ABARES’s recently released report into Foreign Investment in Australian Agriculture caused quite a political and media stir. There is a good reason for this. The report adds a hatful of data and analysis to an important macroeconomic debate.

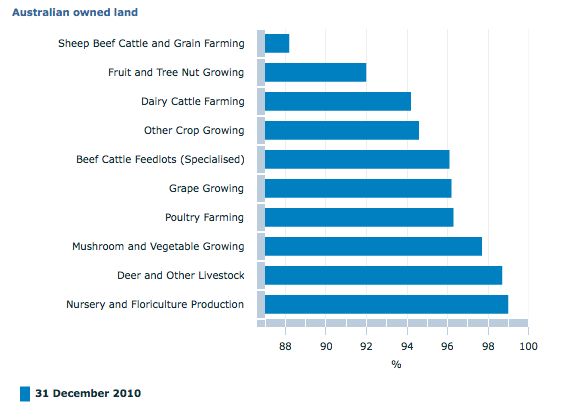

There wasn’t a lot of new news in the report, given that the ABS began its survey of foreign ownership of agricultural land, water and businesses in 2010 (key results plotted below). The media latched on to the fact that 11% of agricultural land, by area, is fully or partly foreign owned; yet by value this figure is much lower. In total, foreign entities own about $1.6trillion of Australian assets (through direct and indirect investment). All of this was new in 2010.

More importantly than breaking news, ABARE specifically outlines recent large land deals, analyses multiple data sources, in the context of an overview of the regulation surrounding foreign ownership. The real value of this report is how it breaks down the factors at play in each agricultural market, and the business strategies being implemented by foreign participants.

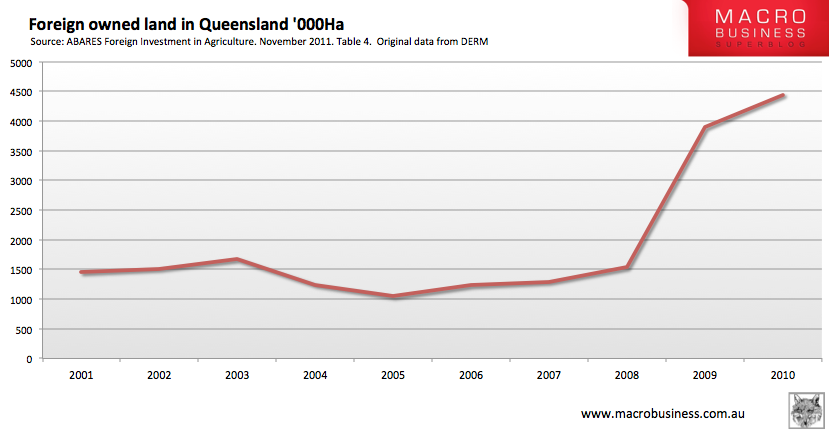

For example, from the QLD land titles registry we get this information, and the data for the following chart, on foreign land ownership –

The large increase in foreign holdings in 2008–09 was dominated by a single purchase, that of 90 per cent of the Consolidated Pastoral Company by the British private equity company Terra Firma Capital, involving approximately 2.6 million hectares in Queensland. This company purchased a further 600 000 hectares in 2009–10.

In 2010, there were 43 purchases of farmland by foreigners in Queensland. Of the total value of farmland that changed hands, 14 per cent or $203 million was accounted for by foreign purchasers. The average value of farms sold in Queensland in 2010 was $1.18 million, but the value of farms bought by foreigners averaged $6.28 million.

In 2010, mining companies constituted a significant proportion (around 60 per cent by value) of the foreign purchasers of farmland in Queensland

The commentariat have heavily focused of the concept of ‘food security’ which is currently of relatively minor significance to Australia and is not destroyed by a change in ownership (but rather by the destruction of soil and irreversible changes of land use), while ignoring the broad macroeconomic, and dare I say, political-economic, policy decisions. These decisions are cementing Australia’s long-term trade position to one of selling our national asset base (or borrowing from abroad) to fund our current account deficit (CAD).

Put simply, if financial and fiscal regulation allows a persistent CAD, we are going to have to sell assets or take on foreign debt (for the capital account to balance with the current account). While national monetary policy is not analogous to household budgeting, national accounting can be compared somewhat easily. If Australia was a household, we would be spending more than we earn (when we trade with others outside our household), and financing this spending by selling off part of our land and other assets, or borrowing from outside the household. No one would recommend this as a sustainable strategy at a household level, nor would they invest in a business with such unsound financials, but policies that reinforce this position are being maintained at the national level.

If you want to argue that domestic savings are insufficient to match the investment opportunities presented, you need to ask why foreign countries can create savings that outstrip their domestic investment opportunities, and what exactly makes Australia any different. It is a great myth that foreign investment is required to bridge a domestic savings shortfall. The only real limit to investment is the stock of physical and human resources to employ in new endeavours.

I will finish by reiterating the relevant conclusion from a previous analysis of Australia’s financial position, which is the real debate we should be having.

So not only do we usually import more than we export, we sell more domestic assets than we buy foreign assets, and the incomes from the transfer of assets to foreign ownership far outweigh the value of the actual trade of goods and services.

A quick example. The government owned business Telstra was privatised, and 25% of the company is now foreign owned. That purchase by foreigners was a transfer of assets to foreign ownership as part of the capital accounts, and the dividends earned on the foreign owned portion now leave the country as part of the deficit in the primary income balance of the current account. The same applies to foreign purchases of agricultural properties, mining shares, and lending to Australian businesses.

For the past 50 years it seems that Australia has been selling off its bountiful natural assets, and going into debt to the rest of the world. It makes me quite frustrated to even suggest that a fair portion of foreign debt incurred in the past decade was used to pay each other higher prices for existing houses, doing nothing to improve our productivity as a nation.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin