The 41st Australian Conference of Economists was held in Melbourne last week. It provided a unique insight into the industry that should have been seriously shaken up by its failure to foresee the financial crisis, and to provide consistent macro-economic advice in general. Sadly, it was not.

John Quiggin set the challenge to all attendees to make economic research relevant to policy, and to communicate it better to the public. He noted that microeconomics had advanced a great deal in the past 20 years, but that the profession had failed to maintain any policy relevance. For example, Quiggin noted that there is no consistent agreed method for assessing whether private or public provision of a service is likely to be better than the other. He noted that we went from three decades of government provision for no particular reason, to the past three decades of privatisation – with neither trend based on solid economic principles.

I agree whole-heartedly that microeconomics has advanced our understanding of markets, but the really important policy questions are mostly macro-economic, and it is here that economists world-wide have struggled. Quiggin, like most intelligent economists, made this point very strongly and suggested that the path for macro-economics in the future would involve dynamic models – in fact it sounded like Quiggin was explaining Steve Keen’s work (and others), yet no one at the conference seemed to know or care about this type of analysis.

It was a telling insight into the ‘market failure’ of the economics profession.

I can divide my overview into three key areas – productivity, Dutch disease, and vested interests.

Productivity

David Gruen, Executive Director of Treasury’s macroeconomic group, spoke about our productivity challenge. Based on a recent international survey, he argued that Australia’s inferior management ability might be the cause of our productivity slump. I held back from asking the obvious question – ‘Is management performance the same unexplained residual as productivity?”. Because it is, basically. And I figured anyone who was a serious economist would immediately see this as the fundamental basis of the argument.

They didn’t. And the media reported his comments uncritically.

It took Dr Hui Wei, Director of Economic Analysis and Reporting at the ABS, to correct the panel about their incorrect inferences from the multifactor productivity (MFP) measure. Wei is the ABS productivity measurement guru, and a serious critic of the measure. His own analysis makes my previous criticisms look mild. Labour productivity, he explained, is the only measure that contains useful information, and it grows mostly through ‘capital deepening’. By this measure our productivity growth is world leading.

Yet, for the rest of the conference vested interest after vested interest used our declining MFP as the critical reason we should adopt their proposed reforms. Henry Ergas tried to blame government infrastructure provision, especially the NBN, for our productivity performance, calling for more privatisation and less regulation in general. He explained that no official cost benefit analysis was undertaken for the NBN, and that this would be just another ‘waste of money’ that will undermine our productivity. He couldn’t think of any government infrastructure project that was ‘successful’, and his own private cost-benefit analysis showed the project the NBN to be a terrible waste of money.

An audience member suggested that most government infrastructure historically never had such analysis, even the successful projects, and that cost-benefit analysis can give you any answer you want in any case by simply tweaking the assumptions. Ergas replied that knowing what assumptions are required for the project to provide net benefits was critical. He then promoted his own analysis (conducted by his consulting firm immediately before it went into administration), while generating a lot of confused looks when he seemed to argue that coaxial cable and fibre optic cable are as good as each other. Yet his analysis is a feasibility study of private benefits, and ignores all social benefits. Indeed, his submission simply assumes that there are economy-wide productivity losses from the NBN compared to the base case. Can’t argue with that now can we?

Judith Sloan added her two cents, suggesting that labour market reform (read: lower wages) is required to make us more competitive internationally. I can’t help think what sort of wage reductions would be required to offset the 40% appreciation of the currency since the middle of last decade.

Ken Henry was one of the few presenters to demonstrate an exceptional understanding of productivity, noting that as we adjust towards mining, the ‘labour shedding’ in other sectors will automatically generate improvements in that sector’s measured productivity. But he failed to make the final link with Wei’s analysis, especially that continued productivity growth requires capital investment in those sectors, which won’t happen during a mining investment boom.

Dutch Disease

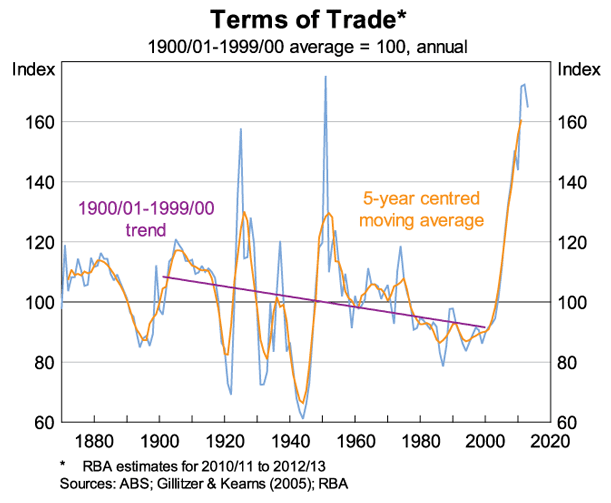

Gruen’s presentation moved on to the Terms of Trade and the mining boom. His chart of the ToT forecast out for 40 years was mind-bogglingly simplistic. Last year I discussed in detail the patterns in the Terms of Trade and the reasons for concern about Dutch Disease. Even the RBA has noted that the ToT never simply glides back slowly from a peak, but typically crashes to far below the long run average (here’s a long run chart).

{kind=link}

The next day Max Corden, Bob Gregory and Peter Sheehan presented detailed analysis of the current Terms of Trade boom and surging investment in mining. These three individuals had probably more experience and knowledge about the topic than the rest of the profession added together. Corden argued that the optimal policy response to the resources boom depends on how long you expect it to last. If you expect it to last indefinitely, as Treasury does, then you could probably do nothing. Although he thought that a highly unlikely scenario.

Ross Garnaut was the only one in the room to suggest that we might want to consider the policy question of what to do if you have just had a short term resources boom and did nothing about it? A much more pressing question given that the ToT has peaked and the historical record shows no precedent for a long boom.

Later, Garnaut spoke about China’s development and Wing Thye Woo provided some insights into Chinese politics, including the problematic political incentives within the Communist Party. If I add this analysis to Treasury’s, and to Ken Hernys’s suggestion that one way for non-mining sectors to adapt is to send production offshore, I get the impression that Australian economic policy has been outsourced to the Communist Party of China.

Ken Henry’s analysis (link has full speech transcript) was very important. He made the observation that the mining boom is not soaking up workers but displacing them by making non-mining trade exposed parts of the economy very uncompetitive. Of course Judith Sloan had her own interpretation:

In effect, mining has been papering over the weakness in the rest of the economy.

Actually, what Ken Henry said is that foreign mining construction investment causes the high dollar, which then causes the slumping non-mining trade-exposed sectors. Although in an environment of low credit growth, other sectors would still be struggling.

Sloan further noted:

But listening to some of the speakers, it was easy to gain the impression that some economists think Australia would be better off without mining. After all, it is largely foreign owned, it doesn’t employ many workers and mining companies hardly pay any tax. And by pushing up the value of the Australian dollar, life is made more difficult for firms in other sectors, most notably those in non-mining trade exposed industries.

I think Sloan is missing the point entirely – there is value in macro-economic stability, and whenever a country has a boom, they forget about the inevitable bust. Ergas said it was odd that we think of mineral wealth and resources as a curse, or a disease. But when asked whether the Spanish might have also thought their foreign funded construction boom was nothing but sunshine and lollipops, and might continue forever, he had little constructive to add. Indeed, I asked him this exact question:

“Henry, you say the the benefits from the mining boom are what you have left when the boom is over. Yet by your reasoning we should all become engineers and labourers, build as many rail lines, ports, pipelines and gas wells as possible, let the dollar reach record highs, let other industries collapse and take no extra taxes from the mining sector. Only then will we be left a prosperous economy when the boom is over.”

Apparently I suffer from Rip Van Winkle fallacy. We won’t simply wake up in forty years. The economy will still exist in the mean time, adjusting back and forth. While I think his forty years is a bit optimistic, he basically has no prescription for macro-economic management regardless of any circumstance. It’s privatisation, deregulation, and lower wages all the way. Not really the guy I’d be looking to for policy advice.

Speaking of very little constructive contribution, the amount of talk about Dutch Disease, with absolutely no reference to foreign ownership and the demand for the Aussie dollar, very little about interest rates and the carry trade, nothing about currency intervention, nothing about anything, really, except nice polite chit-chat about magically becoming more productive, which makes no sense at all because we would actually have to become more productive than everyone else, was a worry. And remember Dr Wei? To become more productive in non-mining sectors they need to invest in more capital equipment, which is exactly what is not happening during a mining construction boom.

Vested Interests

If there was one final lesson, it was that top quality independent thinkers in the profession are vastly outnumbered by vested interests.

For example, Michael Porter thinks that incomes taxes on the rich ‘crowd out’ philanthropy , that there has not been one decent public university anywhere in the world, ever, and that school vouchers are clearly the only way to provide a fair school system. He also said he wished he could live 50 years longer to see just how massive our mining boom will be. According to his CV some very powerful people take him seriously. When Porter asked Ken Henry about decreasing taxes on the super rich so that they might be more inclined to start ‘a private university like the University of Chicago’, Henry at least made it clear that the question was absurd. By the way, the Productivity Commission has very good research on taxes and charitable giving here.

Lawrence H White, George Mason Professor, and an exceptionally engaging speaker, spent his time in the spotlight promoting his book on the Clash of Economic Ideas. If his speech was anything to go by, the book explains how the ideas of the Mount Pelerin Society have stood the test of time, and that governments can do almost nothing to promote well-being and social aims (and that the US might default on its debts to itself).

I asked Professor White whether he thought his discussion was even-handed, noting that he was exceptionally flattering of the Mt Pelerin Society’s members, against a caricature of the ideas of John Maynard Keynes. If I read his book, apparently another chapter deals with Keynes’ ideas in more detail.

Another audience member took this line of enquiry further, noting that the initial meeting of the Mount Pelerin Society in 1947 was funded by bankers and wealthy business people, and that it probably had some vested interest in promoting post-war privatisation policies and a right-wing agenda from the start. White responded that, in fact, he was a member of the society, and that it was now mostly funded by members and their institutions, be they universities or private ‘think-tanks’. Oh, now I get it.

Then there were the usual suspects – some already mentioned such as Judith Sloan, Henry Ergas and some who really shouldn’t have been there at all, like Steven Kates and the statistician of the Master Builders Association.

Lucky, amidst all of this, there were some high quality papers presented by up and coming young stars of the profession, and I learnt a great deal about a wide variety of topics from them.

I want to end with some lessons:

- A Nobel Prize in economics is not an indicator of public speaking ability

- those who know the least talk the most, and this applies to economic debate in the Australian media more generally

- the good guys are completely outnumbered by the vested interests

- there is an absolute lack of disclosure about financial interests of people offering economic policy advise and contributing, “as experts”, to the public policy debate

- The standards of statistical understanding vary enormously

- No one knows what money is or where it comes from

- Representatives of our public institutions are good at talking without saying anything of value

- Ideology rules the day

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin