a lid on the cost of business, maintained positive margins (except for the NZ divisions due to forex movements) and grown sales.

Borrowings have increased a considerable amount and we’d like to see them decrease relative to earnings over the coming years. However, WOW is only moderately geared and should the Masters venture prove profitable, the increased debt levels will have been justified.

Looking forward, I’d expect similar results in the coming years for WOW (assuming the Masters hardware venture performs in line with other segments). Sales growth will most likely track population or income growth in Australia – maybe less if its arch-rival Coles manages to steal some market share. The days of double-digit earnings growth are over as Coles gets its act together and the Australian consumer continues to hibernate.

Valuation

Assuming a normalised ROE of 36%, reinvestment of 20%, an equity per share level of $6.22 and a required return of 15%, Empire values WOW around $27.

This is 10% drop from our $30 valuation a few months back (see here), which reflects our adjusted views on future earnings multiples and earnings growth. To be frank, we’ve changed our optimism levels as Australian retail stays in the doldrums and the US and EU continue to struggle with political ineptitude.

Nonetheless, we still believe Woolworths is a Wonderful company and one of the best investments (at the right price) on the ASX. We think it’s a bargain below $24.50.

Disclosure: The author is a Director of a private investment company (Empire Investing Pty Ltd), which has currently has an interest in the businesses mentioned in this article. The article is not to be taken as investment advice and the views expressed are opinions only. Readers should seek advice from someone who claims to be qualified before considering allocating capital in any investment.